Day of reckoning postponed as global recovery builds

(世界的な景気回復強化で審判の日は先送り)

By Ambrose Evans-Pritchard

Telegraph: 8:05PM BST 04 Aug 2015

(世界的な景気回復強化で審判の日は先送り)

By Ambrose Evans-Pritchard

Telegraph: 8:05PM BST 04 Aug 2015

Monetary expansion in Europe, America and China all point to stronger growth this year, signalling another leg to the global expansion

ヨーロッパ、米国、中国の金融拡大はぜーんぶ今年の成長がいつもより堅調だと示唆しています。また世界的な経済成長のサインですね。

With hindsight it is clear that the world economy came within a whisker of recession earlier this year.

世界経済が今年先に不況寸前だったのは、今思えばはっきりしてたし。

Global shipping volumes contracted by 3.4pc between January and May, according to Holland's CPB world trade index.

オランダCPBの国際貿易指数によると、国際船積量は1-5月期に3.4%も減少したそうで。

This episode is now behind us. Leading indicators and monetary data in the US, Europe and China point to an accelerating rebound over coming months.

これも今や過去のこと。

米国、ヨーロッパ、中国の主要指標も金融データも、今後数か月間は加速的な回復を示唆しています。

Gabriel Stein, from Oxford Economics, says the growth rate of the world's real M3 money supply – based on the US, China, EMU, the UK, Japan and Canada – rose to a six-year high of 6.2pc in June.

オックスフォード・エコノミクスのガブリエル・スタイン氏曰く、世界の実質M3マネーサプライの伸び率(米国、中国、ユーロ、英国、日本、カナダがベース)は6月に6年ぶり最高の6.2%まで上昇したとか。

The M3 gauge tends to lead economic growth by 12 months or so, suggesting that the worst may soon be over.

このM3ゲージは12ヶ月程先の経済成長を示す傾向があって、もう直ぐ底打ちだよと伝えています。

In Europe, the monetary kindling wood of recovery is clearly catching fire. Spain is growing at its fastest pace since the post-Lehman crisis. So is Ireland.

ヨーロッパでは景気回復の兆しがはっきり強まっています。

スペインはリーマン危機以後、最速ペースで成長中。

アイルランドもご同様。

The triple effects of quantitative easing by the European Central Bank, a 12pc fall in the trade-weighted index of the euro in 15 months and the fall in Brent crude prices from $110 to $50 have together lifted Euroland out of its six-year depression.

ECBのQE、15ヶ月間で12%下落したユーロの実効レート、そしてブレント原油の値下がり(110ドルから50ドル)のトリプル効果が、ユーロ圏を6年間の不況から浮上させたと言うわけ。

The property slump is over. Standard & Poor's expects house prices to rise 3pc in Holland, 4pc in Portugal, 5pc in Germany and 9pc in Ireland this year.

不動産不況、終了。

S&Pは今年は住宅価格が値上がりすると予想していまして、オランダ3%、ポルトガル4%、ドイツ5%、アイルランド9%だそうです。

Simon Ward, from Henderson Global Investors, said a key gauge of the eurozone money supply – real six-month M1 – is growing a blistering rate of 12.6pc. This implies a surge in spending later this year. "Monetary policy is too loose in the eurozone. It is highly questionable whether they can really keep going with QE until the end of next year," he said.

ヘンダーソン・グローバル・インベスターズのサイモン・ウォード氏は、ユーロ圏のマネーサプライの主要ゲージ(実質6ヶ月M1)は12.6%なんて猛スピードで伸びていると言います。

これはつまり、今年中に支出が爆増するってことですね。

「ユーロ圏の金融政策なんてゆるっゆるだから。来年末までQEをほんとに続けられるんだか、怪しいもんだ」とのこと。

America is slowly weathering the effects of the strong dollar. The economy grew at a 2.3pc rate in the second quarter. Capital Economics expects it to accelerate to 3pc in the second half. Loans are growing at an 8pc rate. It is not a glorious boom but nor is it the stuff of global meltdowns.

米国は強いドルの影響をゆるゆるとしのいでいます。

第2四半期の米経済成長率は2.3%でした。

キャピタル・エコノミクスは、下半期には3%まで加速するだろうと予測。

貸出の伸び率は8%。

強烈な好景気ってわけじゃないけど、世界的メルトダウンでもありませんな。

The commodity crash may feel as if Armageddon has arrived but it is, in reality, the tail-end of China's hard landing, compounded by Saudi Arabia's political decision to flood the global crude market and strike a blow against Russia, Iran and the US shale industry.

