Fresh glimmers of hope for the eurozone (technical)

(ユーロ圏に希望の兆し(テクニカル))

By Ambrose Evans-Pritchard Economics

Telegraph Blog: Last updated: August 30th, 2012

(ユーロ圏に希望の兆し(テクニカル))

By Ambrose Evans-Pritchard Economics

Telegraph Blog: Last updated: August 30th, 2012

Very quickly, for the handful of readers who share my quirky interest in monetary data.

マネタリー・データについて僕のひねくれた関心を共有してくれる一握りのユーザー向けにサクッと行きます。

By the way, any commentator on this thread who wilfully conflates Monetarism and Keynesian demand theory one more time is disqualified and sentenced to Dante’s 8th Circle of Hell (Bolgia IX) for sowers of discord and schism.

ところで、またまたマネタリズムとケインズの需要論をわざと一緒くたにしている人、君たちは失格。

離間と不和の種を蒔いた罪により、ダンテの第八圏悪意者の地獄逝きを宣告します。

Seminator di scisma, fuor vivi.

不和と分裂の種を蒔いた者達だ。

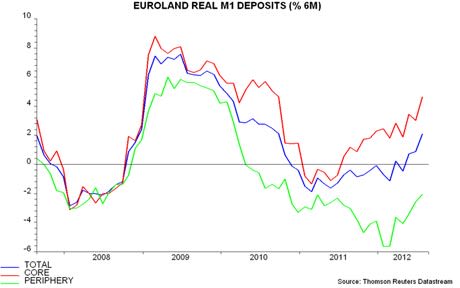

The most useful M1 monetary gauge for the eurozone – real six-month M1 growth – has continued to churn higher.

ユーロ圏を観察する上で最も有益なM1マネタリーサプライ(6ヶ月間の実質M1伸び率)は相変わらず酷く荒れています。

The July data suggest that EMU money contraction bottomed out in April and May. The core is now rising fast, and Ireland is moving into their camp.

7月のデータが示唆するのは、ユーロ圏のマネー縮小は4月と5月で底入れしたということです。

コアでは現在急上昇していまして、アイルランドもこの動きに参入しつつあります。

Typically, this is a leading indicator of industrial output by around six months. It is a pattern, not a prediction.

通常、これは約6ヶ月間先の工業生産を示す先行指標です。

これはパターンであって、予測ではないのです。

Here are the charts from Simon Ward at Henderson Global Investors:

以下はヘンダーソン・グローバル・インベスターズのサイモン・ウォード氏によるグラフです。

Just so there is no misunderstanding, this does not mean the eurozone is "recovering". Far from it.

誤解のないように申し上げますと、これはユーロ圏が「回復中」だという意味ではありません。

とーんでもない。

It would suggest – ceteris paribus, and depending on events in the US, China, and the global oil markets, etc – that eurozone output will trough in the Autumn.

グラフが示唆しているのは、(他の事情が同じだとすれば、そして米国、中国、および国際原油市場などでの事態次第で)秋のユーロ圏の生産は底に達するということです。

Recession may well get worse for a while before the money effects feed through, but the potential outlook for early 2013 is better.

不況も、マネーサプライの影響が浸透するまで、しばらくの間は悪化するかもしれませんが、2013年初頭の見通しはましのようです。

Mr Ward says surging money growth in Germany is the real political risk. This may test the patience of Bundesbank and the German professoriate to breaking point.

ドイツでのマネー急増は本物の政治リスクだ、とウォード氏は言います。

これはドイツ連邦銀行と同国の学識者先生方の沸点を試すことになるかもしれません。

At the end of the day, there is no plausible way to set policy for the North and South of the eurozone. The structure is unworkable.

結局のところ、ユーロ圏の北部と南部のための政策を決めるに当たって、妥当な方法なんてないんですよ。

They can hold it together but only by creating endless distortions for one area or the other, with an endless lurch from one crisis to another, until the maniacs who created monetary union are finally hanged from lampposts by a justly enraged mob. One notes dispassionately, however, that mobs aren’t what they used to be.

無限危機一髪を続けながら、あっちこっちでネジレを無限創作することでしかユーロ圏はまとまっていられないんですから…通貨同盟を生み出したキチガイが遂に、怒り狂った暴徒に正しくも高く吊るされるまで…。

とはいえ、暴徒も昔とは違うんですよね、と冷めた指摘をしてみるテスト。

Be that as it may, money cycles within EMU’s Bataan Death March can be powerful. They can lift equities a long way. Conversely, they can clip the wings of AAA safe-haven bonds enough to hurt.

それはさておき、ユーロ版死の行進のマネーサイクルはパワフルかもしれません。

株価をどーんと上げられるんですから。

逆に言えばですよ、マネーサイクルはAAA格付け国の行動を、相当、制限することが出来るわけです。

You can be absolutely certain that hedge funds – usually operating on a three-month time-frame – are paying very close attention to the money data and whatever they think about the viability of EMU or the Second Coming of the D-Mark.

ヘッジファンド(通常3ヶ月単位で行動します)がマネーサプライのデータに細心の注意を払っていること、そしてヘッジファンドがユーロの持続可能性またはドイツ・マルク再臨について考えていることについて、確信を持って良いと思います。

Personally, I think there are still risks that the global mini-slump of the last few months could tip into a "bad equilibrium" or a "negative feedback loop" to borrow the vogue terms of the IMF, if we are not very careful.

注意していないと、世界的ミニ・スランプが今年最後の2-3ヶ月間に「悪い均衡」か、IMFのなんだかわかんない定義を借りると「ネガティブ・フィードバック・ループ」に陥るリスクは残っている、と個人的には思っています。

The Draghi Plan may be derailed. The six dissenting Fed hawks at the regional banks may block QE3. Capital flight from China may turn the current hard-landing into the kind of crisis that almost nobody (except Prof Victor Shih, Caixin’s Andy Xie, Also Sprach Zarathustra, and a few others) have even begun to think about.

ドラギ・プランだっておじゃんになるかもしれません。

米国では、6つの反動タカ派地区連銀がQE3を邪魔するかもしれません。

中国からの資本の逃避は、既存のハードランディングを、未だ誰も想像し始めてすらいないような危機にしてしまうかもしれません(ヴィクター・シー教授とか、財新のアンディ・シー氏とか、こう語っちゃったツァラトゥストラとか、その他少数を除いて誰も、ですが)。

But here at least is something for the bulls, for a bit.

でも、少なくともブル派にとって、ちょっとの間の、ちょっと良い話です。