US and China tighten in unison, and damn the torpedoes

(米中同時引き締め。かんしゃく玉がどうしたって?)

By Ambrose Evans-Pritchard, International Business Editor

Telegraph: 3:20PM GMT 30 Oct 2014

(米中同時引き締め。かんしゃく玉がどうしたって?)

By Ambrose Evans-Pritchard, International Business Editor

Telegraph: 3:20PM GMT 30 Oct 2014

The world has changed abruptly for investors as the US Federal Reserve and the People's Bank of China both brush aside deflation warnings and press ahead with monetary tightening

FRBと中国人民銀行が一緒になってデフレ・ワーニングを無視して金融引き締めに乗り出しちゃったので、投資家にとっての世界が急変。

Mind the monetary gap as the world's two superpowers turn off the liquidity spigot at the same time.

マネタリー・ギャップにお気をつけくださいー。

世界の二大経済超大国が一緒に流動性の蛇口を締めちゃいましたからー。

The US Federal Reserve and the People's Bank of China have both withdrawn from the global bond markets, each for their own entirely different reasons. The combined effect is a shock of sorts for the international financial system.

FRBと中国人民銀行が、どっちも全くそれぞれのご都合で、国際債券相場から撤収しました。

その影響は国際金融システムにとってちょっとしたショックであります。

The Fed's message on Wednesday night was hawkish. It did not invoke the excuse of a stronger dollar or global market jitters to extened bond purchases. It no longer sees "significant" constraints to the labour market. Instead it spoke of "solid job gains" and a "gradual diminishing" of under-employment.

FRBが水曜日の夜に出したメッセージはタカ派系でした。

債券購入を延長するための、米国ドル高だの国際市場の動揺だのといった言い訳もしませんでした。

労働市場への「重大な」制約ももう考えていません。

その代わりに、「堅調な雇用の増大」と不完全雇用の「段階的減少」について語りました。

This a tightening shift, and seen as such by the markets. The euro dropped 1.5 cents against a resurgent dollar within minutes of the release, falling back below $1.26. Rate rises are on track for mid-2015 after all.

これは、市場の言う通り、引き締めシフトです。

この発表から数分も経たない内に、ユーロは米ドルに対して1.5セント値下がりしまして、1.26ドルを切る水準に逆戻りしました。

結局、利上げは2015年中盤のようですね。

The Fed is no longer printing any more money to buy Treasuries, and therefore is not injecting further dollars into an interlinked global system that has racked up $7 trillion of cross-border bank debt in dollars and a further $2 trillion in emerging market bonds. The stock of QE remains the same. The flow has changed. Flow matters.

FRBはもう米国債を買うために紙幣を刷っていません。

従って、米ドル建ての国際銀行融資を7兆ドル、更に新興市場債を2兆ドルも積み上げた、相互に繋がりあった国際金融システムに米ドルを追加注入していません。

QEのスケールは同じです。

流れが変わったのです。

で、流れってのは大事なのです。

The Fed has ended QE3 more gently than QE1 or QE2. This helps but it may also have given people a false sense of security. The hard fact is that the Fed has tapered net stimulus from $85bn a month to zero since the start of the year.

FRBはQE1やQE2よりもお手柔らかにQE3を終了しました。

これはありがたいんですが、皆に間違った安心感も与えてしまったかもしれません。

FRBが今年の初めからこっち、毎月850億ドルという刺激をゼロまで縮小しちゃったというのは、厳然たる事実なんですから。

The FOMC tried to soften the blow in its statement with pledges to keep interest rates low for a very long time. This assurance has value only if you think QE works by holding down interest rates, as the Yellen Fed professes to believe.

連邦公開市場委員会は声明の中で、金利は非常に長期的に低く据え置くからね、と約束してダメージを和らげようとしました。

この約束は、イェレンFRBがそう思ってるよと言っているように、金利を抑えておくことでQEは上手くいく、と思ってなけりゃ価値がないんですね。

It cuts no ice if you are a classical monetarist and think that QE works its magic through the quantity of money effect, most potently by boosting broad M3/M4 money through purchases of assets outside the banking system.

