Oil slump leaves Russia even weaker than decaying Soviet Union

(石油値下がりでロシアが腐りかけソ連よりもヘロヘロになりそう)

By Ambrose Evans-Pritchard

Telegraph: 8:48PM BST 22 Oct 2014

(石油値下がりでロシアが腐りかけソ連よりもヘロヘロになりそう)

By Ambrose Evans-Pritchard

Telegraph: 8:48PM BST 22 Oct 2014

Russia had the chance at the end of the Cold War to build a modern, diversified economy, with the enthusiastic help of the West. That chance has been squandered

ロシアは冷戦の終わりに、西側から情熱的な支援を得て、現代的で多様な経済を築くチャンスを得ましたが、そのチャンスはスルーされてしまいました。

It took two years for crumbling oil prices to bring the Soviet Union to its knees in the mid-1980s, and another two years of stagnation to break the Bolshevik empire altogether.

1980年代中盤、石油の値下りがソ連を倒すまでに2年を要しました。

そしてボルシェビキ帝国を完全破壊するには、更に2年間の不況を要しました。

Russian ex-premier Yegor Gaidar famously dated the moment to September 1985, when Saudi Arabia stopped trying to defend the crude market, cranking up output instead. "The Soviet Union lost $20bn per year, money without which the country simply could not survive," he wrote.

ロシアのエゴール・ガイダル元首相がその瞬間を1985年9月と特定したことは有名です。

その時、サウジアラビアは原油相場防衛を停止して、代わりに増産に踏み切りました。

「ソ連は年間200億ドルの損失を出した。こんな損失ではどんな国もひとたまりもない」と同氏は記しました。

The Soviet economy had run out of cash for food imports. Unwilling to impose war-time rationing, its leaders sold gold, down to the pre-1917 imperial bars in the vaults. They then had to beg for "political credits" from the West. That made it unthinkable for Moscow to hold down eastern Europe's captive nations by force, and the Poles, Czechs and Hungarians knew it.

ソ連経済は食糧を輸入するための現金を使い尽くしてしまいました。

戦時中の配給制を実施するのを躊躇して、当時の指導部は金庫にあった1917年以前の帝政時代の金の延べ棒まで売り払いました。

そして西側に「政治的信用」を乞いました。

それによってモスクワが武力で東欧を抑え込み続けることはあり得なくなりました。

ポーランド、チェコ、ハンガリーはそれをわかっていました。

"The collapse of the USSR should serve as a lesson to those who construct policy based on the assumption that oil prices will remain perpetually high. A seemingly stable superpower disintegrated in only a few short years," he wrote.

「石油価格はずっと高止まりするという過程に基づいて政策を作る人間にとって、ソ連の崩壊は教訓になるはずである。一見安定した超大国は僅か数年間で瓦解した」と元首相は書きました。

Lest we engage in false historicism, it is worth remembering just how strong the USSR still seemed. It knew how to make things. It had an industrial core, with formidable scientists and engineers.

間違ったヒロイズムに拘わらないように、兎にも角にもどれほどソ連が今も強固に見えたかを覚えておく価値はあります。

物作りの仕方を知っていました。

無敵の科学者と技術者を備えた産業基盤もありました。

Vladimir Putin's Russia is a weaker animal in key respects, a remarkable indictment of his 15-year reign. He presides over a rentier economy, addicted to oil, gas and metals, a textbook case of the Dutch Disease.

ウラジーミル・プーチン露大統領が君臨した15年間の驚くべき非難ですが、ロシアは大事な部分で弱い生き物です。

彼は金利生活経済を仕切り、石油・ガス・金属中毒になり、オランダ病の典型です。

The IMF says the real effective exchange rate (REER) rose 130pc from 2000 to 2013 during the commodity super-cycle, smothering everything else. Non-oil exports fell from 21pc to 8pc of GDP.

IMFは、REERは2000年から2013年までの資源スーパーサイクル中に130%も上昇し、他のありとあらゆるものを押し潰したとしています

石油以外の輸出はGDPの21%から8%まで減少しました。

"Russia is already in a perfect storm," said Lubomir Mitov, Moscow chief for the Institute of International Finance. "Rich Russians are converting as many roubles as they can into foreign currencies and storing the money in vaults. There is chronic capital flight of 4pc to 5pc of GDP each year but this is no longer covered by the current account surplus, and now sanctions have caused foreign capital to turn negative, too."

「ロシアは既に嵐の真っ只中だ」と国際金融研究所のモスクワ支部長、Lubomir Mitov氏は言いました。

「金のあるロシア人は出来る限り沢山のルーブルを外貨に換えて、その金を金庫にしまい込んでいる。毎年GDPの4-5%に上る資本逃避が慢性的になっている。だが、これはもう経常黒字では埋められない。今や制裁によって外貨資本はマイナスにもなっている」

"The financing gap has reached 3pc of GDP, and they have to repay $150bn in principal to foreign creditors over the next 12 months. It will be very dangerous if reserves fall below $330bn," he said.

