Fed kicks off global dollar squeeze as Janet Yellen turns hawkish

(イェレン議長タカ化でFRBが世界的ドル引き締めを始動)

By Ambrose Evans-Pritchard

Telegraph: 9:00PM BST 16 Jul 2014

(イェレン議長タカ化でFRBが世界的ドル引き締めを始動)

By Ambrose Evans-Pritchard

Telegraph: 9:00PM BST 16 Jul 2014

A vast wash of dollars flooded the global financial system when the Fed cut rates near zero and then bought $3.5 trillion of bonds. This may now go into reverse

FRBがゼロ金利に突入して3.5兆ドルもの債券買入をやったら、世界中の金融システムが膨大なドルでジャブジャブになりました。これが今、逆転するかもしれません。

The US Federal Reserve has begun to pivot. Monetary tightening is coming sooner than the world expected, with sober implications for overheated bourses, and for those in Asia, eastern Europe and Latin America that drank deepest from the draught of dollar liquidity.

FRBが方向転換を開始しました。

金融引き締めは世界の予想よりも前倒しされそうです。

過熱した株式市場にとっては冷や水であります。

また、ドル流動性を一番がぶ飲みしちゃったアジア、東欧、ラテン・アメリカの株式市場もご同様です。

We can expect a blistering dollar rally, perhaps akin to the early 1980s or the mid-1990s. It is fortuitous that the BRICS quintet of Brazil, Russia, India, China and South Africa have just launched their $100bn monetary fund to defend each other's currencies. Some of them may need it.

猛烈なドルの爆上げが予想されますね。

1980年代初頭とか1990年代中盤みたいな感じかな。

ブラジル、ロシア、インド、中国、南アフリカのBRICSカルテットがそれぞれの通貨を防衛しようと、1,000億ドルの基金を発足したばっかってのは偶然ですよ。

ちょっと必要になるかもしれないし。

America's unemployment rate has fallen from 7.5pc to 6.1pc in 12 months. The country has been adding 230,000 jobs a month in the first half of this year.

米国の失業率は12ヶ月間で7.5%から6.1%まで下落しました。

この国は上半期に毎月23万人ずつ雇用を増やしてきたわけです。

Since Fed chief Janet Yellen targets jobs above all else, this was bound to force capitulation by the Fed before long. It happened this week in her testimony to Congress. "If the labour market continues to improve more quickly than anticipated, then increases in the federal funds rate likely would occur sooner and be more rapid than currently envisioned," she said.

FRBのジャネット・イェレン議長は何よりも雇用をターゲットにしているわけで、だからこれは遠からずFRBを降伏させる運命にあったわけです。

で、それは今週に彼女が行った議会証言の中で起こりました。

「労働市場が予想よりも早く改善し続けるのであれば、FF金利もより速く上昇する可能性が高く、現在想定されているよりも急速にそうなる可能性が高い」んだそうで。

This is a policy shift. Mrs Yellen has admitted that the Fed misjudged the pace of jobs recovery. The staff did not expect unemployment to fall this low until late next year. The inflexion point has come 15 months early.

これは政策転換であります。

FRBは雇用回復のペースを読み誤った、とイェレン議長が認めたのです。

中の人達は失業率がここまで下がることは来年下旬までなかろうと思っていたんですね。

転換点は15ヶ月前に訪れました。

To some it feels like 2004, when the Greenspan Fed found itself badly behind the curve, suddenly switching from nonchalance in May to rate rises in June. "They may have left it too late again: the risk is a reckoning point when rates rise abruptly," said Jens Nordvig, from Nomura.

