ECBs deflation paralysis drives Italy, France and Spain into debt traps

(ECBのデフレ麻痺でイタリア、フランス、スペインが債務トラップに追い込まれる)

By Ambrose Evans-Pritchard

Telegraph: 9:47PM BST 02 Apr 2014

(ECBのデフレ麻痺でイタリア、フランス、スペインが債務トラップに追い込まれる)

By Ambrose Evans-Pritchard

Telegraph: 9:47PM BST 02 Apr 2014

Frankfurt could force down the euro at any time by signalling a determination to do something about its predicament. It has chosen not to do so

ECBは何か危機対策をやるぞという決意をほのめかせばいつだってユーロを下落させられるでしょうが、そうしたくないのです。

The European Central Bank has let it happen. Deflation has been running at an annual rate of -1.5pc in the eurozone over the past five months, when adjusted for austerity taxes.

ECBは放置プレーにしました。

ユーロ圏のこの5ヶ月間の物価上昇率は年率-1.5%(増税分調整後)になりました。

Prices have been falling at a pace of 6.5pc in Greece, 5.6pc in Italy, 4.7pc in Spain, 4pc in Portugal, 3pc in Slovenia and nearly 2pc in Holland since September, based on my rough calculations (annualised) of Eurostat monthly data.

EUROSTATの月次データをざっくり(年率に)計算したところ、9月以降の物価の下落スピードはギリシャが-6.5%、イタリアが-5.6%、スペインが-4.7%、ポルトガルが-4%、スロベニアが-3%、オランダが-2%近くになってます。

The rise of the euro against the dollar, yen, yuan and the currencies of Brazil, Turkey and developing Asia, account for some of this imported deflation. Euroland's trade-weighted index has risen 6pc in a year.

ユーロの米ドル、日本円、人民元、そしてブラジル、トルコ、アジアの新興諸国の通貨に対する上昇が、この輸入デフレの一端を担っています。

ユーロランドの貿易荷重指数は一年で6%も上昇しました。

But that is no excuse. It is the direct consequence of the ECB's own monetary policy. Frankfurt could force down the euro at any time by signalling a determination to do something about its predicament. It has chosen not to do so, hoping that a few dovish words spoken without conviction will somehow turn the global tide.

でもそんなもん、言い訳になりゃしません。

これはECBの金融政策の直接的な結果ですよ。

ECBは何か危機対策をやるぞという決意をほのめかせばいつだってユーロを下落させられるんですから。

適当なハトっぽいことをちょこっと言えば世界的な流れも変わるかもーとか期待して、そうしないことにしたんでしょ。

It is hard to judge at what point deflation becomes embedded in the system. Factory gate prices have been slipping since mid-2012. The pace quickened to -1.7pc in February, the steepest decline since the Lehman crisis. But this time it is not the one-off effect of a financial crash. It is chronic, and more insidious.

どの時点でデフレが根付いちゃったかを判断するのは難しいです。

工場出荷価格は2012年中盤から下落してますから。

-1.7%に加速したのは2月。

リーマン危機からこっち一番急激な下落です。

でも今回は金融危機による一回限りのことじゃありませんから。

慢性的な上に、もっとヤバい。

Professor Luis Garicano, from the London School of Economics, said the economic models used to predict inflation seem to be breaking down, leading to serial misjudgments. "They need to take very serious action," he told the Financial Times.

ロンドン・スクール・オブ・エコノミクスのルイ・ガリカーノ教授は、インフレ予測に用いられる経済モデルがぶっ壊れて間違いを連発させたみたいだね、と言います。

「無茶苦茶真剣な対策が必要だよ」と教授はFT紙に言いました。

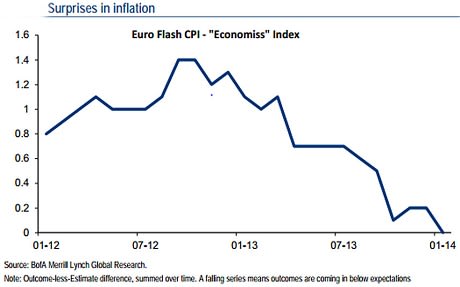

Laurence Boone and Ruben Segura-Cayuela, from Bank of America, say their "inflation surprise" index keeps ratcheting lower as one shock after another hits the eurozone, while their gauge of "deflation vulnerability" has been flashing red for most EMU countries.

