One simple reason why global stock markets are reeling

(世界中の株式市場がへたれている簡単な理由)

By Ambrose Evans-Pritchard, International Business Editor

Telegraph: 6:45PM BST 17 Oct 2014

(世界中の株式市場がへたれている簡単な理由)

By Ambrose Evans-Pritchard, International Business Editor

Telegraph: 6:45PM BST 17 Oct 2014

The world's central banks have slashed stimulus by $125bn a month since the end of last year - leading to the current market rout

世界中の中銀は昨年末以来、月に1,250億ドルずつ刺激を縮小しています…で、この有様ですよ。

It is no mystery why global liquidity is evaporating. Central banks have turned off the tap. They have reduced net stimulus by roughly $125bn a month since the end of last year, or $1.5 trillion annualized.

世界中で流動性が蒸発しているのは、謎でも何でもありません。

中銀が蛇口を締めてしまったのです。

去年の末からこっち、毎月およそ1,250億ドルほども刺激を減らしました。

年率に換算すれば1.5兆ドルに上ります。

That is a shock for the financial system. The ratchet effect has been incremental, but relentless. We are finally seeing the consequences, with the usual monetary policy lag.

金融システムにとってはショックです。

影響の広がり方はジワジワですが、ずーっと広がっています。

僕らは遂に、いつもの金融政策の遅行効果を経て、その結末を目にしつつあるわけです。

The Fed and People's Bank of China (PBOC) have stopped their two variants of global QE altogether (for now). Others have chopped their purchases of bonds by half or more. The Brazilians are net sellers, and in a sense they carrying out reverse QE. The Russians have just joined them again.

FRBと中国人民銀行は(今のところ)各自の世界的量的緩和策を完全停止しています。

他の国の中銀は債券購入の量を半分かそれ以上も減らしました。

ブラジル勢は売り手に回って、或る意味、この連中が逆QEをやらかしています。

ロシア勢もそれに再参戦したところです。

Fed tapering has taken out $85bn a month. The markets are having to go it alone as of this month, without their drip feed. Less understood is the effect of global reserve accumulation by the BRICS, emerging Asia, and the Petro-states. This has collapsed.

FRBの縮小額は月に850億ドルです。

マーケットは今月の時点で点滴の注入もなく、自力で頑張るしかありません。

よくわからないのは、BRICS、新興市場、産油国によって積み上げられた準備の影響です。

これも激減しました。

Nomura's Jens Nordvig has crunched the latest numbers for Q3. They show that China's PBOC has completely withdrawn from global asset markets. In fact, it may have sold almost $9bn of bonds, (even adjusting for currency effects). This is a policy shift by Beijing. Premier Li Keqiang said in May that China's $4 trillion foreign reserves are already so big they have become a "burden".

野村證券のイェンス・ノードヴィク氏はQ3の直近の数字を弾き出しました。

中国人民銀行が世界の資産市場から完全撤収したことがこれによって明らかになりました。

実のところ、90億ドル近い債券を売り飛ばした可能性があります(為替の影響を調整してもですよ)。

これは中国政府の政策転換ですね。

李克強首相は5月に、中国4兆ドルの外貨準備は既にデカ過ぎて「重荷」になっていると言いました。

China bought $106bn as recently as the first quarter of 2014, so this is a very sudden shift. Yes, I know, China's purchases of US Treasuries, Gilts, Bunds, French bonds, and Japanese JGBs are not quite the same as QE. There are complex sterilization effects.

中国はつい2014年第1四半期まで1,060億ドルも買い込んでいましたから、これは思いっ切りのシフトです。

はいはい、わかってますよ、中国の米国債、英国債、独国債、仏国債、日国債の購入はQEとイコールではありません。

複雑な不胎化効果がありますから。

Yet there is a fungible effect whether the Fed is buying Treasuries or whether the Chinese central bank is buying them. It is all a form of global QE. It all helps to inflate asset prices, and vice versa if it reverses.

でも、FRBが米国債を買っているのか、中国人民銀行が米国債を買っているのかどうかには代替効果があります。

全て或る種の世界的量的緩和なのです。

全て資産価格を押し上げるのを助けてくれますし、逆の動きがあれば逆の効果が出るわけです。

This was really what Ben Bernanke meant when he first began talking of the "global savings glut". The flood money into the bond markets was compressing yields for everybody. Hence the subprime debt crisis in the US, and hence too the Club Med debt bubble.