一部の人は2004年みたーいと思っています。

グリーンスパンFRBが無茶苦茶後手後手に回っていることに気付いて、5月のぼけーっとした状態から6月には突然利上げに踏み切ったアレです。

「また手遅れじゃん。金利が突然上がって審判の日なんてことにならなきゃいいけどさ」と野村證券のイェンス・ノードヴィグ氏は言います。

Mrs Yellen added the usual caveats about "false dawns". Wages are barely rising. The jobs market is not yet drawing back the millions who dropped out of the system. The labour participation rate is still stuck at a 36-year low of 62.8pc, and at the lowest ever recorded for men. "The recovery is not yet complete. We need to be careful to make sure the economy is on a solid trajectory before we consider raising interest rates," she said.

イェレン議長はいつもの「あてにならない期待」警告も付け加えました。

賃金は殆ど上がっていません。

労働市場はまだドロップ・アウトした数百万人を取り戻していません。

労働参加率は相変わらず36年ぶり最低の62.8%のまんま、男性に至っては史上最低のまんまです。

「景気回復は未だ完全ではない。利上げを検討する前に、経済が確実に軌道に乗ったことを慎重に確認する必要がある」と議長は言っています。

Yet she has undoubtedly changed gear. She no longer dismissed rising inflation (1.8pc) as "noise". She said share prices for biotech and social media companies were overheating, and that junk bonds were frothy. "Valuations appear stretched. We are closely monitoring developments in the leveraged loan market," she said.

でも議長がギア・シフトしたのは間違いないありません。

もう物価上昇(1.8%)を「ノイズ」なんてスルーしてませんし。

バイオとソーシャル・メディア関連銘柄の株価がオーバーヒートしている、ジャンク債はフロスだ、と仰ってます。

「バリュエーションが行き過ぎているように見受けられる。レバレッジ・ローン・マーケットの展開に注目している」とか。

The critics may be getting to her. The Bank of International Settlements has rebuked the Fed for stoking asset bubbles. Some of her own voting committee are fretting. "I think we are going to overshoot on inflation," said St Louis Fed chief James Bullard.

批判が効いてるのかも…。

BISは資産バブルを煽りやがってとFRBをボロカスに言ってますし。

連銀の委員連中もやきもきしてますし。

「インフレのオーバーシュートになると思ってるよ」とセントルイス連銀のジェームズ・ブラード総裁は言いました。

Mrs Yellen is not as dovish as believed, in any case. Her lodestar is the "non-accelerating inflation rate of unemployment" (NAIRU), the point at which tight labour markets start to drive a wage-price spiral. She thinks this is near 5.4pc.

いずれにせよ、イェレン議長は思われていたほどハト派じゃなかったんですね。

彼女の指針は、厳しい労働市場が賃金物価スパイラルを動かすポイント、「インフレ非加速的失業率(NAIRU)」ですから。

議長の考えだとこれは5.4%くらいだそうで。

When the rate is above NAIRU, she is a dove: when below, she is a hawk. She was one of the first to call for pre-emptive rate rises in 1996 to choke inflation, dissenting from the Greenspan Fed. Nobody thought of her as dovish then.

それがNAIRU以上の時はハトなんですな。

下回るとタカになる。

1996年にインフレを防ぐための先制的利上げを最初に言い出した、グリーンスパンFRBに反旗を翻す連中の一人でしたからね。

当時は彼女をハトだなんて誰も思ってませんでしたよ。

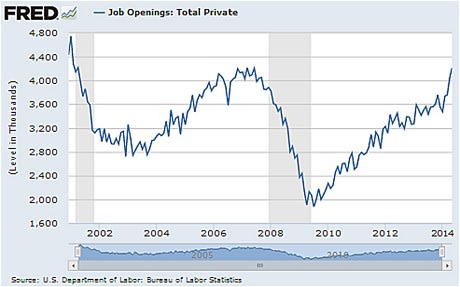

Her argument until now is that most of the jobless surge since the Great Recession is "cyclical and not structural" and therefore treatable by monetary stimulus. This is wearing thin. Skill shortages are cropping up everywhere. A Manpower survey of US firms found that 40pc are having trouble filling jobs. Total job openings have rocketed from 3.5m to 4.2m since January, the steepest rise in modern times.