商品相場クラッシュでハルマゲドン到来!とか感じるかもしれませんけど、現実には、中国のハードランディングの結末に、国際原油市場をジャブジャブにしてロシアとイランと米シェールにガツンと一発食らわせてやる!というサウジアラビアの政治決断が燃料を投下した結果です。

"There has been a sharp drop in the 'commodity-intensity' of China's economic growth," said George Magnus, a trade expert and a senior adviser to UBS.

トレード・エクスパートでUBSのシニア・アドバイザーのジョージ・マグナス氏はこう言ってます。

「中国の経済成長の『商品依存』が急に回復したよね」

"This has sent very chilly winds through parts of the world. Vast swathes of the emerging market universe have lost their export prop."

「世界各地は震え上がったさ。新興市場ユニバースの殆どが輸出って柱をへし折られたんだから」

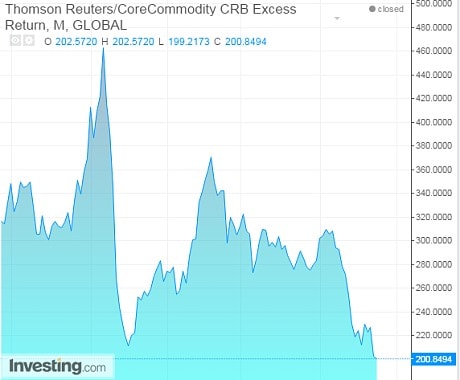

The synchronized rout that we have seen across the gamut of commodities – from copper, to thermal coal, soya and milk - is certainly hair-raising. The Reuters-Jeffrey CRB index of raw materials has collapsed by almost 60pc from its peak in 2008 and is back to levels first reached in 1971.

銅から石炭、大豆、牛乳まで、ありとあらゆる商品で僕らが目撃した同時多発カオスには、確かに震え上がりますよね。

ロイター・ジェフリーズCRB指数は2008年のピークから60%近く爆下げした挙句、1971年に初めてタッチしたレベルに戻っちゃいました。

There is a risk that this could go too far and metastasize, leading to a second leg of global deflation. This would play havoc with debt dynamics in a world where debt ratios have risen by 30 percentage points of GDP since 2008, reaching unprecedented levels.

これが行き過ぎちゃって転移しちゃって世界的デフレ第2幕を開くって危険性はありますね。

債務比率が2008年比+30%と史上最高記録達成しちゃった世界で、これは債務ダイナミクスをむっちゃくちゃにするかもしれないし。

Yet commodity crashes are double-edged. They act as a stimulus for the world economy. The consuming nations are enjoying a $500bn "tax cut" from the OPEC cartel.

でも商品相場クラッシュは諸刃の剣です。

世界経済の刺激にもなるんですよ。

消費国はOPECカルテルからの5,000億ドルもの「減税」を美味しく頂いてますから。

The slide may soon touch bottom in any case, if it has not already done so. The Baltic Dry Index measuring freight rates for dry commodities has almost doubled since the start of June. The shipping firm Clarksons said it is being driven by a revival of Chinese steel demand.

いずれにせよ、この値下がりももう直ぐ底かもしれないし…まだ底打ってないとしてだけど。

バルチック海運指数は6月初めのほぼ2倍だし。

海運会社のクラークソンズによると、中国の鉄鋼需要復活が燃料だそうです。

The chances are that the growth scare of 2015 will prove to be a false alarm, much like the nasty episodes of 1987 and 1998 when market tantrums – frightening at the time – turned out to be innocuous. The cycle had another two years' life both times.

2015年の成長懸念は間違いでした、ってことになりそうですね。

1987年、1998年の、当時はおっそろしかったマーケット癇癪玉が実は無害だったってわかった時の酷い事件と激似。

Markets over-reacted violently this week to a fall in China's PMI manufacturing gauge to 47.8 in July, fearing that the economy is now in the grip of such powerful debt-deleveraging that stimulus no longer works. But the survey was distorted by the immediate fallout from the stock market debacle in Shanghai.

