Fossil industry is the subprime danger of this cycle

(化石燃料業界はこのサイクルのサブプライム)

By Ambrose Evans-Pritchard

Telegraph: 9:03PM BST 09 Jul 2014

(化石燃料業界はこのサイクルのサブプライム)

By Ambrose Evans-Pritchard

Telegraph: 9:03PM BST 09 Jul 2014

The cumulative blitz on energy exploration and production over the past six years has been $5.4 trillion, yet little has come of it

この6年間にエネルギー資源の試掘や生産に投じた資金は5.4兆ドルに上りますが、殆ど実っていません。

The epicentre of irrational behaviour across global markets has moved to the fossil fuel complex of oil, gas and coal. This is where investors have been throwing the most good money after bad.

世界中の市場で見られる非論理的な動きの中心は、石油、ガス、石炭と言った化石燃料の複合体に移動しました。

これこそ投資家が失敗した事業に金をつぎ込んでいる場所です。

They are likely to be left holding a clutch of worthless projects as renewable technology sweeps in below radar, and the Washington-Beijing axis embraces a greener agenda.

再生可能エネルギーの技術がレーダーに捕捉されずに広がり、米中枢軸がよりエコな目標を受け容れる中で、彼らは価値のないプロジェクトを大量に抱えることになりそうです。

Data from Bank of America show that oil and gas investment in the US has soared to $200bn a year. It has reached 20pc of total US private fixed investment, the same share as home building. This has never happened before in US history, even during the Second World War when oil production was a strategic imperative.

バンク・オブ・アメリカのデータは、米国での石油ガス投資が年間2,000億ドルに急増したことを明らかにしています。

その割合は米国の民間設備投資の総額の20%と、住宅建設レベルに達しました。

これは米国史上初めてのことであり、石油生産が戦略的に不可欠だった第二次世界大戦中でもありませんでした。

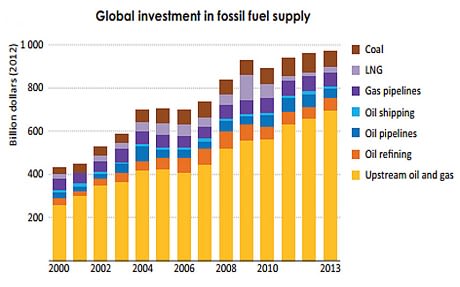

The International Energy Agency (IEA) says global investment in fossil fuel supply doubled in real terms to $900bn from 2000 to 2008 as the boom gathered pace. It has since stabilised at a very high plateau, near $950bn last year.

IEAは、化石燃料供給に対する国際的な投資はブームが加速する2000年から2008年までに、実質ベースで倍増して9,000億ドルに達したとしています。

その後は極めて高い水準で横ばいとなり、昨年は9,500億ドル近くとなりました。

The cumulative blitz on exploration and production over the past six years has been $5.4 trillion, yet little has come of it. Output from conventional fields peaked in 2005. Not a single large project has come on stream at a break-even cost below $80 a barrel for almost three years.

この6年間に化石燃料の試掘や生産に対して投じられた資金の額は5.4兆ドルに上っていますが、殆ど実っていません。

通常の油田からの生産は2005年にピークを迎えました。

ほぼ3年近くに亘って1バレル80ドルを下回る損益分岐点コストで操業するようになった大規模プロジェクトは一つもありません。

"What is shocking is that upstream costs in the oil industry have risen threefold since 2000 but output is up just 14pc," said Mark Lewis, from Kepler Cheuvreux. The damage has been masked so far as big oil companies draw down on their cheap legacy reserves.

「衝撃的なのは、石油産業の上流コストが2000年以降3倍に上昇したのに、生産はたったの14%しか増えていないことだ」とKepler Cheuvreuxのマーク・ルイス氏は言いました。

このようなダメージはこれまでのところ、大手石油グループが安価なレガシー・リザーブを取り崩しているので隠されているのです。

"They are having too look for oil in the deepwater fields off Africa and Brazil, or in the Arctic, where it is much more difficult. The marginal cost for many shale plays is now $85 to $90 a barrel."

「彼らはアフリカやブラジル、または北極圏といった深海の石油も探しているが、遥かに困難だ。多くのシェール・オイルの限界費用は今や1バレル85-90ドルだ」

A report by Carbon Tracker says companies are committing $1.1 trillion over the next decade to projects that require prices above $95 to break even. The Canadian tar sands mostly break even at $80-$100. Some of the Arctic and deepwater projects need $120. Several need $150. Petrobras, Statoil, Total, BP, BG, Exxon, Shell, Chevron and Repsol are together gambling $340bn in these hostile seas.

