Global banks issue alerts on China carry trade as Fed tightens, yuan falls

(FRBの引き締めと人民元の下落のコンボで、世界中の銀行がチャイナ・アラート)

By Ambrose Evans-Pritchard

Telegraph: 4:11PM BST 30 Mar 2014

(FRBの引き締めと人民元の下落のコンボで、世界中の銀行がチャイナ・アラート)

By Ambrose Evans-Pritchard

Telegraph: 4:11PM BST 30 Mar 2014

Citigroup tells clients to brace for second phase of the "taper tantrum" that rocked emerging markets last year, but this time with China at the eye of the storm

昨年新興市場を揺るがせた「QE縮小」の第2波を覚悟せよ、しかし今回の台風の目は中国だ、とシティグループがクライアントにアドバイス。

Three of the world's largest banks have warned that the flood of "hot money" into China is at risk of sudden reversal as the yuan weakens and the US Federal Reserve brings forward plans to raise interest rates, with major implications for global finance.

世界屈指の大手銀行3行が、人民元が下落してFRBが利上げを前倒しすれば、中国へ流入する怒涛の「ホットマネー」は突然逆流するかもしれない、しかも国際金融に著しい影響があるであろう!とワーニングを出しました。

A new report by Citigroup told clients to brace for a second phase of the "taper tantrum" that rocked emerging markets last year, but this time with China at the eye of the storm.

シティグループが出した最新レポートはクライアントに、昨年新興市場を揺るがせた「QE縮小」の第2波を覚悟せよ、しかし今回の台風の目は中国だとアドバイスしています。

"There's a dangerous scenario in which the combination of rising US short-term rates and a more volatile RMB (yuan) could lead to a rather large capital outflow from China," said the report, by Guillermo Mondino and David Lubin.

「危険なシナリオだ。米国短期金利の上昇と人民元の変動激化のコンボで、中国から巨額の資金が流出する可能性がある」とGuillermo Mondino氏とDavid Lubin氏はレポートに記しました。

They argue that China's credit boom has become a "function" of external dollar funding, mostly through offshore lending in Hong Kong and Singapore to circumvent internal curbs. It is a powerful side-effect of super-loose policies by the Fed, which the Chinese have been unable to control. If so, this may snap back abruptly as dollar liquidity dries up and fickle money returns to the US.

中国の信用バブルは、国内規制を回避するために主に香港とシンガポールのオフショア貸出を経由した、外貨ドル建て資金調達の「機能」になった、と二人は論じています。

これはFRBによる超金融緩和策の強力な副作用であり、中国勢には制御不可能でした。

だとすれば、ドル流動性が枯渇して気紛れ資金が米国に還流すると、突然逆転する可能性があります。

Bank lending to emerging markets has surged by $1.2 trillion (£720bn) over the last five years to $3.5 trillion. The banks have funded most of these loans from short-term sources, leaving the whole nexus extremely vulnerable as the US prepares to tighten. The Fed caught markets badly off guard earlier this month when it suggested that interest rates would jump from near-zero to 1pc next year and 2.25pc the year after, a much faster pace than expected.

銀行の対新興市場貸出はこの5年間で1.2兆ドルから3.5兆ドルまで急増しました。

これらのローンの資金源の大半は短資であり、米国が引き締めの準備を進めるにつれ、関係者は総じて被害を受け易い状況に陥っています。

FRBは今月先、金利は来年中にゼロから1%へ、その次の年には2.25%まで、予想よりも遥かに速いペースで跳ね上がるであろうと発表して、市場を思いっ切り不意打ちしました。

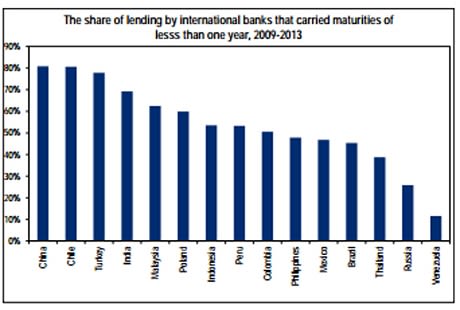

Half of this foreign lending is linked to China, where dollar loans have jumped by $620bn since 2009. Roughly 80pc are at maturities of less than one year. The report warned that higher rates might "erode bank's willingness to roll over their cross-border loans to borrowers in China".