「財政の穴はGDPの3%に達した。今後12ヶ月間に海外の債権者に1,500億ドルの元本を返済しなければいけない。準備高が3,300億ドルを切ったら非常にまずいことになる」

"The benign outcome is a return to the stagnation of the Brezhnev era [Застой in Russian] in the early 1980s, without a financial collapse. The bad outcome could be a lot worse," he said.

「金融破綻が起こらずに1980年代初頭のブレジネフ時代の不況に逆戻りするならマシな結果だ。悪い結果になれば、それよりも遥かに酷い事態になるかもしれない」

Mr Mitov said Russia is fundamentally crippled. "They have outsourced their brains and lost their technology. The best Russian engineers go to work for Boeing. The Russian railways are run on German technology. It looked as if Russia was strong during the oil boom but it was an illusion and now they are in an even worse position than the Soviet Union," he said.

Mitov氏は、ロシアは根本的にボロボロなのだと言いました。

「連中は頭脳をアウトソースして技術をなくしてしまった。ロシア屈指のエンジニアはボーイングに働きに行っている。ロシアの鉄道はドイツの技術で動いている。ロシアは石油ブームの間は強く見えたが、それは幻で、今やソ連の時よりも更に酷い状況にあるようだ」

The Saudi drama of 1985 has powerful echoes today. We do not know exactly why the Saudis decided to drive down the oil price, though they were clearly frustrated by OPEC cheating, and needed extra revenue themselves.

1985年のサウジアラビア事件は今日もしっかり後を引いています。

サウジアラビアがなんだって石油価格を押し下げることにしたのか、正確にはわかりませんが、OPECの詐欺にムカついていたのは明らかですし、彼ら自身、追加収入が必要でした。

Ronald Reagan biographer Paul Kengor says the chief motive was to nurture their strategic alliance with Washington, doing a favour for the US at an inflexion point in the Cold War. The former President's son, Michael Reagan, makes the same claim. "My father got the Saudis to flood the market with cheap oil," he said. The plans were allegedly hatched by CIA Director William Casey.

ロナルド・レーガン元大統領の伝記を記したポール・ケンゴー氏は、米政府との戦略的結び付きを作りたかったというのが主な動機で、そのために冷戦の転換点で米国のためになることをしたのだろうと言います。

元大統領の息子であるマイケル・レーガン氏も同意見です。

「父はサウジアラビアに安い石油でマーケットをじゃぶじゃぶにさせたんだ」とか

この計画はCIAのトップだった、ウィリアム・ケイシー氏が考案したと言われています。

By then President Reagan was spending 6.6pc of GDP on defence and building his 15 aircraft carrier battle groups (never quite achieved), inviting ruinous attempts by the USSR to keep up.

その頃までに、レーガン大統領はGDPの6.6%もの軍事費を費やして、15もの空母航空団を作りつつ(完成はしませんでした)、破滅に導く軍拡競争をロシアにさせたのです。

The "Reagan Doctrine" twisted the knife further by backing guerrilla insurgencies against Soviet client states: in Afghanistan, Nicaragua and Angola, among others. The Pentagon's rule of thumb was that it cost Moscow 10 times as much to defend these regimes as it cost Washington to take pot shots. Hawk anti-aircraft missiles were cheap. Soviet MIG 24 helicopters were expensive.

「レーガン・ドクトリン」は、アフガニスタン、ニカラグア、アンゴラなどソ連の手下の国々に対するゲリラ活動を支援することで、更にダメージを広げました。

国防総省の鉄則は、これらの体制を護るソ連に、米政府が狙い撃ちにかける費用の10倍の額を費やさせることでした。

ホーク地対空ミサイルは安価でした。

ソ連のMIG24ヘリコプターは高価でした。

The Saudis were again helpful. They bankrolled the Nicaraguan Contras when House Democrats cut off funding, quietly paying for an off-books operation by US intelligence. The go-between was Prince Bandar bin Sultan, then Saudi ambassador in Washington.

ここでもサウジアラビアが助けてくれました。

民主党が下院の過半数を握っている時、米国情報部の秘密活動費を密かに出して、ニカラグア戦の資金を融通してくれました。

仲介人は当時駐米大使だったバンダル・ビン・スルタン王子でした。

This is the same Prince Bandar - later head of the Saudi secret service - who spent four hours with Mr Putin last year at his dacha outside Moscow. A transcript of their talk was leaked by the Kremlin, in order to embarrass Riyadh. It suggests that the prince offered Russia a deal to carve up global oil and gas markets, but only if it sacrificed Syria's Assad regime. He purported to speak with the full backing of Washington.

