Global finance faces $9 trillion stress test as dollar soars

(米ドル爆上げで国際金融が9兆ドル・ストレステストにチャレンジ)

By Ambrose Evans-Pritchard

Telegraph: 9:29PM GMT 11 Mar 2015

(米ドル爆上げで国際金融が9兆ドル・ストレステストにチャレンジ)

By Ambrose Evans-Pritchard

Telegraph: 9:29PM GMT 11 Mar 2015

The world is more dollarized today that any time in history, and therefore at the mercy of the US Federal Reserve as rates rise

世界は史上最高に米ドルな感じだし、金利が上がったらFRBの言いなりちゃんですね。

Sitting on the desks of central bank governors and regulators across the world is a scholarly report that spells out the vertiginous scale of global debt in US dollars, and gently hints at the horrors in store as the US Federal Reserve turns off the liquidity spigot.

世界各国の中銀総裁やら規制機関のデスクに鎮座するのは、世界中の米ドル建て債務の気の遠くなるような規模を事細かに説明し、FRBが流動性の蛇口をきゅっとしたらどんな恐ろしいことになるかをやんわりほのめかす学術論文です。

This dry paper is the talk of the hedge fund village in Mayfair, and the stuff of nightmares for those in Singapore or Hong Kong already caught on the wrong side of the biggest currency margin call in financial history. "Everybody is reading it," said one ex-veteran from the New York Fed.

このからっからの紙切れはメイフェアのヘッジファンド村で話題になっていまして、既に金融史上最大の為替マージンコールにやられているシンガポールと香港のヘッジファンド村の人々にとっては、とんでもない悪夢です。

元ニューヨーク連銀ベテランは「みんな読んでるよ!」って言ってました。

The report - "Global dollar credit: links to US monetary policy and leverage" - was first published by the Bank for International Settlements in January, but its biting relevance is growing by the day.

『Global dollar credit: links to US monetary policy and leverage』と題されたレポートは1月にBISが公表したものですが、その強烈な関連性は日に日にじわじわきてます。

It shows how the Fed's zero rates and quantitative easing flooded the emerging world with dollar liquidity in the boom years, overwhelming all defences.

FRBのゼロ金利とQEがバブル時代に、新興市場のディフェンスを圧倒して、どれほど米ドルでジャブジャブにしたかを見せつけています。

This abundance enticed Asian and Latin American companies to borrow like never before in dollars - at real rates near 1pc - storing up a reckoning for the day when the US monetary cycle should turn, as it is now doing with a vengeance.

この量に誘惑されて、アジアと南米の企業は(実質金利1%近くで)前例のない米ドル建て借金をして、米国の金融サイクルが変わったら(今気合い入れてそうなってますが)やってくる審判の日をブッキングしました。

Contrary to popular belief, the world is today more dollarized than ever before. Foreigners have borrowed $9 trillion in US currency outside American jurisdiction, and therefore without the protection of a lender-of-last-resort able to issue unlimited dollars in extremis. This is up from $2 trillion in 2000.

一般的に思われていることとは逆に、今の世界は有史以来最も米ドル漬になっています。

外国人は米国外で米ドル建てで9兆米ドルも借りたんですね。

つまりいざとなった時に無限米ドル発行が可能な最後の貸し手さんの保護もないってことですよ。

2000年の2兆ドルからここまで増えちゃったっていう。

The emerging market share - mostly Asian - has doubled to $4.5 trillion since the Lehman crisis, including camouflaged lending through banks registered in London, Zurich or the Cayman Islands.

新興市場(ほとんどアジア)のシェアもリーマン危機からこっち2倍の4.5兆ドルまで増えちゃってまして、しかもロンドンとかチューリッヒとかケイマン諸島なんかの銀行経由でカムフラージュした借金も含まれてます。

The result is that the world credit system is acutely sensitive to any shift by the Fed. "Changes in the short-term policy rate are promptly reflected in the cost of $5 trillion in US dollar bank loans," said the BIS.

