China's Communist Party goes way of Qing Dynasty as debt hits limit

(中国共産党、借金限界で清朝の道か)

AMBROSE EVANS-PRITCHARD

Telegraph: 18 MAY 2016 ? 8:55PM

(中国共産党、借金限界で清朝の道か)

AMBROSE EVANS-PRITCHARD

Telegraph: 18 MAY 2016 ? 8:55PM

Nobody rings a bell at the top of the credit supercycle, to misuse an old adage. Except that this time somebody very powerful in China has done exactly that.

古い格言を悪用して言えば、信用スーパーサイクルのピークでは誰もベルを鳴らさないものです。

でも今回は、中国の物凄く偉い誰かが正にそれをやりました。

China watchers are still struggling to identify the author of an electrifying article in the People's Daily that declares war on debt and the "fantasy" of perpetual stimulus.

チャイナ・ウォッチャーは人民日報で借金と恒久的刺激策という「ファンタジー」に宣戦布告する驚愕の記事を書いた人物を突き止めようと今も悪戦苦闘中です。

Written in a imperial tone, it commands China to break its addiction to credit and take its punishment before matters spiral out of control. If that means bankruptcies must run their course, so be it.

格調ある文体で書かれた記事は、事態が制御不能になる前に、信用中毒を断って罰を受けろと中国に命じています。

破綻が実際に起こるということならば、仕方ないと。

Fifteen years ago such a mystery article would have been an arcane matter, of interest only to Sinologists. Today it is neuralgic for the entire global - and over-globalized - financial system.

15年前なら、このような謎の記事は不可解なもので、中国研究家しか関心を持たなかったでしょう。

現在では(過剰にグローバル化した)世界の金融システムにとって差し迫った内容です。

China's debt is approaching $30 trillion. The fresh credit alone created since 2007 is greater than the outstanding liabilities of the US, Japanese, German, and Indian commercial banking systems combined.

中国の債務残高は30兆ドルに迫っています。

2007年からの新規融資だけでも、米国、日本、ドイツ、インドの商業銀行のシステムの債務残高を全部足した規模を上回っています。

Moody's warned this month that China's state-owned entities (SOEs) have alone racked up debts of 115pc of GDP, and a fifth may require restructuring. The defaults are already spreading up the ladder from local SOE's to the bigger state behemoths, once thought - wrongly - to have a sovereign guarantee.

ムーディーズは今月、中国の公営企業だけでもGDPの115%もの債務を積み上げた、その5分の1は再編を要する可能性があると警告しました。

地方の公営企業から、かつては(間違いにも)政府に保証されていると考えられていたより巨大なものへと、デフォルトは既に広がりつつあります。

To put matters in context, leverage rose by roughly 50 percentage points of GDP in Japan before the Nikkei bubble burst in 1990, or in Korea before the East Asia crisis in 1998, or in the US before the subprime debacle. This gauge is an almost mechanical indicator of a future credit crisis.

1990年に日経バブルが弾ける前、日本ではレバレッジがGDPの50%ほど増加し、1998年の東アジア金融危機の前の韓国や、サブプライム危機が起こる前の米国でも同様でした、と言えば実感がわくと思います。

この尺度はほぼ機械的な将来の信用危機の指標なのです。

As we all know, China is in a class of its own. Debt has risen by 120 to 140 percentage points. The scale of excess industrial capacity - and China's power and life and death over commodity markets - mean that any serious policy pivot by the Communist Party would set off an international earthquake.

皆知っているように、中国は独特です。

債務は120-140%も増加しました。

その過剰生産能力の規模(中国の影響力とコモディティ市場の生死)は、共産党が重大な政策転換を行えば世界揺るがすことを意味しています。

Hence the fevered speculation about this strange article published on May 9 in the house journal of the Politburo. It was no ordinary screed.

従って、5月9日に政務局の広報誌に掲載されたこの奇妙な記事を巡って、憶測が白熱しているわけです。

いつもの長談義ではなかったのです。

The 11,000 character text - citing an "authoritative person" - was given star-billing on the front page. It described leverage as the "original sin" from which all other risks emanate, with debt "growing like a tree in the air".

11,000文字から成る記事は(「権威ある人物」による)、一面でトップ扱いを受けました。

それはレバレッジを、その他全てのリスクが生まれる「原罪」と、債務は「空中で樹木のように育つ」と評しました。

It warned of a "systemic financial crisis" and demanded a halt to the "old methods" of reflexive stimulus every time growth falters. "It is neither possible nor necessary to force economic growing by levering up," it said.