議長が今まで言ってきたのは、大不況以降の失業者急増の大半は「景気循環的なものであって構造的なものじゃない」、だから金融刺激で手当て可能だということでした。

これが終わりかけてるんですね。

技術不足はそっこらじゅうで起こってます。

マンパワーが行った米企業調査では、40%の企業が採用に悪戦苦闘していることがわかりました。

求人数は1月以降に350万人から420万人に急増してまして、これは現代史上最も急激な伸びであります。

Quantitative easing has done its job, keeping growth alive as Congress and the White House pushed through the most draconian fiscal squeeze since the end of the Korean War. The economy did not fall back into recession, though it came close. It has achieved "escape velocity", of sorts.

QEは役目を終えたんですね。

議会とホワイトハウスが朝鮮戦争の終結以降、最も厳しい財政引き締めをやり通す中でも成長を維持したんですから。

米国経済は不況に舞い戻りませんでしたし…やばかったけど。

或る種の「脱出速度」に達しました。

Yet if America is strong enough to withstand rate rises, it is far from clear what this will do to the rest of the world. A vast wash of dollars flooded the global financial system when the Fed cut rates near zero and then bought $3.5 trillion of bonds. This may now go into reverse.

でも、米国が利上げに耐えられるほど強いんなら、これがその他の国々にはどうよってのは殆どわかりません。

FRBがゼロ金利に踏み切って3.5兆ドルもの債券買入を行った時、世界の金融システムは莫大なドルでジャブジャブにされました。

これが今、逆転するかもしれないわけで。

We still live in a dollarised world. Charles de Gaulle railed against the "exhorbitant privellege" of US dollar hegemony in the 1960s, but remarkably little has changed since. The BIS says global cross-border lending by banks alone has risen from $4 trillion to $10 trillion over the past decade, and $7 trillion of this is denominated in dollars. This does not include the dollar bond markets.

僕らは今もドル覇権世界に生きています。

シャルル・ド・ゴール将軍は1960年代に米ドル覇権の「法外な優越性」に文句を言いましたが、それ以降、驚くほどほとんど何も変わっていません。

BISは、銀行の国際融資だけでも過去10年間に4兆ドルから10兆ドルまで増大した上に、この内の7兆ドルはドル建てだと言っています。

これ、ドル建て債券市場抜きですよ。

What Fed now does arguably has more amplified effects than at any time since the end of gold and the collapse of the fixed-exchange Bretton Woods regime in 1971. This is the paradox of 21st century globalisation.

今、FRBがやらかすことはほぼ間違いなく、1971年に金本位制が逝ってブレトンウッズ体制がぶっ壊れて以降のどの時よりも、でっかい影響があるわけです。

これこそが21世紀のグローバリゼーションの矛盾ですよ。

Much of the dollar business is conducted through European and UK banks, leaving them acutely vulnerable to a dollar squeeze. Such episodes can be ferocious. It was a dollar liquidity shock that turned the Lehman affair into a global banking crisis, instantly engulfing Europe in October 2008.

ドル・ビジネスの大半は欧州や英国の銀行を通じて行われていまして、おかげでこの連中はドル不足に無茶苦茶弱いわけです。

おっそろしいことになりかねませんよ。

リーマンの破綻を世界的な銀行危機に変身させたのは、ドル流動性ショックだったんですからね。

2008年10月、こいつはヨーロッパを一飲みにしましたでしょ。

Emerging markets went into a tailspin last year at the first suggestion of Fed bond tapering. There was a sudden stop in capital flows. The "Fragile Five" (India, Indonesia, South Africa, Brazil and Turkey) were punished for current account deficits. The Fed backed down. The storm passed.