その後、サウジアラビア情報部のトップを務めたバンダル王子にとっても同じでした。

彼は昨年、モスクワ郊外にある別荘でプーチン大統領と4時間に及ぶ会談を行いました。

その内容はロシア政府によってサウジアラビア政府を困らせるためにリークされました。

それによれば、シリアのアサド政権を生贄に出せば、世界中の石油ガス市場を分割してやる、という取引を王子はロシアに持ちかけたようです。

王子は、米政府からの全面的な支援を得て話していると主張しました。

While nothing came of the meeting, it gives a glimpse into the raw geopolitics of oil. It explains why they think the worst in Moscow today as the Saudis cheerfully shrug off a 24pc plunge in Brent crude prices since June. "This is political manipulation, and Saudi Arabia is being manipulated, which could end badly," said Mikhail Leontyev from Russia's oil arm, Rosneft.

会談から得るものは何もありませんでしたが、これは石油地政学の内情を垣間見せています。

ブレント原油の価格が6月以降24%も暴落したこともサウジアラビアが易々と一蹴しながら、モスクワでは最悪の事態を想定している理由がわかります。

「これは政治的な操作だ。サウジアラビアは操られている。酷い結果になるかもしれない」とロスネフチのMikhail Leontyev氏は言います。

Events never repeat themselves. The Saudis lack the spare capacity these days to dictate prices with 1980s panache. They have their own pain threshold. Their welfare blitz since the Arab Spring has run to $130bn. The Shia minority in the Eastern Province has a score to settle, and they are sitting on the giant oil fields.

何もなしに事件が繰り返されることはありません。

最近のサウジアラビアには1980年代の勢いで価格を操作する余力がないのです。

サウジアラビアにはサウジアラビアの限界があります。

アラブの春以降に社会福祉に注ぎ込んだ資金は1,300億ドルに上っています。

東部の少数派、シーア派には晴らすべき恨みがある上に、巨大な油田を抱えています。

Brent oil has settled at around $85 a barrel. Deutsche Bank said the "break-even price" for the Saudi budget is $99, rising to $100 for Russia and Oman, $126 for Nigeria, $136 for Bahrain and $162 for Venezuela. There is a widely-held view that the Saudis are bluffing in order to force the rest of OPEC to agree to output cuts. If so, we will find out in November.

ブレント原油の価格は大体85ドルです。

ドイチェ・バンクによれば、サウジアラビアの財政「損益分岐点」は99ドルで、ロシアとオマーンはそれを上回る100ドル、ナイジェリアは126ドル、バーレーンは136ドル、ベネズエラは162ドルだそうです。

まことしやかに言われているのは、サウジアラビアは他のOPEC加盟国に減産を合意させようとはったりをかましているということです。

だとすれば、11月にはわかるでしょう。

What is clear is that the Saudis can withstand two or even three years at the current price by dipping into their $745bn foreign exchange reserves. This would have the added bonus (for them) of chilling fresh shale ventures, and perhaps killing some deep water forays in the Atlantic.

はっきりしているのは、サウジアラビアは7,450億ドルも貯め込んだ外貨準備に手を付けることで、今の価格を2年、はたまた3年は耐えられるということです。

これには新しいシェール事業を冷え込ませ、上手くすれば大西洋での深海油田開発も幾つか潰せるかもしれない、という(彼らにとっての)おまけも付きます。

Whatever the Saudi motive, Russia is already reeling. The central bank governor Elvira Nabiulina told the Duma last week that plans are afoot to cope with a protracted slide in oil prices to $60. "We are working on a stress scenario, an emergency scenario so to speak," she said.

サウジアラビアの動機がなんであれ、ロシアは既に倒れつつあります。

ロシア中銀のエルヴィラ・ナビウリナ総裁は先週下院で、石油価格が60ドルまで長期的に落ち込んでも耐えられる計画が進行中だと発言しました。

「ストレス・シナリオ、いわゆる緊急事態対策をまとめている」とのこと。

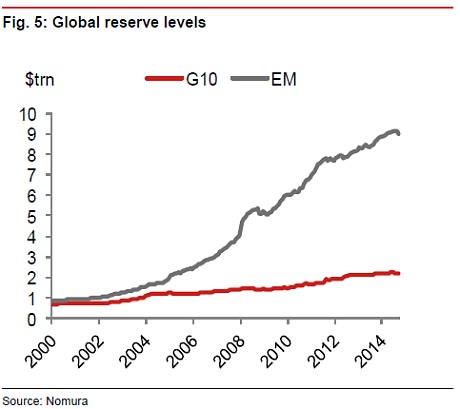

Moody's said the central bank has burned through $60bn of foreign reserves since the end of last year propping up companies starved of dollar liquidity. The total has dropped to $396bn on its estimates (leaving aside the Reserve Fund) and is becoming a sovereign credit risk.