バンク・オブ・アメリカのローレンス・ブーン氏とルーベン・セギュラ=カユエラ氏は、「インフレ・サプライズ」指数はショックがユーロ圏を襲う度にガンガン下がると同時に「デフレ脆弱性」はユーロ加盟国のほとんどで赤信号点滅中だ、と言いました。

The effect is deeply corrosive even if the region never crosses the line into technical deflation. "Lowflation" near 0.5pc can play havoc with debt trajectories if it goes on for long, ultimately throwing Europe back into a debt crisis. "The biggest threat to public debt dynamics is weaker-than-expected inflation. Merely lower than expected inflation, not even deflation, would lead to a significant deterioration in countries' public finances," they said.

ユーロ圏が一度もテクニカル・デフレの一線を越えていなかったとしても、その影響は深刻ですよ。

0.5%近い「ローフレ」は長引けば債務を爆増させる可能性、そして最終的にはヨーロッパを再び債務危機に投げ込む可能性があります。

「政府債務のダイナミクスに対する最大の脅威は、予想を下回るインフレ。期待値を下回るだけで、デフレですらないのに、国家財政を猛烈に悪化させるからね」とのこと。

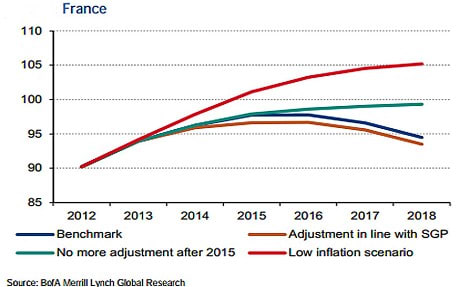

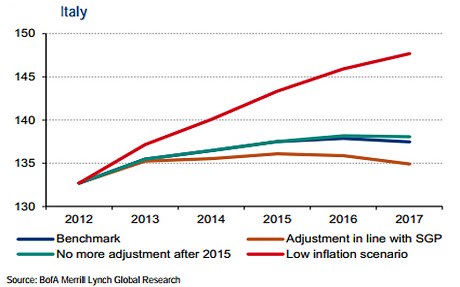

The bank said lingering "lowflation" would cause debt ratios to surge by 2018, rising 10 percentage points in France to 105pc of GDP, 15 points in Italy to 148pc and 24 points to 118pc in Spain.

バンク・オブ・アメリカ曰く、長期「ローフレ」は2018年までに債務比率を急増させるそうで、フランスは105%(+10%)、イタリアは148%(+15%)、スペインは118%(+24%)になるとか。

These countries face a Sisyphean Task. Whatever they achieve through austerity is overwhelmed by the greater power of debt-deflation. The same "denominator effect" - a debt burden rising faster than nominal GDP - would engulf the private sector as well, still the Achilles Heel for Spain, Portugal and Ireland.

これらの国は果てしなく無駄な労働に直面しています。

緊縮財政で何を達成しようが関係なく、それは債務デフレの巨大な力に圧倒されるのであります。

この「デノミ効果」は、未だにスペイン、ポルトガル、アイルランドのアキレス腱である民間セクターも一口ペロリでしょう。

Moody's says "lowflation" (0.5pc to 1pc until 2018) would "reignite concerns about debt sustainability", tightening the vice on households and companies with fixed-rate debts. It would erode bank assets, risk fresh bank failures and hit life insurers through a mismatch in maturities. "Avoiding outright deflation does not fully shield the euro area from the shock: the combination of low growth and low inflation has significant implications for all sectors of the economy," it said.