カーボン・トラッカーのレポートは、企業は今後十年間に、元を取るためには価格が95ドルを超えなければならないプロジェクトへ、1.1兆ドルを注ぎ込むつもりだとしています。

カナダの殆どのタール・サンドは80-100ドルが損益分岐点です。

北極圏や深海油田の一部は120ドルです。

ペトロブラス、スタトイル、トタル、BP、ブリティッシュ・ガス、エクソン、シェル、シェブロン、レプソルは総額3,400億ドルをこれらの荒海に投げ込んでいます。

Martijn Rats, from Morgan Stanley, says the biggest European oil groups (BP, Shell, Total, Statoil and Eni) spent $161bn on operations and dividends last year, but generated $121bn in cash flow. They faces a $40bn deficit even though Brent crude prices were buoyant near $100, due to disruptions in Libya, Iraq and parts of Africa. "Oil development is so expensive that many projects do not make sense," he said.

モルガン・スタンレーのMartijn Rats氏は、欧州屈指の石油グループ(BP、シェル、トタル、スタトイル、エニ)は昨年、オペレーションと配当に1,610億ドルを費やしたが、キャッシュフローは1,210億ドルしか生み出さなかったと言います。

これらの企業は、リビア、イラク、アフリカ各地の紛争により、ブレント原油の価格が1バレル100ドルという高水準に迫っていたにも拘わらず、400億ドルもの赤字に直面しています。

「石油開発は高価過ぎて、多くのプロジェクトはナンセンスになっている」そうです。

There are, of course, other candidates for the bubble prize of the current economic cycle, now into its 22nd quarter and facing the headwinds of US monetary tightening. China's housing boom has echoes of the Tokyo blow-off in 1989, and is four times more stretched than US subprime in 2006, based on price-to-incomes.

勿論、22期目に突入しつつあり、米国の金融引き締めという向い風に遭う今の経済サイクルの、バブル賞金を獲得しそうなところは他にもあります

中国の住宅ブームは1989年の東京のバブル崩壊を彷彿とさせますし、所得に対する住宅取得価格を基準にすると、2006年の米国サブプライム・バブルの4倍にも上っています。

The 2007-era vogue for Club Med sovereign bonds comes despite surging debt ratios, made worse by incipient deflation. This gamble is based entirely on the premise that Germany will let the European Central Bank print money a l'outrance, a political calculation that borders on wishful thinking.

2007年頃の地中海クラブ国債ブームは、債務比率の急上昇にも拘らずやって来た上に、デフレの予兆で悪化しました。

このギャンブルは、ドイツがECBに全面的量的緩和を許可するだろうという前提、つまり妄想紙一重の政治的計算に基づくものです。

Yet the sheer scale of "stranded assets" and potential write-offs in the fossil industry raises eyebrows. IHS Global Insight said the average return on oil and gas exploration in North America has fallen to 8.6pc, lower than in 2001 when oil was trading at $27 a barrel. What happens if oil falls back towards $80 as Libya ends force majeure at its oil hubs and Iran rejoins the world economy?

しかし、化石燃料産業の「棚卸資産」や潜在的不良債権の規模は驚くべきです。

IHSグローバル・インサイトによれば、北米での石油ガス試掘の平均利益率は8.6%であり、1バレル27ドルだった2001年当時よりも低くなっているとのこと。

リビアが石油ハブへの攻撃を止めてイランが国際経済に復帰して、石油価格が再び80ドルへと下落したらどうなるのでしょう?

A large chunk of US investment is going into shale gas ventures that are either underwater or barely breaking even, victims of their own success in creating a supply glut. One chief executive acidly told the TPH Global Shale conference that the only time his shale company ever had cash-flow above zero was the day he sold it - to a gullible foreigner.

米国の投資の殆どは、既にアンダーウォーターにあるか損益分岐点ぎりぎりで、供給過剰を生み出した独自の成功の犠牲になっているシェール・ガス事業に向かっています。

某CEOはTPHグローバル・シェール・コンファランスで、自分のシェール事業会社のキャッスフローがプラスだったのは会社を(バカな外国人に)売却した日だけだった、と憎々しげに言いました。

The Oxford Institute for Energy Studies says the Eagle Ford Dry Gas field, the Marcellus WC T2 and "C" Counties, Powder River, Cotton Valley, among others, are all losing money at the current Henry Hub spot price of $4.50. "The benevolence of the US capital markets cannot last forever," it said.

