米国の金融機関の問題を解決するために、国有化を求める声が日増しに高まっている様だ。以下、ちょっと長いが記事の主な部分を簡単に訳している。

国有化=株式価値の喪失、という痛みを伴わない時間稼ぎにより、日本的な長期の不況のリスクが高まりつつある状況で、今後が注目される。

○Nationalize the Banks! We're all Swedes Now

http://www.washingtonpost.com/wp-dyn/content/article/2009/02/12/AR2009021201602.html

日本の1990年代やアメリカの1930年代の様にならないためには銀行システムの国有化しかない。

The U.S. banking system is close to being insolvent, and unless we want to become like Japan in the 1990s -- or the United States in the 1930s -- the only way to save it is to nationalize it. ・・・・・

サブプライム住宅ローン1.2兆ドルに加え、商業用不動産ローン、消費者クレジットカード負債、ハイイールド債、レバレッジローン等の7兆ドルが、その多くの価値を失うリスクにさらされている。・・・・

The subprime mortgage mess alone does not force our hand; the $1.2 trillion it involves is just the beginning of the problem. Another $7 trillion -- including commercial real estate loans, consumer credit-card debt and high-yield bonds and leveraged loans -- is at risk of losing much of its value. Then there are trillions more in high-grade corporate bonds and loans and jumbo prime mortgages, whose worth will also drop precipitously as the recession deepens and more firms and households default on their loans and mortgages.

・・・・・・・・

金融機関の損失は計3.6兆ドル、米金融機関で半分の1.8兆ドルと予想。米銀行資産は1.4兆ドルしかなく、0.4兆ドル不足。

But if you think that $2 trillion is high, consider our latest estimates at the financial Web site RGE Monitor: They suggest that total losses on loans made by U.S. banks and the fall in the market value of the assets they are holding will reach about $3.6 trillion. The U.S. banking sector is exposed to half that figure, or $1.8 trillion. Even with the original federal bailout funds from last fall, the capital backing the banks' assets was only $1.4 trillion, leaving the U.S. banking system about $400 billion in the hole.

ガイスナーのプランは正しい方向だが、金融システムがまだ債務返済能力があるとの前提にたっており、問題の解決はできない。

Two important parts of Geithner's plan are "stress testing" banks by poring over their books to separate viable institutions from bankrupt ones and establishing an investment fund with private and public money to purchase bad assets. These are necessary steps toward a healthy financial sector.

But unfortunately, the plan won't solve our financial woes, because it assumes that the system is solvent. If implemented fairly for current taxpayers (i.e., no more freebies in the form of underpriced equity, preferred shares, loan guarantees or insurance on assets), it will just confirm how bad things really are.

国有化が唯一の手段。

Nationalization is the only option that would permit us to solve the problem of toxic assets in an orderly fashion and finally allow lending to resume. Of course, the economy would still stink, but the death spiral we are in would end.

Nationalization -- call it "receivership" if that sounds more palatable -- won't be easy, but here is a set of principles for the government to go by:

ステップ1は、債務返済能力のない銀行を特定すること(いちばんたいへん)。

First -- and this is by far the toughest step -- determine which banks are insolvent. Geithner's stress test would be helpful here. The government should start with the big banks that have outside debt, and it should determine which are solvent and which aren't in one fell swoop, to avoid panic. Otherwise, bringing down one big bank will start an immediate run on the equity and long-term debt of the others. It will be a rough ride, but the regulators must stay strong.

ステップ2は債務返済能力のない銀行を国有化する。株主は排除され、預金者、短期債権者を保護した後に、長期の債権者に割り当て。

Second, immediately nationalize insolvent institutions. The equity holders will be wiped out, and long-term debt holders will have claims only after the depositors and other short-term creditors are paid off.

国有化後、資産を良いものと悪いものにわけ、悪い資産は時価(価値が下がっていれば反映して)で評価。ここでガイスナーのいう民間資本が購入ということもある。 良い資産はIPOか戦略投資家に売却。

Third, once an institution is taken over, separate its assets into good ones and bad ones. The bad assets would be valued at current (albeit depressed) values. Again, as in Geithner's plan, private capital could purchase a fraction of those bad assets. As for the good assets, they would go private again, either through an IPO or a sale to a strategic buyer.

資産売却益は預金者、債権者にいったのち、残りは政府へ。

The proceeds from both these bad and good assets would first go to depositors and then to debt-holders, with some possible sharing with the government to cover administrative costs. If the depositors are paid off in full, then the government actually breaks even.

残ったすべての悪い資産を集めて、満期まで保有or国民の負担で売却

Fourth, merge all the remaining bad assets into one enterprise. The assets could be held to maturity or eventually sold off with the gains and risks accruing to the taxpayers.

・・・・・・

1992年、スウェーデンで同じような国有化の試み。

Nationalizing banks is not without precedent. In 1992, the Swedish government took over its insolvent banks, cleaned them up and reprivatized them. Obviously, the Swedish system was much smaller than the U.S. system. Moreover, some of the current U.S. financial institutions are significantly larger and more complex, making analysis difficult. And today's global capital markets make gaming the system easier than in 1992. But we believe that, if applied correctly, the Swedish solution will work here.

・・・・・・

○The Growing Chorus for Nationalization

http://www.calculatedriskblog.com/2009/02/growing-chorus-for-nationalization.html

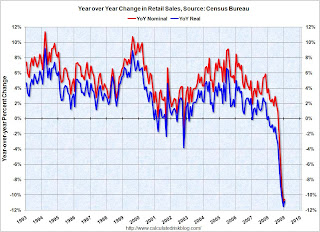

Click on graph for larger image in new window.

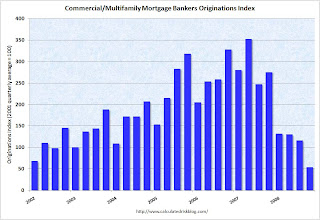

Click on graph for larger image in new window.

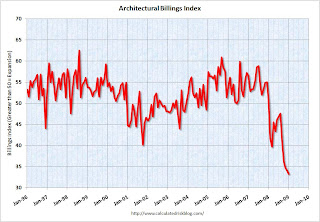

Click on graph for larger image in new window.

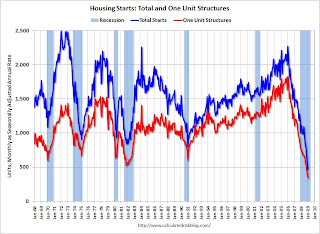

Click on graph for larger image in new window.