その結果、国際信用システムはFRBの一挙手一投足にピリピリですよ。

「短期金利が変わると速効、米ドル建て銀行ローンに5兆ドルのコストがかかる」とBISは言ってます。

Total US dollar debt outside US (米国外の米ドル建て借金)

Markets are already pricing in such a change. The Fed's so-called "dot plot" - the gauge of future thinking by Fed members - hints at three rate rises this year, kicking off in June.

マーケットはそういう変化を既に折り込みつつあります。

FRBのいわゆる「ドット・プロット」(FRBメンバーによる今後の考え方の尺度)は、今年中に3度の利上げをほのめかしています。

一発目は6月です。

The BIS paper's ominous implications are already visible as the dollar rises at a parabolic rate, smashing the Brazilian real, the Turkish lira, the South African rand and the Malaysian Ringitt, and driving the euro to a 12-year low of $1.06.

米ドルがブラジル・レアルもトルコ・リラも南ア・ランドもマレーシア・リンギットも粉砕して対ユーロでも12年ぶり最高の1.06ドルに達して急上昇する中、BISのレポートに書かれた不気味な推測は既に現実のものになりつつあります。

The dollar index (DXY) has soared 24pc since July, and 40pc since mid-2011. This is a bigger and steeper rise than the dollar rally in the mid-1990s - also caused by a US recovery at a time of European weakness, and by Fed tightening - which set off the East Asian crisis and Russia's default in 1998.

DXYは7月以降24%も急騰しています。

対2011年中盤比なら+40%です。

東アジア金融危機と1998年のロシア財政破綻のきっかけになった、1990年代半ばの米国ドル・ラリーよりももっともっとヤバい上がり方ですねえ(あっちも欧州低迷中の米国回復がとFRB引き締めが原因)。

Emerging market governments learned the bitter lesson of that shock. They no longer borrow in dollars. Companies have more than made up for them.

新興市場の政府はあのショックで手痛い教訓を得たわけです。

もう米ドル建てで借金なんてしてないもん。

代わりに企業がもっと借りましたとさ。

"The world is on a dollar standard, not a euro or a yen standard, and that is why it matters so much what the Fed does," said Stephen Jen, a former IMF official now at SLJ Macro Partners.

「世界は米ドル基準だから。ユーロでも日本円でもないんだよ。だからFRBの動きがこれほど重要なんじゃないか」と元IMFで現SLJマクロパートナーズのスティーヴン・ジェン氏は言います。

He says the latest spasms of stress in emerging markets are more serious than the "taper tantrum" in May 2013, when the Fed first talked of phasing out quantitative easing.

また、直近の新興市場の発作は、FRBが初めてQEやめちゃおっかなーとか言っちゃった2013年5月の「テーパーリング談話」よりもっとマジヤバいとのことです。

"Capital flows into these countries have continued to accelerate over recent quarters. This is mostly fickle money. The result is that there is now even more dry wood in the pile to serve as fuel," he said.

「新興市場への資本流入はこの数四半期も加速し続けてるし。殆どは投機資金なのね。おかげで今じゃもっと燃料たっぷりよ」とのこと。

Mr Jen said Asian and Latin American companies are frantically trying to hedge their dollar debts on the derivatives markets, which drives the dollar even higher and feeds a vicious circle. "This is how avalanches start," he said.

ジェン氏は、アジアと南米の企業は死に物狂いで米ドル・デットをデリバティブ市場でヘッジしようと頑張ってると言いますが、これによって米ドルは益々上がるわ、悪循環は益々パワーアップするわっていう。

「雪崩ってこうやって起こるもんなのよ」

Companies are hanging on by their fingertips across the world. Brazilian airline Gol was sitting pretty four years ago when the real was the strongest currency in the world. Three quarters of its debt is in dollars.