オックスフォード・エネルギー研究所によれば、イーグル・フォード・ドライ・ガス・フィールド、マーセラスWC T2とCカウンティ、パウダー・リバー、コットン・バレーなどはいずれも4.50ドルというヘンリーハブ・スポット価格では赤字だそうです。

「米資本市場の慈善にも限界がある」とのこと。

This does not mean shale has been a failure. Optimists still hope it will reach a "positive inflexion point" in five years or so, the typical pattern for a fledgling industry. Some drillers have switched to tight oil projects that are much more more profitable because crude is closely linked to global prices. Yet the low-hanging fruit has been picked and the costs are ratcheting up. Three Forks McKenzie in Montana has a break-even price of $91.

これはシェール・ガスが失敗だったと言っているのではありません。

楽観主義者は今も、新しい産業では典型的なパターンを辿って、5年ほどで「好ましい変曲点」に達するだろうという望みを持っています。

掘削業者の一部は、原油の方が国際価格と密接に関連しているため、遥かに大きな利益の出るタイト・オイル開発に切り替えました。

しかし容易に利益を出せるものは全て開発済みであり、コストは急上昇中です。

モンタナのスリー・フォークス・マッケンジーの採算価格は91ドルです。

Nor does it mean that America has made a mistake. Shale has been a timely shot in the arm, helping the US economy achieve "escape velocity" from the Great Recession, unlike Europe, which lurched back into a double-dip recession.

また、米国が間違ったということでもありません。

シェールは素晴らしいタイミングのカンフル剤であり、米国経済が大不況からの「脱出速度」に達するのを助けました。

二番底に転げ落ちたヨーロッパとは違います。

It has whittled down the US current account deficit, now just 2pc of GDP. Cheap gas costs - a third of EU prices and a quarter of Asian prices - has brought US industry back from near death, perhaps for long enough to give America another two decades of superpower ascendancy. But making money out of shale is another matter.

それは米国の経常赤字を減らし、今ではGDPの僅か2%です。

安価なガス(ヨーロッパの3分の1、アジアの半分の価格)により米国の産業は瀕死の状態から復活しました。

米国があと20年間、超大国でいられるだけの余裕を稼いだと思われます。

しかしシェールで儲けることは、また別の問題です。

Even if the fossil companies navigate the next global downturn more or less intact, they are in the untenable position of booking vast assets that can never be burned without violating global accords on climate change.

上記の化石燃料企業は、次の世界的不況をほぼそのままの状態で乗り切ったとしても、気候変動に関する国際協定に違反することなく燃やすことは出来ない膨大な資産を抱えるという、困難な状態にあります。

The IEA says that two-thirds of their reserves become fictional if there is a binding deal limit to CO2 levels to 450 particles per million (ppm), the maximum deemed necessary to stop the planet rising more than two degrees centigrade above pre-industrial levels. It crossed 400 ppm threshold this spring, the highest in more than 800,000 years.

IEAは、二酸化炭素排出量の上限を、産業革命以前からの気温上昇を2度を上回るのを阻止するために必要とされる限界である450ppmとする合意が結ばれれば、これらの企業の埋蔵量の3分の2はフィクションに終わるだろうとしています。

この春には80万年以上ぶり最高値の400ppmのラインを超えました。

"Under a global climate deal consistent with a two degrees centigrade world, we estimate that the fossil fuel industry would stand to lose $28 trillion of gross revenues over the next two decades, compared with business as usual," said Mr Lewis. The oil industry alone would face stranded assets of $19 trillion, concentrated on deepwater fields, tar sands and shale.

「世界の気温上昇を2度以内とする気候変動枠組条約下では、化石燃料産業の今後20年間の収益は、条約がない場合と比べて、28兆ドル少なくなると試算している」とルイス氏は言いました。

石油産業だけでも19兆ドルもの、深海油田、タールサンド、シェールに集中する棚卸資産を抱えることになるでしょう。

By their actions, the oil companies implicitly dismiss the solemn climate pledges of world leaders as posturing, though shareholders are starting to ask why management is sinking so much their money into projects with such political risk. This insouciance is courting fate. President Barack Obama's new Climate Action Plan aims to cut US emissions by 30pc below 2005 levels by 2030. His Clean Air Act is a drastic assault on coal-fired power plants, "industrial sabotage by regulatory means" in the words of the industry lobby.