あなたが古典的マネタリストで、QEの魔法は貨幣の量の効果を通じて効くわけで、一番良いのは銀行システム外で資産を買ってM3/M4を増やすこと、と思ってたら効かないわけです。

Pessimists argue that the world economy is so weak that it needs a minimum of $85bn a month of Fed money creation (not to be confused with zero interest rates) just to avoid stalling again.

悲観主義者は、世界経済はボロボロ過ぎるから、また停止しちゃわないようにするためだけでも月850億ドルのFRBの貨幣創出が必要なんだと言っています(ゼロ金利とごっちゃにしちゃいけませんよ)。

Or put another way, there is nagging worry that tapering itself may amount to an entire tightening cycle, equivalent to a series of rate rises in the old days. If they are right, rates may never in fact rise above zero in the US or the G10 states before the global economy slides into the next downturn.

別の言い方をすれば、テーパリングそのものが引き締めサイクルになっちゃうかもしれない、かつての連続利上げに相当するものになっちゃうかも、という心配があるんですね。

彼らが正しければ、世界経済が次の景気後退に陥る前に、米国やらG10やらで金利がゼロ以上に引き上げられることは永遠にないかもしれません。

It is no great mystery why the world is caught in this "liquidity trap", or "secular stagnation" if you prefer. Fixed capital investment in China is still running at $5 trillion a year, and still overloading the world with excess capacity in everything from solar panels to steel and ships, even after Xi Jinping's Third Plenum reforms.

世界がこの「流動性の罠」、またはこっちの方がお好きなら「長期的不況」の虜になっちゃった原因は、謎でも何でもありません。

習近平主席の第三会議の後ですら、中国の固定資産投資は相変わらず年に5兆ドルもやらかしていますし、太陽光パネルから鉄鋼、船舶までありとあらゆる分野の過剰生産で世界にのしかかっているのも相変わらずです。

Europe has been starving the world of demand by tightening fiscal policy into a depression, running a $400bn current account surplus that is now big enough to distort the global system as a whole. George Saravelos, at Deutsche Bank, dubs it the "Euroglut", the largest surplus in the history of financial markets. The global savings rate has risen to a fresh record of 25.5pc of GDP, the flipside of chronic under-consumption.

ヨーロッパは今や国際システムを丸ごとぐちゃぐちゃに出来る4,000億ドルもの経常黒字を出して、緊縮財政で世界中の需要を干上がらせて不況に追い込んでいます。

ドイチェ・バンクのGeorge Saravelos氏はこれを「ユーログラット」と呼んでいます。

金融市場史上最大の黒字です。

世界の貯蓄率はまた新記録を出してGDPの25.5%まで上昇しました。

ひっくり返せば、慢性的な消費不足ってことです。

Of course, it is not the job of the Fed to run monetary policy for the world, and that is the new problem facing QE-addicted investors. The US economy is growing briskly at a 3pc rate. It can arguably handle monetary tightening, at least for now.

勿論、世界のために金融政策を仕切るのはFRBのお仕事じゃありません。

で、それはQE中毒の投資家が直面する新たな問題なのです。

米国経済は3%の順調なペースで成長しています。

少なくとも今のところ、金融引き締めも乗り越えられるといっても良いでしょう。

New home building is up 17.8pc over the past year. The Case-Shiller 20-City index of house prices is up 22pc since early 2012. Unemployment has tumbled to 5.9pc. Lay-offs have dropped to a 14-year low.

新規住宅着工件数は一年間で17.8%上昇しました。

ケースシラー指数は2012年初頭以来22%も上昇しました。

失業率は5.9%まで激減しました。

人員削減は14年ぶり最低まで下落しました。

We are entering a new phase of the monetary cycle where the US is strong (relatively) and the world is weak (relatively). The Fed has switched from a being the friend of global asset prices, to being neutral at best, with a strong hint of menace.

僕らは、米国が(相対的に)強く世界が(相対的に)弱い、金融サイクルの新段階に突入しつつあります。

FRBは世界の資産価格の友人であることを止めて、良く言って若干の悪意をほのめかしつつ中立的になったわけです。

It is a very odd environment. The US Treasury market is pricing in near-depression conditions. Five-year inflation expectations have suddenly collapsed. You could say it is remarkable that the Fed should be withdrawing any stimulus at all in such circumstances.

