Time running out for China on capital flight, warns bank chief

(中国: 資本逃避の時間切れだ!と総裁がワーニング)

By Ambrose Evans-Pritchard

Telegraph: 8:43PM GMT 01 Feb 2016

(中国: 資本逃避の時間切れだ!と総裁がワーニング)

By Ambrose Evans-Pritchard

Telegraph: 8:43PM GMT 01 Feb 2016

'The Chinese have not been very convincing. There is a perception that the renminbi could weaken drastically,' warns the Institute of International Finance

「中国人にはあんまり納得出来ないんだよねー。人民元が思いっ切り下落するかもって認識があるんだよね」とIIFがワーニング。

China is rapidly losing the confidence of global lenders and capital outflows risk turning virulent if the current policy paralysis continues, the world's top banking body has warned.

中国は各国首脳の信頼を猛スピードで失いつつある上に、今の政策麻痺が続くようなら資本流出が猛烈になりかねない、と世界トップの銀行団体がワーニングしました。

"There is a perception that the renminbi could weaken drastically," said Charles Collyns, the managing-director of the Institute of International Finance in Washington.

「人民元が思いっ切り下落するかもって認識があるんだよね」とワシントンの国際金融協会(IIF)のチャールズ・コリンズ専務理事。

Mr Collyns said the authorities have so far failed to articulate a coherent strategy, and there are serious worries that outflows of capital could accelerate, broadening into a flood beyond Beijing's control.

同氏曰く、当局は未だまともな戦略を立てられてないし、資本流出が加速して、中国政府のコントロールの及ばない怒涛の流出に拡大するかもって心配も深刻なんだとか。

"The Chinese have not been rigorous and they have not been very convincing," he told The Telegraph.

「中国人は頑張ってないし。全然納得出来ないし」と小紙に語りました。

Mr Collyns said China has already allowed the renminbi (yuan) to weaken against the country's new trade-weighted basket of currencies, stoking suspicions that the recent shift from a crawling dollar-peg to a more opaque foreign-exchange regime is really a cover for devaluation.

更に、中国は既に人民元がバスケット通貨に対して下落するのを放置プレーして、米ドルのクローリング・ペッグからますます怪しい為替制度に最近シフトしたのは実はデバリュエーション隠蔽のためじゃないの、という疑惑に燃料を投下したじゃないか、と言いました。

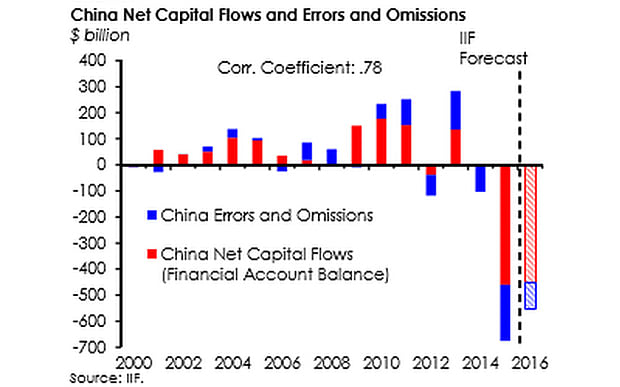

The IIF, the chief global body for the banking industry, calculates that capital outflows from China reached $676bn last year. The central bank has been burning through foreign exchange reserves to offset the bleeding and shore up the currency, culminating in intervention of $140bn in December, by some estimates.

銀行業界の最高国際機関、IIFは、中国から昨年の間に流出した資本の額は6,760億ドルに達したと試算しています。

中国人民銀行はこの流出を相殺して人民元を支えるために外貨準備を融かしまくり、12月の介入は1,400億ドルとかいう試算もあります。

A big drop in the yuan would send a deflationary shockwave through a fragile world economy already on the cusp of a debt-deflation trap, and do so at a time when the eurozone and Japan are actively driving down their currencies. It would risk a pan-Asian currency storm along the lines of 1998, but on a much bigger scale.

