BIS fears emerging market maelstrom as Fed tightens

(BIS:FRBの金融引き締めで新興市場大惨事を危惧)

By Ambrose Evans-Pritchard

Telegraph: 12:21PM BST 13 Sep 2015

(BIS:FRBの金融引き締めで新興市場大惨事を危惧)

By Ambrose Evans-Pritchard

Telegraph: 12:21PM BST 13 Sep 2015

Global debt levels are dangerously high and central banks cannot keep the game going indefinitely, warns the high priest of orthodoxy

世界的に債務レベルが危険水域まで上昇してるぞ、中銀だっていつまでもこんなことやってらんないんだからな、と正統派の指導者が警告!

Debt ratios have reached extreme levels across all major regions of the global economy, leaving the financial system acutely vulnerable to monetary tightening by the US Federal Reserve, the world's top financial watchdog has warned.

債務比率が世界経済の主要地域全部で極端なレベルに達し、金融システムはFRBの金融引き締めに丸腰状態になったぞよ!と世界最高の金融監視機関がワーニングです。

The Bank for International Settlements said the wild market ructions of recent weeks and capital outflows from China are warning signs that the massive build-up in credit is coming back to haunt, compounded by worries that policymakers may be struggling to control events.

BISによると、この数週間の市場のワイルドな値動きと中国からの資本流出は、政策立案者は事態のコントロールに悪戦苦闘しているのかも、という懸念を燃料に、馬鹿でかく積み上げた信用のツケが回ってきつつあるというワーニング・サインなんだとか。

"We are not seeing isolated tremors, but the release of pressure that has gradually accumulated over the years along major fault lines," said Claudio Borio, the bank's chief economist.

「単独のゴタゴタはないけど、主要な断層線に沿って長年蓄積されてきたプレッシャーの放出はあるね」とBISのチーフ・エコノミスト、クラウディオ・ボリオ氏。

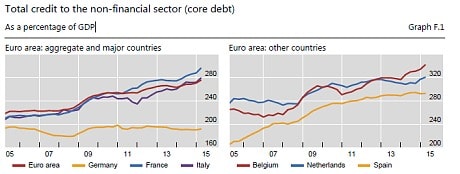

The Swiss-based BIS said total debt ratios are now significantly higher than they were at the peak of the last credit cycle in 2007, just before the onset of global financial crisis.

スイスに拠点を置くBISは、債務比率のトータルは今や、前回は2007年(世界的な金融危機の開始直前)の信用サイクルのピークを思いっ切り上回っている、と言います。

Combined public and private debt has jumped by 36 percentage points since then to 265pc of GDP in the the developed economies.

官民合わせた借金の合計は、先進国だと、GDPの265%まで跳ね上がりました。

This time emerging markets have been drawn into the credit spree as well. Total debt has spiked 50 points to 167pc, and even higher to 235pc in China, a pace of credit growth that has almost always preceded major financial crises in the past.

今回は新興国も信用バブルに引き込まれましたからね。

債務の総残高は50ポイントも上がって167%。

中国だったらもっとすごくて235%。

信用増加のスピードは過去のどの大きな金融危機前よりも速かったのです。

Adding to the toxic mix, off-shore borrowing in US dollars has reached a record $9.6 trillion, chiefly due to leakage effects of zero interest rates and quantitative easing (QE) in the US. This has set the stage for a worldwide dollar squeeze as the Fed reverses course and starts to drain dollar liquidity from global markets.

これに加えて、オフショアの米ドル建て負債が史上最高の9.6兆ドルに到達。

米国でのゼロ金利とQEの効果のリークが主な原因。

これで、FRBが世界中の市場から米ドル流動性を吸い上げ始めると、世界的に米ドル不足が発生するお膳立てが出来ちゃったわけです。

Dollar loans to emerging markets (EM) have doubled since the Lehman crisis to $3 trillion, and much of it has been borrowed at abnormally low real interest rates of 1pc. Roughly 80pc of the dollar debt in China is on short-term maturities.

新興国に対する米ドル建て融資の額はリーマン危機以来3兆ドルまで倍増してまして、その大半は1%なんて異常な低金利で借りられました。

中国の米ドル建て負債の大体8割は短期物なんですよね。

* The figures are for 2014. The figures for Q1 of 2015 cited are slightly different

これは2014年。2015年Q1は若干違う。

These countries are now being forced to repay money, though they do not yet face the sort of 'sudden stop' in funding that typically leads to a violent crisis.

これらの国が今、借金返済を迫られているわけですが、通常物凄い危機を発生させる資金「急停止」みたいなもんには未だ直面してません。

The BIS said cross-border loans fell by $52bn in the first quarter, chiefly due to deleveraging by Chinese companies. It estimated that capital outflows from China reached $109bn in the first quarter, a foretaste of what may have happened in August after the dollar-peg was broken.