今週、マーケットは中国のPMI製造業指数が7月に47.8まで落っこちたことに物凄いリアクションを見せました。

中国経済がもはや刺激の効果も無力化されるほど強烈な債務レバレッジ解消にはまり込んだんじゃないかと危惧したんですね。

でも、これは上海の株騒動のあおりをまともに食らった、まともなデータじゃないから。

Nomura says its "growth surprise index" is signalling a "strong rebound" after touching the bottom in May.

野村證券曰く、「成長サプライズ指数」は5月に底打ちした後「堅調なリバウンド」のサインを出しているそうですよ。

The bank's "heat map" for China shows that 53pc of the components are flashing "hot", including electricity output, chemical fibres, non-ferrous metals, chemical fertilizers, real estate investment, car production and M2 money. The "hot" ratio is up from 44pc in May, and 31pc last October.

野村證券の中国「ヒートマップ」によると、電力生産、化学繊維、非鉄金属、不動産投資、自動車生産、M2マネーなど53%が「ホット」とか。

「ホット」の割合は5月の44%、昨年10月の31%を上回ってますね。

It hard to know whether premier Li Keqiang misjudged China's hard-landing earlier this year. The Politburo is deliberately trying to deflate the country's $26 trillion credit bubble – up from $9 trillion in early 2009 - knowing that stimulus-as-usual is becomes more dangerous with each stop-go mini-cycle.

李克強首相が中国のハードランディングについて今年先にミスジャッジしてたのかどうかは、わかり辛いですな。

常務委員会は26兆ドルもの信用バブルをわざと潰そうとしています(2009年初頭は9兆ドル)。

いつもの刺激策は、ミニ・サイクルでやらかす度に益々やばくなってるってことをしってるんですね。

Yet the calibrated slowdown may have gone too far. One-year borrowing costs rose from zero in 2011 to 5pc in real terms last year as deflation took hold, a form of passive monetary tightening.

でもこういう管理減速もやり過ぎたのかも。

デフレが本格化して、一年もの借入金利は2011年のゼロから去年は実質ベースで5%まで上昇したし。

受け身の金融引き締めの一種ですわ。

Thanks to China's dollar peg, the exchange rate has risen 20pc against the euro, 60pc against the Japanese yen and 100pc against the Russian rouble since mid-2012.

中国がドル・ペッグ制を布いてるおかげで、人民元も2012年中盤以降、ユーロに対して20%、日本円に対して60%、ロシア・ルーブルに対して100%も上昇したしね。

At the same time the economy went over a "fiscal cliff" at the start of the year as local governments saw a collapse in revenues from land sales and were prohibited from bank borrowing.

それと同時に、中国経済は今年の初め、地方自治体の土地売却収入が激減して銀行からの借入も禁止されたおかげで、「財政の崖」から落っこちたし。

The authorities were slow to respond to multiple shocks but they have finally get their bond market off the ground. Local entities are issuing securities at a pace of $130bn a month, amounting to a shot of stimulus. Real borrowing costs have halved since late last year.

当局は同時多発ショック対応が遅かったものの、最終的には債券市場を立ち直らせましたね。

地方自治体は月間1,300億ドルのペースで債券を発行してまして、これが刺激策になってます。

実質借入金利も昨年末の半分になりました。

Nomura says monetary policy is now as loose as in the depths of the post-Lehman crisis. A mini-blitz of a fresh infrastructure spending has begun to plug the fiscal gap.

野村證券によると、金融政策は今やリーマン危機後のドツボ時ほど緩いんだとか。

インフラ新規建設のミニ刺激策が財政ギャップを埋め始めましたし。

It is not a return to the manic uber-stimulus of the boom years, but it is unlikely that China will spiral deeper into its slump over coming months. The Communist Party controls the quantity of credit through the state-controlled banks, and it is using that lever to pump-prime the economy.

バブル時代のキチガイ刺激策復活、じゃありませんが、中国が今後数か月間に不況を悪化させることはないでしょう。

中国共産党は政府系銀行を使って信用の量を調整していますし、経済活性化ツールを利用しています。

If need be, it can cut the reserve requirement ratio for banks from 18.5pc to zero, injecting $3 trillion into the system. Only once Beijing has played that final card, should we start to worry. China's day of reckoning is still far away.

必要なら、銀行の準備比率を18.5%からゼロにすることだって出来るんだし。

これでシステムに3兆ドルも注入出来ますよ。

中国政府がこの最後のカードを切ったら、僕らも心配し始めるべきだけど。

中国の審判の日はまだまだ先なのだ。