人民元爆下げは既に債務デフレ・トラップ寸前のヨボヨボ世界経済全体にデフレ電波を送るでしょうし、しかもそれがユーロ圏と日本が積極的に通貨下落をやらかしてる真っ最中。

1998年張りの全アジア通貨嵐になりかねないんだけど…スケールは遥かにデッカイっていう…。

China is not just another country. Its fixed capital investment has been running at $5 trillion a year, matching the combined total of North America and Europe. This has led to excess capacity across swathes of industry that casts a shadow over the entire global system.

中国はその他諸々じゃないからね。

ここの固定投資は年間5兆ドルもあって、北米とヨーロッパを足した規模なんだから。

これであっちもこっちも余剰能力のある産業だらけになって、全世界のシステムに影を落としてるってわけ。

Chinese officials insist solemnly that the new basket rate is the "decided policy of China" and will be upheld come what may, but concerns are mounting that they may be overwhelmed by market forces.

中国のお役人は真面目な顔で、新バスケット制度は「中国の断固たる政策」だとか、何が何でも死守するとか言い張ってるけど、市場の力に圧倒される可能性があるもなんて不安が募ってるわけ。

The crucial question is whether the exodus of money is chiefly a one-off move by Chinese companies and investors to pay off dollar debt - and to unwind "carry trade" positions in dollars – as the US Federal Reserve raises interest rates and drains liquidity. If so, the outflows are largely benign and should make the world's financial system safer.

重要なのは、資金の大量流出は、FRBが利上げして流動性をなくそうとしてる中での、主に一回限りの中国企業投資家の借金返済(あと米ドル建ての「キャリートレード」ポジ解消)かどうかってことよね。

だとしたら、流出も概ね良性なわけで、世界の金融システムの安全強化になるはずだし。

Mark Tinker, head of equities for AXA Framlington in Asia, said the bulk of the outflows are to pay off liabilities. "Chinese corporates are issuing corporate bonds in record quantities and using the capital to restructure their balance sheets, both onshore and offshore. This is not capital flight, it is asset liability matching, both duration and currency. It is a good thing being presented as a bad thing," he said.

アクサ・フラムリントン・アジアのヘッド・オブ・エクイティ、マーク・ティンカー氏は、流出の大半は借金返済だって言ってますね。

「中国企業はバランスシートを建て直すためにオンショアとオフショアの資本を使って、史上最多の社債を発行してるんだよね。これは資本逃避じゃないから。資産負債のマッチング。デュレーションとカレンシーの両方。ワルっぽく見せかけた良いことよ」とのこと。

The IIF's Mr Collyns, a former assistant US Treasury Secretary, is less sanguine. He calculates that total dollar debt in China peaked at roughly $1.5 trillion in late 2014, if all forms of exposure are included. "We think they have paid off a third of this. Half of the outflows are to repay dollar debt," he said.

IIFのコリンズ氏(元副財務長官)はそこまで楽観してませんけど。

彼の計算だと、中国の米ドル建て債務の残高は、あらゆる形のエクスポージャーを含めると、2014年終盤の1.5兆ドルがピークだったとか。

「この3分の1くらい返したんじゃないのかな。流出の半分は米ドル建ての借金を返済するためさ」

"What is worrying is that there could be a broadening of the outflows. There has been a surge in 'errors and emissions' and this is ominous. A lot of this is a capital outflow below board through inflated trade invoices and other forms of subterfuge, and some of it is ending up in the London property market," he said.

「心配なのは、流出拡大があり得るってことよ。『誤差脱漏』が急増したし、これって不気味じゃん。水増し請求なんかの手口を使った水面下での資本流出がこれに山ほど含まれてるし。一部はロンドンの不動産市場に流れ着いてるよ」

Mr Collyns said there is no guarantee that the outflows will slow even if all the dollar debt is paid off since Chinese companies may start taking out "long" dollar positions (short renminbi) in the currency markets if they fear that Beijing is losing control.

コリンズ氏は、米ドル建ての借金を返済した所で流出が減速するなんて保証はないね、だって中国企業が中国政府はコントロールをとれなくなりつつあるんじゃないかと不安に思えば、為替市場で米ドル「ロング」ポジションを取り始めるかもしんないんだから(つまり人民元のショート)、と言います。

"The Chinese have to restore confidence by pushing through reforms. There must be greater transparency in fiscal and monetary policy, and they must tackle excess industrial capacity. At the moment they won't impose losses on anybody," he said.