この対外融資の半分は中国関連であり、対中ドル建て融資の残高は2009年以来6,200億ドルも急増しています。

およそ80%が一年以内に期限を迎えます。

レポートは、利上げによって「銀行の中国国内の借手に対する対外融資をロールオーバー意欲が損なわれるだろう」とワーニングを出しています。

Speculators have been borrowing dollars to buy Chinese assets, a flow known as the "carry trade". They often do so with leverage and through convoluted means, some involving use of copper or iron ore as collateral. The bet is that the yuan will strengthen, generating a near certain profit on the exchange rate. This has gone badly wrong as the central bank intervenes to force down the exchange rate, causing the yuan to fall 2.5pc against the dollar since January.

投機家は中国資産の購入のためにドル建てで借り入れをしてきました(いわゆる「キャリートレード」)。

レバレッジをかけたり複雑な経路を通じて借り入れることも多く、中には銅や鉄鉱石を担保にしているものもあります。

人民元は上昇して為替レートでほぼ確実に儲けが出るという前提です。

中銀が人民元を下落させるために介入して、1月以降米ドルに対して2.5%も下落した後は、目論見は完全に外れてしまいました。

Nomura issued a client note on Friday warning that the carry trade is "reversing gear", describing a break-down of discipline in which almost everybody in China from investors, to manufacturers, exporters, and commercial banks have been playing the game. Most of the borrowing has been in dollars and yen on the Hong Kong market.

野村証券は金曜日、キャリートレードを「リバースギア」に入れるよう警告するクライアント・ノートを出し、投資家から製造業者、輸出業者、商業銀行まで中国のほぼ全ての人間が参加してきたゲームのルールは崩壊したと説明しました。

借入の大半は香港市場での米ドル建て、日本円建てです。

Wendy Liu, Nomura's China strategist, said investors are putting too much hope in the promise of fresh stimulus and infrastructure spending, ignoring the risks of a weak yuan.

野村証券のチャイナ・ストラテジスト、ウェンディ・リュー氏は、投資家は人民元安リスクを無視して、追加刺激やインフラ支出の約束に望みをかけ過ぎていると言います。

She said devaluation is a double-edged sword. It helps cushion the shock of China's economic slowdown, boosting "the razor-thin margins" on exporters along the Eastern seaboard. It may also mitigate the "coming wave of credit defaults". But is also exposes the fragility of the system. A view is gaining credence that the weak yuan is an early warning sign that "China's credit bubble may implode imminently", she said.

また、デバリュエーションは諸刃の剣だとも述べています。

これは中国の景気減速ショックの緩和して、東沿岸部の輸出業者の「薄利」を増やしてくれるでしょう。

更に「来る信用デフォルトの波」を軽減するかもしれません。

しかし同時に、システムの弱点をさらすことにもなります。

人民元安は「中国の信用バブルは今すぐにでも弾ける可能性がある」という早期警報だ、という見解の信頼は高まりつつあると同氏は言いました。

The Bank for International Settlements caught the attention of central banks across the world -- especially the Bank of England -- with a report last October warning that foreign loans to China are now large enough to risk a repeat of the 1998 financial crisis in Asia.

BISは昨年10月に中国に対する対外融資は1998年のアジア金融危機を再現出来るほど巨大になっている、と警告するレポートを発表して、世界中の中銀(特にイングランド銀行)から注目を集めました。

"They have more than tripled in four years, rising from $270bn to a conservatively estimated $880bn in March 2013. Foreign currency credit may give rise to substantial financial stability risks associated with dollar funding," it said. Analysts say dollar loans -- to firms, not the Chinese state -- have since risen to $1.2 trillion. Almost a quarter come from British-based banks.