企業は指一本で崖っぷちからぶら下がりです。

ブラジルのゴル航空なんて、レアルが世界最強通貨だった4年前はなかなか素敵に見えたもんです。

ここの借金の4分の3が米ドル建てですからねえ。

This has now turned into a ghastly currency mismatch as the real goes into free-fall, losing half its value. Interest payments on Gol's debts have doubled, relative to its income stream in Brazil. The loans must be repaid or rolled over in a far less benign world, if possible at all.

レアルが自由落下するにつれ、これがおっそろしい為替ミスマッチに変身しまして、時価総額が半分になっちゃった。

ゴルのブラジルでの稼ぎと相対的に見てみると、借金の金利支払いは2倍増ですね。

この借金は返済しなくちゃいけないものですし、さもなければ思いっ切り冷たくなった世界でロールオーバーしなくちゃいけない…出来ればの話ですけど。

You would not think it possible that an Asian sovereign wealth fund could run into trouble too, but Malaysia's 1MDM state fund came close to default earlier this year after borrowing too heavily to buy energy projects and speculate on land. Its bonds are currently trading at junk level.

アジアのソブリン・ウェルス・ファンドまでややこしいことになるとか思わないでしょ。

でも、今年に入って、マレーシアの1MDMステートファンドがエネルギー開発投資と土地投機で借金し過ぎてデフォる寸前になったじゃないですか。

ここの債券なんて今じゃジャンク扱いですから。

It became a piggy bank for the political elites and now faces a corruption probe, a recurring pattern in the BRICS and mini-BRICS as the liquidity tide recedes and exposes the underlying rot.

政治家の貯金箱になってたから、今じゃ汚職捜査されちゃってるし。

BRICSだのミニBRICSだので、流動性の潮が引いて腐った水底があらわになると何度も繰り返されてるパターンですな。

BIS data show that the dollar debts of Chinese companies have jumped fivefold to $1.1 trillion since 2008, and are almost certainly higher if disguised sources are included. Among the flow is a $900bn "carry trade" - mostly through Hong Kong - that amounts to a huge collective bet on a falling dollar. Woe betide them if China starts to drive down the yuan to keep growth alive.

BISのデータからは中国企業の米ドル建て負債が2008年比5倍の1.1兆ドルまで急増してるのがわかりますが、怪しいソース分を含めたらほぼ確実にもっとありますね。

この中には9,000億ドルの「キャリートレード」(主に香港経由)が含まれてまして、これは莫大な集団的ドル売りに相当します。

中国が生き延びる為に人民元安操作を続ければ、こいつら悶え苦しむことになりますね。

Manoj Pradhan, from Morgan Stanley, said emerging markets were able to weather the dollar spike in 2014 because the world's deflation scare was still holding down the cost of global funding. These costs are now rising. Even Singapore's three-month Sibor used for benchmark lending is ratcheting up fast.

モルガン・スタンレーのManoj Pradhan氏は、新興市場は2014年の米ドル急騰をしのげたけど、あれは世界のデフレ・パニックが国際的な資金調達コストを抑え続けてたからだと言います。

で、このコストが今や上昇中。

シンガポールのベンチマーク金利、3ヶ月物SIBORなんて急上昇してますから。

The added twist is that central banks in the developing world have stopped buying foreign bonds, after boosting their reserves from $1 trillion to $11 trillion since 2000.

しかもなんと、開発途上国の中銀が準備金を2000年の1兆ドルから11ドルまで膨れ上がらせた挙句、外債買入を止めちゃったんですね。

The Institute of International Finance (IIF) calculates that the oil slump has slashed petrodollar flows by $375bn a year. Crude exporters will switch from being net buyers of $123bn of foreign bonds and assets in 2013, to net sellers of $90bn this year. Russia sold $13bn in February alone.