これこそ正にベン・バーナンキ元FRB議長が、「世界的貯蓄過剰」を初めて語り始めた時に、言おうとしていたことなんですね

債券相場に怒涛の如く雪崩れ込むマネーは、皆の金利を押し下げました。

だから米国ではサブプライム危機が起こり、だから地中海クラブでは債務バブル危機が起こったわけです。

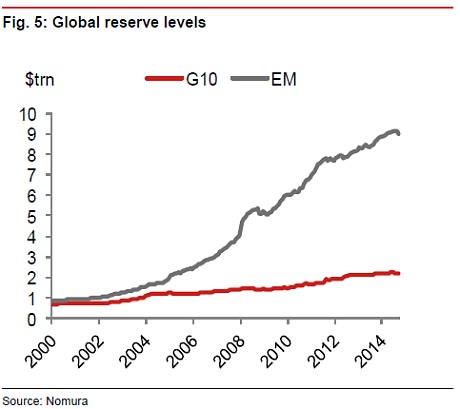

The money had to go somewhere as the rising world powers boosted global FX reserves to $11.3 trillion from under $1 trillion in 2000. It went into safe-haven bonds, displacing that money into everything else.

新興市場が世界的な外貨準備高を2000年の1兆ドル弱から11.3兆ドルまで積み上げる中で、このマネーはどこかに行かねばなりませんでした。

で、セーフヘイヴンの債券に向かい、そのマネーは 他の全てのものに取って代わりました。

Over the latest quarter, almost every country has been choking back: the Bank of Korea has cut net purchases from $25bn to $9bn; the Reserve Bank of India from $43bn to $12bn; the petro-states have cut from $19bn in Q1 to $11bn. (That must surely turn steeply negative with oil at $86 a barrel).

前四半期、ほぼ全ての国がマネーを吐き出しました。

韓中銀は買い越し額を250億ドルから90億ドルに減らしました。

印中銀は430億ドルから120億ドルに、産油国はQ1は190億ドルだったものを110億ドルまで減らしました。

(石油が86ドルまで値下がりしていることを考えればこれは確実にマイナスになりますな。)

Net sellers were: China (-$9bn), Brazil (-$7bn), Singapore (-$7bn), Malaysia (-$5bn), Thailand (-$3bn), Turkey (-$1bn). Overall FX accumulation worldwide fell from $106bn to $22bn.

売り越ししたのは中国(-90億ドル)、ブラジル(-70億ドル)、シンガポール(-70億ドル)、タイ(-30億ドル)、トルコ(-10億ドル)です。

世界中の外貨準備高は1,060億ドルから220億ドルまで減少しました。

The Bank of Japan - now on QE8 -- is buying $75bn a month of Japanese domestic debt. But that is almost a fixture. It is not raising the pace of monthly stimulus.

現在QE8実施中の日銀は毎月750億ドルの日本国債を買い続けています。

でも、それは殆どお決まりのことになっています。

毎月の刺激策を強化してはいないわけです。

Stephen Jen from SLJ Macro Partners said QE by the West since the Lehman crisis has - by a complex process -- set off a roughly comparable increase in the scale of bond purchases by central banks in developing countries. This is a sort of "two-for-one" stimulus, at least for the global bond markets.

SLJマクロ・パートナーズのスティーヴン・ジェン氏は、リーマン危機以降の西側のQEは(複雑なプロセスによって)新興市場の中銀の債券買い付け額とほぼ同じ額を相殺したと言います。

これは「1個のお値段で2個」的刺激策ですね…少なくとも、世界の債券相場にとって。

"The effect has been massive for the world economy, and one of the least understood. Reserve managers are faceless. They sit at computers pressing buttons. The data is not well-tracked," he said.

「世界経済には物凄い影響を与えたね。しかも一番よくわかんない。外貨準備を切り盛りする連中は正体不明だから。コンピューターの前に座ってクリックしてるわけだ。データも余りよくトラッキングされてないし」とのこと。

Unfortunately, it means that the end of QE by the Fed also has a "two-for-one" impact. The world is doubly leveraged on the way back down

残念ながら、それってFRBのQE終了も「1個のお値段で2個」的影響があるってことですね。

リバースの時には世界は倍返しされるわけですよ。

For at least three years a liquidity bonanza has fueled asset booms despite a weak global economy, a slowing China, perma-slump in Europe, and stagnation in Brazil, and Russia. The assumption was that the world economy would eventually catch up with stockmarkets and the frothiest of assets. It has not done so.

少なくとも3年間続いた流動性祭は、世界経済がダラダラで、中国は減速して、ヨーロッパは永遠の不況で、ブラジルとロシアも不景気なのに、資産価格を押し上げました。

世界経済はいずれ株式市場ととってもフロスな資産に追い付く、はずだったんですけどね。

追い付きませんでしたね。

The obvious risk is that the S&P 500, the FTSE-100, the DAX and other bourses will have to continue deflating downwards as the whole process goes into reverse, until the gap is closed.

ハッキリしたリスクは、何もかもがリバースする中で、S&P500、FTSE 100、DAXその他がギャップが埋まるまで下がり続けなければならなくなることです。

Or just as likely, until the blinking starts at the Fed and the People's Bank. QE4 is creeping onto the table already.

または、FRBと中国人民銀行がやばいやばいと言い始めるまでそうなるってことも同じくらいあり得ますね。

QE4は既にメニューに載りつつあります。