新興市場なんて、去年、FRBが債券買入規模縮小を口にした途端にキリキリ舞いになったし。

資本の流れがいきなり止まったんですから。

「脆弱ファイブ」(インド、インドネシア、南アフリカ、ブラジル、トルコ)は経常赤字のお仕置きをされましたしね。

この嵐は去りました。

There was a second "taper tantrum" earlier this year as the Fed finally began to pair back its $85bn monthly purchases under QE3. This too settled down. Those like India and Mexico that took advantage of the calm last Autumn to boost their defences were largely unscathed. Mrs Yellen has since recruited Bank of Israel veteran Stanley Fischer to be her number two, partly to navigate the reefs of emerging markets.

今年先にはQE3の850億ドル/月債券買入を遂に縮小し始めて、第二次「QE縮小爆弾」が弾けましたね。

この嵐も去りました。

去年の秋の凪を利用して護りを固めたインドとメキシコは概ね無事でした。

イェレン議長はその後、イスラエル中銀のベテラン、スタンレー・フィッシャー氏を右腕に迎えましたが、これは新興市場の岩礁を進むためでもありました。

However, that is not the end of story. A study by the International Monetary Fund concluded that the Fed's QE had pushed $470bn into emerging markets that would not otherwise have gone there. IMF officials say nobody knows how much of this hot money will come out again, or how fast.

でもそれで終わりじゃないんですね。

IMFの研究は、FRBのQEは4,700億ドルも新興市場にぶち込んだけど、FRBがQEをやってなかったら新興市場なんかに向かわなかった、との結論です。

中の人言わく、このホットマネーが幾ら流れ出して来るのか、どれだけのスピードで流れ出して来るのか誰もわからん、とのこと。

The BIS in turn said in its annual report two weeks ago that private companies had borrowed $2 trillion in foreign currencies since 2008 in emerging economies, lately at a real rate of just 1pc. Loans to Chinese companies have tripled to $900bn - some say $1.2 trillion - mostly through Hong Kong and often disguised by opaque swap contracts in what amounts a dangerous carry trade. Countries do not borrow in dollars any longer (mostly) but their banks and industries certainly do.

で、BISは2週間前に出した年次報告書の中で、新興国では民間企業が2008年以降、2兆ドルもの外貨建て融資を借り入れており、最近の実質金利はたったの1%だったと述べています。

中国企業への融資は3倍の9,000億ドルに達しており(1.2兆ドルって言ってる人もいますけどね)、その大半は香港経由でしかも危険なキャリートレードと言える怪しげなスワップ契約によって借りられています。

政府はもうドル建て借金なんて(ほとんど)しませんけど、銀行やら企業は確実にやってます。

The report said monetary largesse in the West has destabilised emerging economies in all kinds of ways. One of the worst - and least understood - ways is that they were forced to choose between internal credit bubbles or surging currencies. Most opted for bubbles as the lesser evil, holding their domestic interest rates at 300 basis points below the safe "Taylor Rule" level.

このレポートによれば、西側の金融緩和がありとあらゆる形で新興国を不安定化したんだそうですよ。

一番酷い(上に一番理解されていない)形は、これが国内の信用バブルか通貨急騰の二者択一を迫ったことなんだそうで。

殆どの新興国はバブルの方がマシだとこっちを選んで、国内の金利を安全「テイラー・ルール」水準より300BPも低いところに据え置いちゃったっていう。

This has driven their total debt levels to a record 175pc of GDP. It may be even worse. China has thrown all caution to the wind, pushing credit from $9 trillion to $25 trillion since Lehman. Its debt levels have reached 220pc by some estimates. Officials at both the IMF and the BIS privately doubt whether China can extricate itself smoothly from this.

これで連中の債務レベルがGDPの175%なんて史上最高値を達成することになりました。

もっと酷いかもしれませんね。

中国なんてなりふり構わずで、リーマン危機からこっち、信用残高を9兆ドルから25兆ドルまで膨れ上がらせましたでしょ。

債務レベルは220%到達なんて言う人もいますね。

IMFとBISの中の人がオフレコで言うには、中国がこれを難なく抜け出せるかどうか怪しいもんだよねとのこと。

Not all emerging markets are in the same boat. It is meaningless to compare Poland or the Czech Republic with Nicaragua. Yet there is no denying that a long string of countries are in structural crisis, ensnared by the middle-income trap. They have exhausted the low-hanging fruit of catch-up growth. They failed to carry market reforms to varying degrees. Productivity has wilted.

