Europe's money contracts again

(ヨーロッパのマネーサプライがまた減少)

By Ambrose Evans-Pritchard

Telegraph Blog: Last updated: May 30th, 2012

(ヨーロッパのマネーサプライがまた減少)

By Ambrose Evans-Pritchard

Telegraph Blog: Last updated: May 30th, 2012

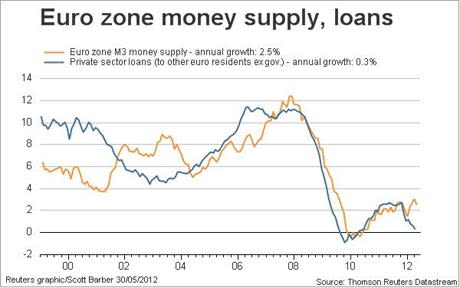

Very quickly, today's ECB data shows that Euroland's money supply is contracting again.

クイックで。

今日発表された欧州中央銀行のデータですが、ユーロ圏のマネーサプライがまた減少中です。

M3 fell by €51bn in April.

M3は4月に510億ユーロ減少。

M1 fell by €55bn.

M1は550億ユーロ減少。

Private credit fell €55bn.

民間向けの信用は550億ユーロ減少。

I don't yet have the country breakdown. My guess is that the Club Med implosion is grim.

国毎の内訳はまだです。

多分、地中海倶楽部の崩壊は深刻でしょうね。

The chart is based on the annual rate. It has not yet picked up the month-on-month contraction.

上のグラフは年率に直したものです。

前月比の減少はまだ持ち直していません。

Clearly the sugar rush from the ECB's 3-year credit blitz has worn off, leaving behind some very toxic effects.

明らかに、ドラギ・バズーカのシュガーラッシュは、非常に厄介な悪影響を残して消えてしまったのです。

Those banks in Italy and Spain that used the money to play the Sarkozy redemption trade by purchasing sovereign debt – some with ten times leverage – are in serious trouble.

国債を買い付けて(中には10倍ものレバレッジをかけて)サルコジ・リデンプション・トレードを行うために欧州中央銀行の資金を使ったイタリアとスペインの銀行は、深刻なトラブルの渦中にあります。

Today's spike in Italian yields shows that they are running out of LTRO money to keep the game. Spanish five-year debt is over 6pc. Muy feo.

今日のイタリア国債の利回り急騰は、ドラギ・バズーカのお金を使い果たしつつあるということを示しています。

スペイン国債5年物の利回りは6%を超えています。

ヤバイですねー。

Quite why anybody thought that a €1 trillion liquidity blitz through the banks is better than €1 trillion in genuine QE is beyond me.

1兆ユーロ規模の正真正銘の量的緩和よりも、1兆ユーロの流動性を銀行経由で流す方が良いとか、一体全体誰が考えたんでしょうか?

僕にはさっぱりわかりません。

I think the ECB has twisted itself in knots to comply with a dysfunctional mandate, enshrined in the dysfunctional Maastricht treaty. One error begets another.

欧州中央銀行は、上手く機能しないマーストリヒト条約に厳かに規定された、上手く機能しない任務に従うために自暴自爆になっているんだと思います。

過ちが過ちを生んでいるのです。

This is not a criticism of Mario Draghi. He had no choice. The Italian and Spanish banking systems were crumbling last November. He outmanoeuvred the Bundesbank for a few months and bought time.

これはマリオ・ドラギECB総裁の批判ではありません。

総裁に選択肢はないのです。

イタリアとスペインの銀行システムは昨年11月に崩壊しつつありました。

2-3ヶ月の間、総裁はドイツ連邦銀行の裏をかいて時間を稼ぎました。

Unfortunately, that time has run out.

残念ながら、その時間も尽きてしまいました。

What next? Any reader brainwaves on how we get out of this?

次はなんでしょうか?

お客様の中に脱出方法をご存知の方はいらっしゃいませんか?