ムーディーズは、「ローフレ」(2018年まで0.5-1%)は「債務の持続性懸念を再燃」させて、固定金利の借入のある家計と企業の締め付けを強めるだろうと言っています。

銀行資産も目減りさせて、新たな銀行破綻を招くリスクもあり、償還期限のミスマッチにより生保に損害を与える可能性もあります。

「本格的なデフレを回避してもユーロ圏をショックから完全に護ることはなお。低成長とローフレのコンボは経済全般に著しい影響を与えている」とのこと。

Reza Moghadam, from the International Monetary Fund, says that even inflation of 0.5pc threatens to "scupper the nascent recovery" in Europe. It aggravates the North-South divide, making it yet harder for the Club Med to claw back lost competitiveness. The debt-stricken states have to carry out even more drastic internal devaluations to regain ground, but that in turn pushes up their debt ratios. "Each point of relative price adjustment must be bought at the cost of greater debt deflation," he said.

IMFのレザ・モガダム氏は、0.5%の物価上昇率ですらヨーロッパの「初期の回復を損ない」かねないとしています。

これは南北格差を悪化させて、地中海クラブの競争力回復を一層困難にしています。

重債務国は足場を再確保するために更に抜本的な内的減価を実施しなければなりませんが、それによって債務は増加しています。

「相対価格を調整する毎に債務デフレのコストは増大する」と同氏は言います。

"Very low inflation may benefit important segments of the population, notably net savers. But in the current context of widespread indebtedness problems, it is working to the detriment of recovery in the euro area, especially in the more fragile countries, where it is thwarting efforts to reduce debt," he said.

「超ローフレは国民の重要グループ、特に預金者に恩恵をもたらすかもしれない。しかし現在の後半な債務問題を考えれば、ユーロ圏の景気回復をとん挫させつつある。特に債務削減努力が邪魔されているより脆弱な国だ」

Once you grasp this elemental point that it is "thwarting" efforts to control debt, the spectacular idiocy of EMU policy becomes clear. Austerity as designed is self-defeating. The fundamental failure has been the ECB refusal to offset the contractionary effects with enough monetary stimulus to keep nominal GDP growing faster than the debt stock of Italy, France, Spain, Portugal and Greece, but not only for those countries.

債務をコントロールしようとする努力を「邪魔している」という初歩的なポイントを理解すると、ユーロ政策の天文学的バカさ加減が明白になります。

まともに緊縮財政を実施することは自滅的なのです。

根本的な失策は、ECBが、これらの国々に留まりませんが、イタリア、フランス、スペイン、ポルトガル、ギリシャの債務残高よりも速く名目GDPを成長させ続けられるだけの金融刺激を行って、縮小効果をオフセットしようとしないことです。

Again, the ECB could have done this. It chose not to because it allowed its monetary policy to become infected by judgments on moral hazard outside its proper ambit, by pre-modern central banking doctrines or by fear of what Germany might or might not say.

もう一度言いますが、ECBはこうすることが出来たのです。

こうしないことに決めたのです。

それというのも、ECBの正当な守備範囲外でのモラルハザードに関する判断や前時代的な中銀ドクトリン、またはドイツが言うかもしれないし言わないかもしれないことへの恐怖に、金融政策が影響されることを許したからです。

Nowhere is this failure more obvious than in Italy, where debt has jumped from 119pc to 133pc since 2010 despite draconian fiscal tightening and a primary budget surplus. Rock-star premier Matteo Renzi has stormed into office with a 100-day New Deal, tearing up the austerity script and going for broke with supply-side reforms and a fiscal blast to kickstart growth.

イタリアほどこの失策が明白な場所はありません。

苛烈な緊縮財政やプライマリーバランスが黒字であるにも拘わらず、同国の債務比率は2010年の119%から133%まで跳ね上がりました。

ロックスターのようなマッテオ・レンツィ首相は100日間のニューディールを掲げて就任し、緊縮財政シナリオを破り捨て、経済成長のエンジンをかけるべく、サプライサイド改革と財政出動に乗り出しました。

Antonio Guglielmi, from Mediobanca, said markets are betting that Mr Renzi will prove to be the "discontinuity catalyst" capable of pulling Italy out of its seemingly unstoppable low-growth trap, achieving a virtuous circle that at last raises the economic speed limit and cuts into debt ratios. But even this high-stakes gambler from Florence can do little in the end against the sheer granite madness of the EMU edifice.

