Norway teaches Britain how to choke house booms without killing economy

(ノルウェーは英国に経済を殺さずに住宅バブルを潰す方法を教えてくれました)

By Ambrose Evans-Pritchard Economics

Telegraph Blog: Last updated: May 13th, 2014

(ノルウェーは英国に経済を殺さずに住宅バブルを潰す方法を教えてくれました)

By Ambrose Evans-Pritchard Economics

Telegraph Blog: Last updated: May 13th, 2014

British house prices have fallen 6pc since peaking in November 2007 at an average of £181,618. The average in March this year was £169,124, according to the Land Registry.

英国の住宅価格は平均181,618ポンドを付けた2007年11月のピークから6%値下がりしました。

今年3月の平均は169,124ポンドでした(土地登記所調べ)。

This is based on hard sales data, unlike the asking price indexes used by the property companies. It is backward looking but not massively so.

これは確固たる売却データに基づくものでして、不動産屋が使う希望価格指数とは違います。

後方重視ですが、でもまあ、大して後方でもありません。

The fall in real terms must be around 25pc by now. This is hardly yet a bubble.

実質ベースでの値下がりはこれまでで大体25%ほどに違いありません。

これではとてもバブルとは言えません。

It would be folly for the Bank of England to raise interest rates purely in order to break a London boomlet at time when broad money (M4Lx) contracted at a rate of -3.2pc over the last three months.

イングランド銀行が、広義のマネー(M4Lx)が-3.2%のスピードで過去3か月間減少してるって時に、ロンドンのブームを潰すためだけに利上げしたらバカですよ。

Or indeed, when UK economic output has barely recovered the lost ground from the Lehman crash, and when much of the manufacturing hinterland is still in near slump.

ってか、英国経済の生産がリーマン危機で吹っ飛ばした分を殆ど回復していない時に、しかも製造業地域の大半がまだまだスランプって時にやったらバカでしょ。

Such action would push sterling through the roof before recovery was secure. It would lead to an even more calamitous deficit in the current account, ceteris paribus. The deficit is already running at over 5pc of GDP on a quarterly basis (the worst in the industrial world).

そんなことしたら景気回復がしっかりする前に英ポンドが吹っ飛びますよ。

しかもいまのままなら、経常収支がますますもってマッカッカになりますよ。

今ですらもう四半期ベースでGDPの5%超なんですから(先進国中ワースト)。

The proper answer to the housing shortage is to build houses, if necessary by returning full power to councils to do it themselves.

住宅不足にちゃんと応えるなら、家、作んなさいよ。

必要なら自分達で仕切れるように、地方自治体に全部権限戻して…。

But if the Bank wishes to contain credit, it should learn from Norway's success. Instead of raising rates, it has used "macroprudential" tools. It cut the loan-to-value ceiling on mortgages from 90pc to 85pc. It forced the banks to raise to capital buffers further.

でもイングランド銀行が信用を制御したいのなら、ノルウェーの成功から学ぶべきでしょ。

ノルウェーは金利を上げるんじゃなくて、「マクロプルデンシャル」ツールを使いました。

これで住宅ローンのLTV上限を90%から85%まで下げました。

銀行ももっと資本のバッファーを強化せざるを得なくなりましたしね。

The Norges Bank has recommended a 1pc counter-cyclical buffer based on its view of what constitutes a safe level of credit growth.

ノルウェー中銀は信用成長の安全速度とするものに基づいて、1%の景気変動抑制的なバッファーをオススメしてます。

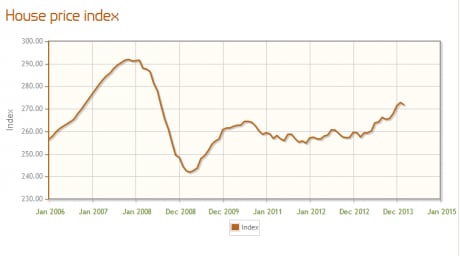

Contrary to claims that these tools never work, they worked splendidly, as you can see from this chart today from HSBC's David Bloom.

こんなもん上手くいくか!という声に反して、ものすっごく上手くいったんですよ、これが…HSBCのデイヴィッド・ブルーム氏が今日公表したグラフの通りです。

Norway's house price boom stopped it its tracks. The krone fell. Collateral damage was limited.

ノルウェーの住宅バブル、フリーズ。

ノルウェー・クローネ、下落。

巻き添え被害、限定的。

The Banque de France explores the whole experience of such policies across the world in its latest Stability Report.

フランス中銀は最新の安定性報告書の中で、全世界でのこういった政策の経験について検討しています。

It includes this paper from the Hong Kong Monetary Authority's Dong He, showing that higher stamp duties were indeed successful in reining in house price spirals.

これには香港金融管理局のDong He氏が記した同論文も含まれていまして、印紙税増税は住宅価格スパイラルの制御に役立ったんだそうですよ。

There have been trials all over Asia. They are not perfect. But they do work. It is time for the Bank of England to stop trying chip out of bunkers with a driver.

実験はアジア全域で行われました。

完璧じゃありません。

でも確かに機能します。

イングランド銀行もバンカーで穴掘りするようなマネはそろそろ止めませんか。