「中国人は改革を押し進めて信頼を回復しなきゃいかんのよ。財政政策も金融政策ももっともっと透明性がなくちゃ。でもって余剰生産もどうにかせにゃ。今のところ、誰にも損を背負わせようとしないんだから」

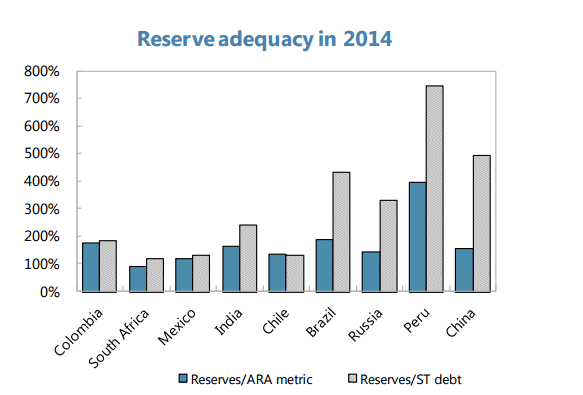

The warnings come as China's $3.3 trillion foreign reserves fall to the bottom end of the safe band under the International Monetary Fund's measure of reserve adequacy (ARA).

このワーニングが出た頃、中国3.3兆ドルの外貨準備はIMFのARAが定めるセーフバンドの底まで減少。

These reserves are relatively low by emerging market standards, given that Beijing is trying to defend a semi-fixed exchange rate and do so within a framework of heavy capital flows. The Philippines, Thailand, Peru, Brazil, India and even Russia score higher.

中国政府が準固定為替レートを防衛して、しかも怒涛の資本流出のフレームワークの中でそうしてることを考えると、これって新興市場のスタンダードだと比較的低いレベルだし。

フィリピン、タイ、ペルー、ブラジル、インド、ロシアですらもっとあるから。

The IMF recommends a band of 100pc to 150pc under its complex ARA measure. China is currently near 120pc and almost certainly fell further in January.

IMFの複雑なARA指標のオススメレベルは100-150%。

中国は今や120%近くになっている上に、ほぼ確実に1月はもっと下がってます。

Societe Generale said the safe level for China is $2.75 trillion. After that Beijing will lose operational flexibility. The country has roughly $600bn left – at the most – before it finds itself in a very uncomfortable situation. "They haven't got as much headroom as people think," said Albert Edwards, the bank's global strategist.

ソシエテ・ジェネラル曰く、中国にとっての安全水準は2.75兆ドルだとか。

それを超えたら、中国政府は操作柔軟性をなくしちゃう。

相当厄介な状況まで(多く見積もって)あと6,000億ドルほどだね。

「皆が思ってるほどの余裕はないよ」と同行のグローバル・ストラテジスト、アルバート・エドワーズ氏は言います。

Mr Edwards said the central bank is automatically tightening monetary policy as it runs down reserves, adding to the growing threat of bad loans in the banking system. "This is not something that can continue for very long. If they resist downward pressure on the currency, they will shrink the money supply," he said.

更に、中国人民銀行は準備金を減らすと自動的に金融政策を引き締めちゃって、銀行システムの不良債権の脅威に油を注ぐことになると述べました。

「これはそう長い間続けられるこっちゃないから。通貨の下落圧力に抵抗したらマネーサプライを縮小させることになる」

"All of the indicators we're look at from the housing market and fiscal stimulus say the economy should be bottoming out. The surprise is that the Chinese data is still so weak. That is worrying. The risk is that they will snatch a hard-landing from the jaws of recovery," he said.

「住宅市場から財政刺激まで、僕らが見てる指標は全部、経済は底打ちのはずだって示してるけどね。驚きなのは、中国のデータが相変わらずかなり弱いこと。こりゃ心配だよ。景気回復の顎からハードランディングをゲット!とかしちゃう危険性ありかな」だそうです。