「4年間で3倍以上に増大した。2,700億ドルから、2013年3月には低く見積もっても8,800億ドルにまで増大した。外貨建て融資は、ドル建て資金の調達に関連した金融安定リスクを高める可能性がある」

アナリストは、ドル建て融資(中国政府ではなく対企業)は1.2兆ドルにまで上っているだろうと言っています。

その4分の1近くが英系銀行からのものです。

The BIS said the loan-to-deposit ratio for foreign currencies in China has doubled from 100pc in 2005 to 200pc today. Much of this has been through foreign exchange swaps and forms of credit that are hard to track.

BISは、中国における外貨の預金準備率は2005年の100%から今の200%まで2倍になったとしています。

この大半は外貨スワップや追跡し辛い形式の信用によるものです。

China has $3.8 trillion of foreign reserves and ample monetary fire-power to shore up its financial system if need be. The banks are an arm of the state. The authorities can unleash $2 trillion of credit by slashing the reserve requirement ratio (RRR), currently 20pc. It was 6pc in the late 1990s. The question is whether President Xi Jinping wishes to do so.

中国の外貨準備は3.8兆ドルに上り、必要に応じて金融システムを支えるだけの資金力は十分です。

銀行は政府の一部です。

当局は現在20%とされている預金準備率を引き下げて2兆ドルの信用を放出することが出来ます。

1990年代終盤は6%でした。

問題は、習近平主席がそうしたがるかどうかです。

The current monetary squeeze has been deliberately engineered to crush speculators and prick the bubble before it is too late. Mr Xi's "Third Plenum" reforms aim to break China's reliance on excess credit, and on a catch-up growth model beyond its sell-by date. The paradox is that western lenders may be as much at risk -- or more so -- than the Chinese themselves.

現在の金融引き締めは、手遅れになる前に、投機家を潰しバブルを弾くための意図的なものです。

習主席の「第3の圧力」改革は中国の過剰信用と、賞味期限切れのキャッチアップ型成長モデルへの依存を打破を目指しています。

矛盾しているのは、西側の金融機関が中国人と同じ位、または中国人以上にリスクを負っているかもしれないということです。

Credit Suisse says HSBC is heavily exposed, generating a large chunk of its profits from trades linked to China. The Swiss bank says the speculative part of the carry trade has reached $200bn and entails an intricate web of manoeuvres through Hong Kong. "Various indicators point to stress in the system. The risk of a mis-step is increasing," it said.

クレディ・スイスは、HSBCのエクスポージャーは巨大であり、利益の大部分は中国関連取引から得ているとしています。

また、キャリートレードの投機部分は2,000億ドルに達しており、香港経由の複雑な操作を伴っているとのことです。

「様々な指標がシステムのストレスを示唆している。失敗のリスクは高まっている」

Citigroup said dollar lending to Brazil, India, Indonesia and Turkey has also been enough to create "some threat to external stability". Outflows will have the effect of squeezing domestic credit, and risk pushing these countries into deeper downturns.

シティグループは、ブラジル、インド、インドネシア、トルコへのドル建て融資も「外部安定性に対する脅威」を生み出すに十分だとしています。

資金が流出すれば国内の信用を不足させることになり、これらの国々が一層酷い不況に追い込まれる危険があります。

The worry is different from last year's "taper tantrum" when the Fed's tough talk set off a 100 basis point rise in 10-year US bond yields, driving up global borrowing costs and triggering flight from emerging markets. Mr Lubin said the Fed's shift was the cause of China's "nasty liquidity crunch" in June.

心配されるのは、FRBが昨年QE縮小をほのめかして米国債10年物の金利を100BPも跳ね上がらせ、国際融資金利を押し上げ新興市場からの資金逃避を引き起こした「QE縮小騒動」との違いです。

ルービン氏は、FRBの方針転換こそ中国が6月に見舞われた「酷い流動性不足」の原因だったと述べています。

This time bond yields have been better behaved. Citigroup says investors may be taking false comfort, concluding prematurely that the emerging market stress is over. The Achilles Heel in 2014 may prove to be the Fed's short-term rates.

今回、債券金利はもっと落ち着いています。

シティグループは、投資家は勘違いして安心している可能性がある、新興市場の混乱は終わったと性急な結論を導き出している可能性があるとしています。

2014年のアキレス腱は、FRBの短期金利だと明らかになるかもしれません。