ムーディーズによれば、ロシア中銀は昨年末以来、600億ドルも外貨準備をドル不足に苦しむ企業を支えるために注ぎ込んだそうです。

その試算によれば(予備基金を除く)残高は3,960億ドルまで減っており、ソブリン・クレジット・リスクになりつつあります。

This time Russia is not facing Reaganesque rearmament, but it is facing nuclear-tipped sanctions, more destructive than many realise in a globalised banking system. It is not a stretch to say that American regulatory power has never been so far-reaching, or imperial. The result is that Russian banks, companies and state bodies are shut out of the global capital markets, unable to roll over $720bn of external debt.

今回、ロシアはレーガン時代の軍拡競争には直面していませんが、グローバル化した金融システムにおいては多くの人が理解しているよりも破壊力のある強烈な制裁に直面しています。

米規制当局の力がここまで広がったこと、またはここまで絶大になったことはないと言っても言い過ぎではありません。

その結果が、ロシアの銀行、企業、政府機関の国際資本市場出金措置と、7,200億ドルの外債ロールオーバー不可なのです。

Russia's reserves of cheap crude in West Siberian fields are declining, yet the Western know-how and vast investment needed to crack new regions have been blocked. Exxon Mobil has been ordered to suspend a joint venture in the Arctic. Fracking in the Bazhenov Basin is not viable without the latest 3D seismic imaging and computer technology from the US. China cannot plug the gap.

シベリア西部の安価な原油の埋蔵量は減少中ですが、西側のノウハウや新規開発に必要な巨額の投資は手に入りません。

エクソン・モービルは北極圏での合弁事業を停止するよう命じられました。

バジェノフ油田でのフラッキングは、米国の最新の3D地震反射法やコンピューター技術なくして実現不可能です。

中国が穴を埋めることは出来ません。

Andrey Kuzyaev, head of Lukoil Overseas, said it costs $3.5m to drill a 1.5 km horizontal well-bore in the US, and $15m or even $20m to drill the same length in Russia. "We're lagging by 10 years. Our traditional reserves are being exhausted. This is the reality for our country," he said.

ルークオイル・オーバーシーズのアンドレイ・クズヤエフ会長は、米国で1.5㎞の水平抗井を掘ろうと思ったら350万ドルかかるが、ロシアで同じ長さを掘るなら1,500万ドル、もしかすると2,000万ドルもかかると言いました。

「10年遅れてるんだ。昔からの油田は枯れつつある。これがロシアの現実だよ」

Lukoil warns that Russia could ultimately lose a quarter of its oil output if the sanctions drag for another two or three years.

ルークオイルは、制裁があと2-3年続けば、ロシアの石油生産量は最終的に4分の1減ることになりかねないと警告しています。

The IMF's latest "Article IV" report on Russia is an acid verdict on the Putin era. Product market barriers are the worst of any large country in the world. The economy is a tangle of bottlenecks. Russia's development model has "reached its limits".

IMFのロシアに関する「4条協議」最新版は、プーチン時代に対する辛辣極まりない判決です。

生産物市場の障壁は世界主要国中最悪です。

経済はボトルネックだらけです。

ロシアの発展モデルは「限界に達した」のです。

For details, try the World Economic Forum's index of competitiveness. Russia ranks 136 for road quality, 133 for property rights, 126 for the ability of firms to absorb technology, 124 for availability of the latest technology, 120 for the burden of government regulation, 119 for judicial independence, 113 for the quality of management schools, 107 for prevalence of HIV, 105 for product sophistication, 101 for life expectancy and 56 for quality of maths and science education. This is the profile of decline.

細かいところを見るなら、世界経済フォーラムの競争力ランキングでしょう。

ロシアは道路状態で136位、財産権で133位、起業の技術吸収力で126位、最新技術力で124位、政府規制の負担で120位、司法の独立性で119位、マネジメント・スクールの質で113位、HIV流行で107位、製品の洗練性で105位、寿命で101位、理数系教育の質で56位です。

これは衰退のプロフィールです。

Russia had a window of opportunity at the end of the Cold War to build a modern, diversified economy, with the enthusiastic help of the West, before the ageing crisis hit and the workforce began shrink by 1m a year. This chance has been squandered. Mr Putin's rash decision to pick a fight with the democratic world has made matters infinitely worse. Cheap oil could prove to be the death knout.

ロシアには冷戦の終わり、高齢化危機が本格化して労働力が毎年100万人ずつ減少する前に、現代的で多様な経済を西側からの熱心な支援を得て築くチャンスがありました。

このチャンスは無駄にされてしまいました。

民主的な世界と喧嘩するというプーチン大統領の拙速な決断によって、事態はどうしようもないほど悪化しました。

安い石油がとどめになるかもしれません。