BISによると、クロスボーダー・ローンは第1四半期の間に520億ドル減ったとかで、これは主に中国企業がレバレッジ解消したから。

試算によると、第1四半期に中国から流出した資本の額は1,090億ドルに到達したとかで、米国ドル・ペッグ制崩壊の後の8月の有様の予告編みたいなもんですね。

China and the emerging economies were able to crank up credit after the Lehman crisis and act as a shock absorber, but there is no region left in the world with much scope for stimulus if anything goes wrong now.

リーマン危機の後、中国と新興国の仲間達は信用増加に成功して、衝撃吸収材の役割を果たしましたが、今何かあっても刺激策やる余裕のある地域なんて、世界に一つも残ってません。

The venerable BIS - the so-called 'bank of central bankers' - was the only global body to warn repeatedly and loudly before the Lehman crisis that the system was becoming dangerously unstable.

いわゆる「中銀マンの銀行」、BIS尊師は、リーマン危機の前に、システムがヤバいほど不安定になりつつあるぞよ、と何度も何度も喧しくワーニングを出した唯一の国際機関でした。

It has acquired a magisterial authority, frequently clashing with the International Monetary Fund and the big central banks over the wisdom of super-easy money.

で、高々とした権威をゲットして、IMFやら大手中銀と超金融緩和の知恵を巡ってちょくちょくやり合ってきました。

Mr Borio said investors have come to count on central banks to keep the game going but engenders moral hazard and is ultimately wishful thinking. "Financial markets have worryingly come to depend on central banks' every word and deed," he said.

投資家は、祭を続けてくれるよね、と中銀を頼るようになっちゃったけど、モラルハザードを生み出してるし、結局は甘い考えなんだよ、とボリオ氏は言ってます。

「金融市場は中銀の一挙手一投足におっそろしいほど依存するようになった」そうです。

A disturbing feature of the latest scare over China is a "shift in perceptions in the power of policy", a polite way of saying that investors have suddenly begun to question whether the emperor is wearing any clothes after all following the botched intervention in the Shanghai stock market and the severing of the dollar exchange peg in August.

中国を巡る最新パニックのいやーな特徴って「政策の力における認識のシフト」。

これは、投資家が、上海市場の介入失敗やら8月の米国ドル・ペッグ制中止なんかを受けて、王様は裸なんじゃないの?と突然言い始めちゃった、ってのを上品に言ってるわけです。

The BIS 'house-view' is that the global authorities may have put off the day of reckoning by holding interest rates below their 'natural' or Wicksellian rate with each successive cycle but this merely stores up greater imbalances, drawing down prosperity from the future and stretching the elastic further until it snaps back. At some point, you have to take your bitter medicine.

BISの「お考え」はというと、世界各国の当局はサイクルの度に金利を「自然」またはウィクセル的な水準以下に抑え付けることで審判の日を先延ばししたかもしれないけど、こんなもんもっと大変な不均衡をため込んで、未来から富を盗んでブチっといくまで引き延ばしまくってるだけだ、とのこと。

いずれツケが回って来るぞ、と。

The BIS report said the rich countries have failed to right the ship over the last seven years or bring leverage back down to manageable levels, as the Nordic states succeeded in doing after the banking crises a quarter of a century ago. Instead they seem to be caught in a Japanese trap.

BISのレポートによると、北欧諸国が四半世紀前に銀行危機の後で成功したように、襟を正してレバレッジを対処可能な水準まで減らすってことを、富裕国は過去7年間にやらなかったんだとか。

代わりに日本式トラップに引っかかったってことみたいですね。

"Aggregate private debt has barely stabilised, let alone started to correct downwards, even in the corporate sector. And government debt continues to rise steadily, in a manner reminiscent of Japan's trend deterioration in the 1990s," it said in its quarterly report released over the weekend.

「民間債務は減り始めてないのはもちろん、殆ど安定すらしてないし。企業セクターですらそうだもん。政府債務の方は、1990年代の日本の悪化傾向を彷彿とさせる形で、着実に増え続けてるし」と週末に公表した四半期報告の中で述べておられます。

Britain, Spain, and the US have cut household debt ratios but this is still not enough to offset the massive jump in public debt since the Lehman crisis.

英国、スペイン、米国は家計の債務比率を減らしましたが、これでもリーマン危機後の政府債務爆増をオフセットするには足りません。

France has suffered the worst deterioration of any major country in the developed world, with total non-financial debt levels spiralling upwards by 75 percentage points to 291pc, overtaking Britain at 269pc for the first time in decades.