また「システミックな金融危機」について警告し、成長が軟化する度に脊髄反射的な刺激策という「昔のやり方」を止めるよう要求しました。

「経済成長を融資増加で強いることは可能でも必要でもない」

It called for root-and-branch reform of the SOE's - the redoubts of vested interests and the patronage machines of party bosses - with an assault on "zombie companies". Local governments were ordered to abandon their illusions and accept the inevitable slide in tax revenues, and the equally inevitable rise in unemployment.

更に「ゾンビ企業」をターゲットに、公営企業(既得権益の砦であり党幹部の利権機構)を抜本的に改革するよう呼びかけました。

地方自治体は幻想を捨てて税収の否応ない減少、そして同様に避けようのない失業者の増加を受け容れるよう命じられました。

If China does not bite the bullet now, the costs will be "much higher" in the future. "China's economic performance will not be U-shaped and definitely not V-shaped. It will be L-shaped," said the text. We have been warned.

中国が今決意しなければ、将来の犠牲は「遥かに増大する」でしょう。

「中国の景気動向はU字型にはならず、V字型には絶対にならない。L字型だろう」とのこと。

僕らは警告されたわけです。

Jonathan Fenby, a China veteran at Trusted Sources, says you can interpret the piece in two very different ways: either as a "call to arms" after three years of foot-dragging on the Third Plenum reforms, or the "last gasp for reformers who see their agenda slipping away."

トラステッド・リソーシズの中国問題のベテラン、ジョナサン・ファーンビー氏は、この記事は2つの非常に異なる形で解釈出来ると言います。

第3回会議の改革を3年間見合わせてきた挙句の「戦闘準備命令」か、もしくは、「自分達の計略が失敗しつつあると考える改革派の最期のあがき」とのこと。

"We see the current state of affairs as very much resembling the old imperial court, where various factions fight for attention of the undisputed leader ? namely, Xi," he said.

「今の状況は古の宮廷と凄く似ていると思っている。様々な派閥が誰しも認めるリーダー、つまり習近平主席の注意を引こうと争っているわけだ」

Mr Fenby compares it to the Qing Dynasty in the late 19th century, when reformers battling to modernize the economy were ultimately defeated by the old guard. The same pattern recurred under Chiang Kai-Shek's Kuomintang in the 1920s and 1930s. Each time it ended in stagnation. The difference today is that China is vastly more important to the world economy.

同氏はこれを19世紀末の清朝に例えました。

当時、経済の近代化を目指して闘う改革派は、結局、守旧派に敗北しました。

同じパターンが1920年代と1930年代の蒋介石の国民党政権でも起こりました。

いつも低迷で終わるのです。

今日の違いと言えば、中国が世界経済にとって以前よりも圧倒的に重要になったということです。

Most think the author was either President Xi Jinping himself, or his right-hand man Liu He - who handles daily operations for the 'Leading Group', China's version of the White House National Economic Council.

殆どの人は執筆者は習近平主席そのものか、彼の右腕である劉鶴氏だと考えています。

「先頭グループ」(中国版ホワイトハウス国際経済会議)の日常的なオペレーションを仕切る人物です。

A day later the People's Daily published a hitherto closed-door speech by Mr Xi lashing out at "careerists and conspirators existing in our Party and undermining the Party's governance".

その翌日、人民日報は、これまでは非公開だった習主席の、「党内に存在し党のガバナンスを阻害する出世第一主義者や陰謀家」を非難するスピーチを掲載しました。

He denounced the latest property bubble and excesses in the banking system, but confusingly he also laced his talk with quotes from Confucious, Mao, and Marx - the latter increasingly part of his discourse as he invokes dialectical materialism and other such forgotten gems.

主席は直近の不動産バブルと銀行システムの過剰を非難しましたが、混乱を招くことに、孔子、毛沢東、マルクスの言葉を豊富に引用しました。

主席が弁証法的唯物論やその他の既に忘れ去られた素晴らしい物を引き合いに出す中で、ちなみにマルクスの引用は増えています。

It was the usual incoherence we expect from the new Helmsman. He may not be the clear-thinking mystery man after all, yet it would courting fate to ignore the warnings from the People's Daily altogether.