石油企業はその行動によって、世界各国の首脳陣が立てた厳粛な気候変動の誓いを恰好だけのものだと暗に片付けてしまっているのですが、株主は何故経営陣が彼らの資金をそのような政治的リスクのあるプロジェクトにあれほど投じているのか問い始めています。

バラク・オバマ米大統領の気候行動計画は、米国の温暖化ガス排出量を2030年までに2005年の水準を下回るまでに削減することを目指しています。

また、業界が「規制による産業サボタージュ」と呼ぶ大気浄化法は、石炭火力発電所に対するドラスティックな攻撃です。

China too is trying to break free of coal after anti-smog protests across the cities of the Eastern Seaboard. It is shutting down its coal-fired plants in Beijing this year. There is a ban on new coal plants in key regions.

中国も東部沿岸部の都市全域で反スモッグ・デモが起こったことを受けて、石炭からの解放を目指しています。

今年は北京の石炭火力発電所を閉鎖しています。

主張地域では同発電所の新規建設を禁止しました。

The Communist Party's Five-Year Plan aims to cap demand at 3.9bn tonnes a year up to 2015. Since the country consumes half the world's coal supply, this has left Australia's coal industry high and dry, Exhibit number one of assets stranded by a sudden policy change. Peak coal demand is in sight.

中国共産党の五か年計画は、2015年までに年間需要量を39億トンに制限することを目標としています。

この国は世界の石炭供給量の半分を消費しているため、これによってオーストラリアの石炭産業は暗礁に乗り上げました。

突然の政策転換による棚卸資産の一つと言えるでしょう。

石炭需要のピークも見えてきました。

In any case, staggering gains in solar power - and soon battery storage as well - threatens to undercut the oil industry with lightning speed, perhaps in a race with cheap nuclear power from a coming generation of molten salt reactors. The US National Renewable Energy Laboratory has already captured 31.1pc of the sun's energy with a solar chip, but records keep being broken.

いずれにせよ、太陽光発電の驚くべき発展(間もなく電池もそうなるでしょう)は、恐らく溶融塩増殖炉の到来による安価な原子力発電との競争の中で、電光石火で石油産業を駆逐しようとしています。

米国立再生可能エネルギー研究所は既にソーラー・チップによって太陽光エネルギーの31.1%を捕らえましたが、記録は破られ続けています。

Brokers Sanford Bernstein say we are entering an era of "global energy deflation" where gains in solar technology must relentlessly erode the viability of the fossil nexus, since it goes only in one direction. Deep sea drilling will become pointless. We can leave the Arctic alone.

ブローカーズ・サンフォード・バーンスタインによれば、これは一方向にしか進まないため、太陽光テクノロジーが化石燃料の存続可能性を一貫して侵食する「グローバル・エネルギー・デフレ」時代に僕らは突入しつつあるのだそうです。

深海油田の掘削は無意味になります。

僕らは北極圏を放っておけるのです。

Once the crossover point is reached - and photovoltaic energy already competes with oil, diesel and liquefied natural gas in much of Asia without subsidies - it must surely turn into a stampede. My guess is that the world energy landscape will already look radically different in the early 2020s.

一線を越えてしまえば(太陽光エネルギーは既にアジアの大半で補助金もなしに石油、ディーゼル、LNGと競争していることですし)、確実に大きな流れとなるでしょう。

世界のエネルギー事情は2020年初頭には既に異次元的に違っているのではないかと思います。

Cheuvreux's Mr Lewis compares the big oil companies with European utilities caught off-guard 10 years ago by the switch to wind and solar, their survival in doubt, their share prices slashed by two-thirds since 2008. "The utilities told us that renewables would have no impact on their business models, and now they are facing an existential crisis," he said.

シュブルーのルイス氏は大手石油企業を、風力太陽光への切り替えに10年前に不意を突かれ、2008年以降株価が3分の2も下落して存続が怪しくなっているヨーロッパの公益企業になぞらえています。

「これらの公益企業は、再生可能エネルギーは自分達のビジネス・モデルに一切影響を与えないと我々に言っていたが、今や存亡の危機に直面している」とのこと。

BP's Lord Browne was derided for embracing solar and rebranding his company "Beyond Petroleum" in 2000. His successors repudiated his vision, famously going back to basics. He may have his moment of sweet vindication after all.

BPのロード・ブラウンは2000年に、太陽光エネルギーを受け容れて同社を「Beyond Petroleum(石油を超越する)」ようリブランドしたと嘲笑われました。

彼の後継者達は、良く知られているように基本に立ち戻って、彼のビジョンを否定しました。

結局、ロード・ブラウンは自分の正しさが証明される素晴らしい瞬間を楽しんでいるのかもしれません。