フランスは先進国の主要国としては最悪の悪化に見舞われて、非金融機関の総債務比率はなんと75%も急上昇して291%に…数十年ぶりに英国(269%)を抜きました。

The concern is what will happen as the Fed prepares to raise interest rates for the first time since 2006, perhaps as soon as this week.

心配なのは、FRBが2006年以来初めて利上げの準備をしたら(下手すりゃ今週にも)どうなるかってことですね。

A study on financial spillovers in the BIS report found that much of the global financial system remains anchored to US borrowing rates, whether or not countries have fixed exchanged rates or floating currencies, and regardless of normal theory on trade links and business cycles.

BISのレポートの金融的波及効果に関する論文からは、固定為替制だろうが自由変動制だろうが関係なく、しかもトレード・リンクやビジネス・サイクルに関する通常の理論とかも関係なく、世界的な金融システムの大半は相変わらず米金利に固定されたままだってことがわかります。

On average, a 100 point move in US rates leads to a 43 point move for emerging markets and open developed economies, with powerful knock-on effects on longer-term bond rates. "We find economically and statistically significant spillovers," it said.

平均すると、米金利が100ポイント動くと新興国と開放された先進国は43ポイント動いて、長期金利にも強烈な波及効果を与えるようです。

The grim implication is that emerging economies may face a monetary shock as rates ratchet higher, even if the liabilities are in their own currencies.

金利が上昇したら、自国の通貨建ての借金だったとしても、新興国はマネタリー・ショックに見舞われるかも、ってイヤーな予感が致します。

Enthusiasts for the 'BRICS' and mini-BRICS insist that today's EM squall is entirely different to the crises in the early 1980s and mid-1990s since the governments of these countries no longer borrow in dollars or hard-currencies - though their companies clearly do, and on a very large scale.

「BRICS」やミニBRICSのファンは、米ドル建てとか外貨建てでもう借金してないんだから、今の新興国騒動は1980年代初頭とか1990年代中盤のあれとはぜーんぜん別モンだもん!と言い張ってますが、これらの国の企業は明らかにやっちゃってるわけで、しかも無茶苦茶デカいスケールでやらかしてます。

The BIS data suggests that this assumption may be complacent. Emerging markets may just as vulnerable this time, and perhaps more so given the much greater stock of debt.

BISのデータからは、この推測が楽観的かもしれない、ってことがわかります。

新興国は今回だって同じ位丸腰かもしれないし、借金の山がもっともっとデカいことを考えたらもっともっと丸腰かもしれないよっと。

What remains unclear is whether QE by the European Central Bank will delay the denouement yet again. Cross-border loans surged by $748bn in the first quarter, and $536bn of this was in euro-denominated debt.

相変わらずよくわかんないのは、ECBのQEがまたこの審判の日を先送りしてくれるかどうかってこと。

クロスボーダー・ローンは第1四半期に7,480億ドルも急増したし、この内の5,360億ドルはユーロ建てなんだよね。

Even American companies are issuing securities in euros in record volumes - so-called 'reverse yankee bonds' - to take advantage of lower rates in Europe, often making an implicit bet that the euro will weaken further. Their foreign debt issuance has doubled in pace since 2013, reaching $93bn in the first half of this year.

米企業のユーロ建て債券発行額だって史上最高になってるし(いわゆる「リバース・ヤンキー・ボンド」)。

ヨーロッパの低金利を利用しちゃおうって狙いで、ユーロはもっと安くなるって暗黙の賭けに出てることも良くありまして。

Global banks based in London also appear to be borrowing huge sums in euros to fund activities around the world , pushing offshore euro liabilities to a record $2.8 trillion.

ロンドンに拠点を置く国際銀行も、世界各国での活動資金調達のためにユーロ建てで爆借りしてるっぽいですね。

で、ユーロ建てのオフショア負債を史上最高額の2.8兆ドルまで増やしちゃって…。

The ECB is in effect displacing the Fed. This may mean that the baton passes safely from one super-power bank to another, buying a little more time.

ECBは事実上、FRBに取って代わりつつあるんですね。

これは、超大国中銀Aから超大国中銀Bにバトンが無事に渡されて、もちょっと時間稼ぎが出来た、って意味かも…。

Mr Borio warns investors not to push their luck. "It is unrealistic and dangerous to expect that monetary policy can cure all the global economy's ills," he said.

ボリオ氏は投資家に調子に乗るなとワーニングしてます。

「金融政策が世界経済の問題をぜーんぶ解決出来る、なんて期待するのは非現実的だし危険だ」そうですよ。

Nor is there any easy way out of the debt-trap now encompassing much of the globe. "If I were you, I would not start from here," he said.

それに、今、世界の大半を包囲してる債務トラップから脱出するのは簡単じゃないし。

「僕ならここから始めようとはしないね」とのことです。