この新しい操縦士からは、いつもの支離滅裂を予期していました。

彼は結局、明確に思考する謎の人物ではないかもしれませんが、人民日報のワーニングを完全にスルーするのは不吉でしょう。

The latest stop-go credit cycle began in mid-2015 and has since accelerated to an epic blow-off, with the M1 money supply now growing at 22.9pc, by the fastest pace since the post-Lehman blitz.

直近のストップ・ゴー信用サイクルが始まったのは2015年中盤でした。

その後、史上最高の水準まで加速されて、M1マネーサプライの伸び率は今ではリーマン危機後の大刺激策から最速の22.9%に達しています。

Wei Yao from Societe Generale estimates that total loans rose by $1.15 trillion in the first quarter, equivalent to 46pc of quarterly GDP. "This looks like an old-styled credit-backed investment-driven recovery, which bears an uncanny resemblance to the beginning of the 'four trillion stimulus' package in 2009. The consequence of that stimulus was inflation, asset bubbles and excess capacity," she said.

ソシエテ・ジェネラルのWei Yao氏の試算では、総融資残高は第1四半期に1.15兆ドル、四半期GDPの46%に相当する分増えたのだとか。

「これはまるで昔ながらの信用担保とする投資を燃料にした回復みたいだ。2009年の『4兆刺激策』の始まりに不気味に似ている。あの刺激策の結末はインフレと資産バブルと過剰生産能力だった」と彼女は言います。

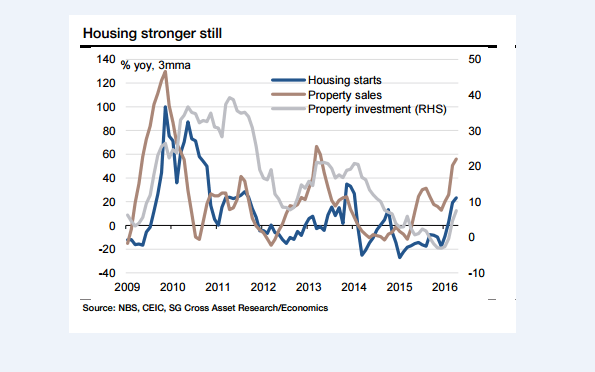

House sales rose 60pc in April, despite curbs to cool the bubble. New starts were up 26pc. Prices jumped 63pc in Shenzhen, 34pc in Shanghai, 20pc in Beijing, and 18pc in Hefei. Panic buying is spreading to the smaller Tier 3 and 4 cities with the greatest glut.

バブルの抑制にも拘らず、住宅販売は4月に60%増加しました。

新規着工は+26%でした。

価格はシンセンで+63%、上海で+34%、北京で+20%、河北で+18%となりました。

パニック買いは著しい供給過剰になっているティア3やティア4の都市まで広がりつつあります。

It all has echoes of the stockmarket boom and bust last year. "Investors are convinced that the government will guarantee that housing prices won't fall," said Professor Zhu Ning from the Shanghai Advanced Institute of Finance, speaking to the South China Morning Post. It also sounds like Britain.

全て昨年の株式市場の大相場を色濃く反映しています。

「投資家は住宅価格が下がらないことを政府が保証してくれると確信している」とサウス・チャイナ・モーニング・ポスト紙に上海高級金融学院のZhu Ning教授は言いました。

There was a slight cooling in April but less than headlines suggested. The old measure of total social financing (TSF) slipped but this was more than offset by record bond issuance of $180bn. Together they reached a 26-month high.

4月は若干収まったものの、ヘッドライン程でもありませんでした。

TSFという昔の指数は下落しましたが、これは1,800億ドルという史上最高額の債券発行でおつりがくるほどオフセットされました。

合せて26ヶ月ぶり最高に達しました。

Capital Economics says budgeted funds must be disbursed by the end of this quarter under new finance ministry rules, implying another $310bn of bonds by late June.

キャピタル・エコノミクス曰く、新しい財務省のルールによって計画された資金は今期中に支出されなければならず、これはつまり6月終盤に更に3,100億ドルの債券が発行されることを意味するとのこと。

The fiscal boost will be 'front-loaded'. The money will pile up in accounts and flood the economy over the late summer. If the usual time-lags hold, the mini-boom will last for a few more months. Then the trouble will start. Needless to say, markets may roll over long before the economy itself.