IIFの計算では、石油大バーゲンでオイルマネーが年3,750億ドルも減ったんだとか。

原油輸出国は2013年には外国債だの外国資産だのを1,230億ドルも買っていましたが、今年は900億ドルの売り手に回りました。

ロシアは2月だけでも130億ドル分も売り払いました。

China has also changed sides, becoming a seller late last year as capital flight quickened. Liquidation of reserves automatically entails monetary tightening within these countries, unless offsetting action is taken. China still has the latitude to do this. Russia is not so lucky, and nor is Brazil. If they cut rates, they risk a further currency slide.

中国もサイド・チェンジしてまして、資本逃避が加速した昨年下旬に売り手に変わりました。

ってことでこれらの国では、準備金が融けちゃったことで自動的に金融引き締めが起こるわけです、それを打ち消すような対策をやらない限り。

中国は未だにその余裕がありますね。

ロシアはそこまで運が残ってなかったりで、ブラジルもご同様。

連中が利下げをやれば益々為替安を招くでしょうな。

Powerful undercurrents in the world's financial system are swirling beneath the surface. Some hope that the European Central Bank's €60bn blast of QE each month will keep the asset boom going as the Fed pulls back, but this is a double-edged effect for the world as a whole. It pushes the dollar yet higher. That may matter more in the end.

国際金融システムの海の水面下で強力な潮が渦を巻いて流れています。

ECBが毎月600億ユーロぶっ放してくれることでFRBが引き上げても資産バブルが続くと良いな、と思ってる人もいますが、これって世界全体でみると諸刃の剣ですよ。

だって米ドルが益々上がるじゃん。

最終的にはその方がもっと問題になるかもよ。

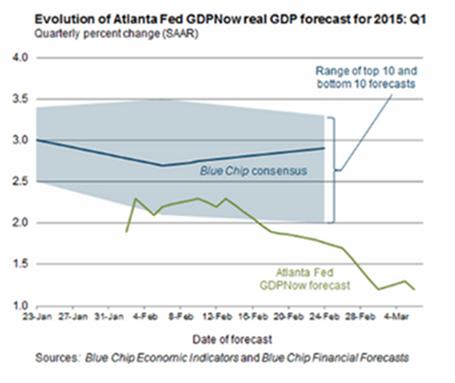

It is possible that the Fed will retreat once again, judging that the world economy is still too fragile to withstand any tightening. The Atlanta Fed's forecasting model for real GDP growth in the US itself has slowed sharply since mid-February.

世界経済が相変わらず引き締めに耐えらんないほどボロボロってことを考えて、FRBがまたまた退く可能性もありますしね。

アトランタ連銀の米実質GDP予測モデルだって2月中旬から急ブレーキかかってるし。

Yet the message from a string of Fed governors over recent days is that rate rises cannot be put off much longer, the Atlanta Fed's own Dennis Lockhart among them. "All meetings from June onwards should be on the table," he said.

でも数日前からあっちこっちの連銀総裁が次々に、利上げをこれ以上先延ばしするとか無理!ってメッセージを出してますよね。

アトランタのデニス・ロックハート総裁とか。

「6月以降の全部の会議で議題にすべき」との仰せですな。

The most recent Fed minutes cited worries that the flood of capital coming into the US on the back of the stronger dollar is holding down long-term borrowing rates in the US and effectively loosening monetary policy. This makes Fed tightening even more urgent, in their view, implying a "higher path" for coming rate rises.

直近の会議の議事録は、米ドルに加えて怒涛の資本還流が起こっていることで米国の長期金利が抑え込まれている上に、事実上、金融政策をゆるゆるにしてるじゃないか、という心配の声が記されています。

これでFRBの引き締めは、彼らの頭の中では、益々切実になっちゃうわけで、つまり来るべき利上げカーブが「益々急になる」って意味ですね。

Nobody should count on a Fed reprieve this time. The world must take its punishment.

今回は誰もFRBが執行猶予をくれるのに期待しちゃいかんですね。

世界はお灸を据えられなくちゃいけません。