大変奇妙な環境ですな。

米国債市場は準不況的な状況を折り込んでいます。

5年インフレ期待は急落しました。

こんな状況でFRBがちょっとでも刺激を引き上げるとかビックリと言って良いでしょうね。

Janet Yellen has to navigate a perilous course between the Scylla of deflation and the Charybdis of corrosive asset booms, just the like the Riksbank this week, or indeed the Bank of Canada, or the Bank of England. Yet the precipitous slide in commodities since June may be a warning sign that stress is building.

ジャネット・イェレン議長は、今週のスウェーデン中銀のように、またはカナダ中銀、またはイングランド銀行のように、デフレとやばい資産バブルの間を苦心惨憺してナビゲートしなければなりません。

でも6月以降の商品の急激な値下がりは、ストレスがたまりつつあるというワーニングサインの可能性がありますね。

There are echoes of 1928, when commodity prices buckled even as the boom on Wall Street was still gathering pace, and as the credit bubble in Weimar Germany was still gathering towards a crescendo. Fed hawks, led by Benjamin Strong, chose to ignore the deflation risk, instead raising rates to teach "speculators" a lesson. The move set off a global chain reaction.

ウォール街バブルが相変わらず加速している上に、ワイマール帝国ドイツの信用バブルが引き続き活気を強めている中でも商品価格が値下がりした1928年っぽいです。

ベンジャミン・ストロング率いるFRBタカ派軍団はデフレ・リスクを無視することに決め込んで、その代わりに利上げは「投機家」への教訓になるなんて言ってます。

こんなことしたら世界的ドミノ倒しになりますよ。

Mrs Yellen is unlikely to repeat that error, but there are many pushing her to do so, and since she is not a monetarist, she may have misjudged the quantity effects of tapering. Note that the growth rate of Divisia M4 - a broad measure of the money supply tracked by the Center for Financial Stability - has dropped to 2pc from 6.2pc in early 2013.

イェレン議長が例の過ちを繰り返すことはなさそうですが、彼女にそれを余儀なくさせるものは沢山ありまして、議長はマネタリストではないので、テーパリングの量的効果を間違ったかもしれません。

金融安定センターがトラッキングしているマネーサプライの広義の基準であるDivisa M4の伸び率が、2013年初頭の6.2%から2%まで下落したことは覚えておきましょう。

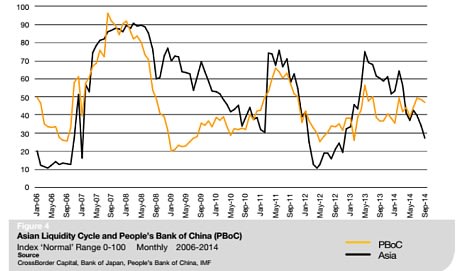

The Fed pivot comes at a delicate moment because China's (PBOC) is at the same time winding down stimulus, trying to tame China's $25 trillion credit monster before it is too late. The central bank has not yet blinked - beyond minor short-term liquidity shots - even though bad loans are rising fast at the big state banks.

中国人民銀行が手遅れになる前に中国25兆ドルの信用モンスターを抑え込もうと刺激を減らそうとしたのと同時、という微妙な時にFRBは方向転換しました。

不良債権が大手の国営銀行で急増しているにも拘らず、中国人民銀行は(ちょっとした短期的流動性注入以外)まだ動じていません。

China became a net seller of global bonds in the third quarter (even adjusting for currency effects). It was buying $35bn a month earlier this year.

中国は第3四半期、債券の売り手に回りました(為替調整後ですら)。

今年先には毎月350億ドルも買っていました。

The move was well-flagged in advance. Premier Li Keqiang said in May that excess foreign reserves had become a "burden" and were making it impossible for China to run a sovereign monetary policy. The policy shift automatically entails monetary tightening - vis-a-vis the status quo ante - unless China acts to sterilise the effects. It has not done so. We have seen a sudden stop in China's "proxy QE".