財政支出増加は「前倒し」になるでしょう。

マネーは口座に積み上げられ、夏終盤に経済に大量放出されることになります。

通常のタイムラグがあるとすれば、ミニ・ブームは2-3ヶ月続くことになります。

トラブルが始まるのはそれからです。

いうまでもなく、市場は経済そのものよりも随分早くロールオーバーするかもしれません。

A number of western fund managers jumped the gun last year - including Britain's Crispin Odey -betting that the long-awaited China crisis was about to unfold. Some over-estimated the importance of the Shanghai equity fiasco; others mistook China's new currency regime for a devaluation (there was none), and many misread the credit, transport, and industrial data.

昨年は西側ファンドマネジャーが多数、長らく待たれていた中国危機が始まりそうだと考えて、フライングしました(英国のクリスピン・オディを含む)。

上海の株暴落の重要性を過大評価するところもあれば、中国の新しい為替制度をデバリュエーション(これは全くなし)だと勘違いしたところもあり、多くは信用、輸送、産業データを読み間違えました。

Bloomberg reports that Roslyn Zhang from China's sovereign wealth fund (CIC) mocked them for their "herd mentality" at last week's Skybridge Alternatives conference in Las Vegas.

ブルームバーグは、中国CICのRoslyn Zhang氏が先週ラスベガスで開催されたスカイブリッジ・オルターナティヴス・コンファレンスで、彼らの「群集心理」を馬鹿にしたと報じました。

"They really don't know much about China but they just spend two seconds and put on the trade. Should we pay two and 20 for treatment like this?" she said, meaning the industry fee of 2pc in tithes and 20pc of profits. She vowed to cull amateurs mercilessly from CIC patronage.

「中国について大してわかっちゃいないのよ。それなのにトレードするのに2秒しか費やさないって。こんなやり方に給料をやるべき?」と言いました。

また、CICからアマチュアを無慈悲に一掃すると誓いました。

Yet this year the China bears may get their revenge, if they have any money left to play with. The rot in the country's $7.7 trillion bond markets is metastasizing. Bo Zhuang from Trusted Sources said more than 100 firms cancelled or delayed bond issues in April due to widening credit spreads.

しかし今年、そのお金さえあれば、中国はリベンジ出来るかもしれません。

7.7兆ドルの中国債券市場の腐敗は転移しつつあります。

トラステッド・リソーシズのBo Zhuang氏は、4月は100社を超える企業が金利スプレッドの拡大を理由に債券発行をキャンセルまたは先延ばししたと言いました。

Ten companies have defaulted this year, with the shipbuilder Evergreen, Nanjing Yurun Foods, and the solar group Yingli Green Energy all in trouble this month. But what has really spooked markets is the suspension of nine bonds issued by the AA+ rated China Railways Materials, the first of the big central SOE's to signal default. "This has greatly weakened investors' long-standing expectation of implicit government support," he said.

今年、10社が倒産しました。

今月は造船会社のEvergreen、Nanjing Yurun Foods、そして太陽光グループのYingli Green Energyが苦戦中です。

しかし市場を本当に震え上がらせたのは、デフォルトの兆しが見えた最初の大手公営企業、AA+格付けの中国鉄道材料グループが発行した債券を9つも売買停止にしたことでした。

「これは投資家が以前から持ってきた隠れた政府支援への期待を相当弱めた」とのこと。

Bo Zhuang said investors have poured money into bonds in the latest frenzy. The stock of corporate bonds has jumped by 78pc to $2.3 trillion over the last year. It is the epicentre of leverage through short-term 'repo' transactions, and it is now coming unstuck.

また同氏は、投資家は最近の騒動で債券に資金を投入したと言いました。

社債の残高は昨年1年間で78%も急増して2.3兆ドルとなりました。

これが短期の「レポ」取引によるレバレッジの中心であり、今や崩れつつあります。

"The experience with the stock market shows how difficult it can be to contain a reversal in leveraged bets. In our view, a bond market crisis would be much more destructive," he said.

「株式市場の経験から、レバレッジを利用した賭けで失敗を防ぐことがどれほど困難たり得るかがわかる。我々の考えだと、債券市場危機は遥かに破壊的になるだろう」とのこと。

With luck, the rest of us outside China will have three or four more months to order our own affairs before the storm gathers. Whether it is bumpy landing, a hard landing, or a crash landing, depends on who the "authoritative person" in Beijing turn out to be.

運があれば、中国国外にある僕らには、嵐が本格化する前に自分達の始末をつけるために3-4ヶ月の猶予があるでしょう。

それが荒っぽいランディングになるか、ハード・ランディングになるか、それとも墜落になるのか、それは中国政府の「権威ある人物」次第です。