全部の新興市場がこんな羽目に陥ったわけじゃありません。

ポーランドとかチェコをニカラグアと比べるのは無意味ですから。

でもね、沢山の国が構造危機に陥ってて中所得国の罠にはまってるってのは否定出来ません。

キャッチアップ型経済の楽勝分は楽勝し尽しちゃいましたから。

色々な形で市場改革を進めることに失敗したわけです。

生産性は下降線ですよ。

Brazil, South Africa and Russia have all hit the buffers and all have a foot in recession right now, casualties of commodity addiction or the Dutch Disease. The outlook for Russia is utterly bleak. It has blundered into a conflict with the West that will smother investment for years, and it may have to draw down its reserves to cover $700bn of foreign currency debt unless it can tap the capital markets again. It faces demographic implosion.

ブラジル、南アフリカ、ロシアは揃ってバッファーに突き当たって、今や片足を不況の棺桶に突っ込んでます。

商品バブル中毒、オランダ病の犠牲者ですな。

ロシアのお先なんて全く真っ暗ですよ。

この先何年間も投資が見込めなくなるような西側との衝突をやらかした上に、資本市場にもう一回入れてもらえなければ7,000億ドルも積み上げた外貨建て債務を手当てするために準備金を取り崩さなくちゃいけなくなるかもしれません。

人口問題も抱えてますしね。

Now these countries - and many others with parallel problems, like autocratic Turkey under Tayyip Recep Erdogan - must brace for a secular rise in global borrowing costs, and as the BIS warns, the world is today more sensitive to interest rates than ever before. As yields on two-year US Treasuries ratchet higher, the US currency will inevitably ratchet with it. "I am convinced that we are close to a major cyclical recovery for the dollar," said Nomura's Mr Nordvig.

今、この手の国(と、タイィップ・レセップ・エルドアンの独裁トルコみたいに似たような問題を抱える沢山の国)は、世界的な借入金利の長期的上昇を覚悟しなくちゃいけないわけで、それからBISがワーニングしてるみたいに、世界は今やこれまで以上に金利に対してセンシティブになっているわけです。

米国債2年物の金利が急上昇すると同時に、米ドルも否応なく急上昇するでしょうよ。

「確信してるんだけどね…僕らはもう直ぐ大周期的な米ドル上昇に見舞われるよ」と野村證券のノードヴィグ氏は言いました。

The dollar did not rally in the tightening cycle of 2004 to 2007 but that was an exception, the result of the EMU bubble, as well as trillions of reserve accumulation by China and the commodity bloc, amid a feverish rotation into euro bonds. That chapter is closed.

米ドルは2004年から2007年の引き締めサイクルの時には上昇しませんでしたけどね、あれって例外でしたしね…EMUバブルとか、中国と資源国が貯め込んだ数兆ドルの外貨準備とか、

思いっ切りユーロ債へ資金をGOした結果ですよ。

あの時代は終わったんです。

This time may look more like the traumatic episodes of the Volcker Fed, or the mid-1990s, both occasions when the world woke up to find the US had not spiralled into decline after all, and latterly was the only superpower left.

今回はボルカーFRBとか1990年代中盤のトラウマ事件っぽくなるんじゃないかなーと…両方とも、気が付いたら米国は没落なんて全然してなくて世界最後の超大国になってました、っていう。

The BRICS, the mini-BRICS and much of global finance have taken out a colossal short position on the US dollar. Mrs Yellen has just issued the first margin call.

BRICSとかミニBRICSとか世界の殆どの金融は米ドルを思いっ切りショートしてきましたでしょ。

イェレン議長は最初の追証請求を出したわけです。