この動きは予めしっかり予告されていました。

李克強首相は5月に、過剰な外貨準備は「重荷」になって、中国が金融政策を実行するのを邪魔していると言いました。

中国が影響を不胎化しない限り、この政策転換は自動的に(以前の状態に対して)金融引き締めをもたらします。

僕らは中国の「代理QE」の急停止を目撃したわけです。

Brazil, Malaysia, Singapore and Thailand all cut their foreign reserves in the third quarter. Korea slashed net purchases from $25bn to $9bn, and India from $43bn to $12bn. Russia is now burning through its reserves to defend the rouble. Others oil states will have to do the same to cover their budgets.

ブラジル、マレーシア、シンガポール、タイはいずれも第3四半期に外貨準備を減らしました。

韓国は準買入額を250億ドルから90億ドルに減らし、インドは430億ドルから120億ドルに減らしました。

ロシアは今やルーブル防衛のために外貨準備を燃やしまくっています。

他の産油国も財政のために同じことをしなけりゃならなくなるでしょう。

Net bond stimulus by all the global central banks together has fallen by roughly $125bn a month since the end of last year, an annualised pace of $1.5 trillion. We have seen an abrupt halt to the $10.2 trillion of net reserve accumulation since 2000 that has played such a role in the asset boom of the modern era. That does not automatically mean asset prices will fall, but it removes a powerful tailwind.

昨年末以降、世界中の中銀による債券購入額は月に1,250億ドル程度ずつ減っています。

年間1.5兆ドルのペースで減っているわけです。

現代史上屈指の資産ブームであれほど大きな役割を果たした、2000年から10.2兆ドルにも上った準備金蓄積の急停止を目撃したわけです。

だからって資産価格が下がるってことじゃありませんけど、強力な追い風はなくなります。

Hopes that the Europe would pick up the QE baton to keep the asset boom going border on wishful thinking. The European Central Bank's balance sheet has contracted by almost ?150bn due to passive tightening since the Mario Draghi first spoke of buying asset-backed securities in June.

ヨーロッパがQEリレーのバトンを受け取って資産ブームを続けてくれるんじゃないか、なんて期待は希望的観測と紙一重です。

ECBのバランスシートは、マリオ・ドラギ総裁が6月にABS購入を初めて口にしてからこっち、受動的引き締めのおかげで1,500億ユーロ近く縮小したんですから。

There is much chatter from peripheral ECB governors, a talkative lot. Listen instead to Sabine Lautenschlager, Germany's member of the ECB's executive board. Her predecessor backed the Draghi rescue plan for Italy and Spain (OMT) in August 2012 against objections from the Bundesbank, and that is what made it possible.

周辺国からのECB理事はお喋りでごちゃごちゃ言ってます。

が、その代わりに、ドイツ人専務理事のサビーヌ・ラウテンシュレンガー専務理事の言葉に耳を傾けましょう。

彼女の前任は2012年8月にドイツ中銀の反対に歯向かってドラギOMTに賛成しまして、そのおかげで実行出来ました。

I may be wrong, but it strikes me as implausible that the ECB will risk launching QE on a massive scale as long as both German members are opposed. The bank can dabble at the edges, as it is doing now, but a reflation blitz requires German political assent.

僕が間違っているのかもしれませんけど、ドイツ人メンバーが反対する限りECBが大規模QEを開始するリスクを取るなんてあり得ないと思うんですよね。

ECBは今そうしてるみたいにお茶を濁すことは出来るでしょうけど、リフレ政策実施にはドイツからの政治的証人が要りますから。

So what is Dr Lautenschlager saying? "I take a more critical view of some areas of the ECB's unconventional measures. If we talk about large-scale purchase programmes of securitised assets, the so-called ABS plan, or even large-scale sovereign bond purchases - then I take a more critical view, because for me the balance between costs and needs is negative at the moment. Those are measures one uses as a last resort if deflation is visible and that is by no means the case."

というわけで、ラウテンシュレンガー博士はなんと仰っているのか?

「私はECBの異例の対策の一部について批判的見解である。いわゆるABSプランという大規模な金融資産購入プログラム、または大規模な国債購入について語るなら、私は一層批判的見解を持つ。なぜなら、私にとってコストとニーズのバランスは今のところネガティブだからである。デフレが明白となった場合に最後の手段として用いるべき対策であり、今は全くそのような場合ではない」

Draw your own conclusions.

各自、結論はお任せします。