メディオバンカのアントニオ・ググリエルミ氏は、マーケットはレンツィ首相がイタリアを一見停止不可能な低成長トラップから引っ張り出せる「不連続カタリスト」であることを証明し、遂に好循環を回し始めて経済のスピードリミットを引き上げ、債務比率を下落させるだろうと考えている、と言います。

とはいえ、フローレンスから来たこの大物ギャンブラーですら、ユーロ大魔殿の超狂気の沙汰には殆どお手上げでしょう。

Mediobanca said his last-ditch mission to save Italy is doomed unless the ECB launches quantitative easing to head off debt deflation, and if he has to comply with the EU Fiscal Compact as it forces the country into a primary budget surplus of 6pc of GDP by next year. "It is up to Mr Renzi to give a loud and clear message to Frankfurt on softening austerity," said the bank.

メディオバンカは、レンツィ首相の果敢なイタリア救済ミッションは 、ECBが債務デフレ阻止のために量的緩和を実施しない限り、また来年までにプライマリーバランスの黒字を対GDP比6%にせよとイタリアに命じるEUの欧州財政協定に従わなければならないことになれば、成功の見込みなしだとしています。

「緊縮財政の緩和についてECBにハッキリ物申すかどうかはレンツィ首相次第だね」とのことです。

We will find out on Thursday whether the ECB is ready to grasp the nettle of QE, or indeed any nettle. Loans to businesses are contracting at a rate of 3pc. The ECB is missing its 2pc inflation target by 150 basis points, and will continue to miss it badly in 2015 and 2016 by to its own forecasts. You could argue that this is a grave breach of of its primary mandate - not to mention its broader Treaty obligations to support growth and the economic objective of the Union - yet it still sits on its hands.

ECBがQEという困難、または何らかの困難と闘う覚悟をしたかどうかは、木曜日にわかるでしょう。

法人に対する貸出は3%の勢いで減少中です。

ECBは自らのインフレターゲット2%を150BPもミスっている上に、自分で2015年と2016年も思いっ切りミスり続けるだろうと予測しています。

これは深刻な重要任務違反だと言ってやることは出来るでしょうが(成長とEUの経済目標を助けるというより広範な欧州条約の義務は言うまでもなく)、それでもECBは何もしないのです。

Critics have noted that German M3 growth has been on a near perfect path of 4pc to 5pc annually over the years, but let it never be said that the ECB sets monetary policy entirely in the interests of one country - whatever the devastation all around, including in Finland and Holland lately. If other governors are so supine - or so cowed by Bundesbank supremacy - that they go along with this, they deserve their fates.

批判者は、ドイツのM3マネーサプライの伸び率は何年間も年率4-5%という完璧なカーブに乗っかっているじゃないかと指摘していますが、最近ではフィンランドやオランダなども含む全方位大惨事にも拘らず、ECBは一ヶ国の利益のためにだけ金融政策を設定しているなどとは決して言われません。

他国の中銀総裁が余りにも根性なしで(またはドイツ中銀の力に屈して)これに諾々と従っているとすれば、その運命も当然です。

Perhaps there will be a tiny cut in interest rates, or a negative deposit rate, or an end to sterilisation of bond purchases; or some such eyewash that comes a year late, is a trillion short and makes no difference. Once deflation fastens on an economy, it takes ever more radical action to break loose. Jens Weidmann, from the Bundesbank, has opened the door to QE - very slightly, seemingly for tactical reasons - but the political bar to such action is punishingly high in Germany.

恐らく、微々たる利下げかマイナス預金金利があるでしょう。

または国債購入の不胎化終了があるでしょう。

もしくは似たようなお茶を濁すような真似を一年手遅れでやるかもしれません。

全然足りませんよ。

何の違いも生みませんよ。

デフレが経済に根付いたが最後、それから逃れるには今よりも一層異例の対策が必要になります。

ドイツ中銀のイェンス・ヴァイトマン総裁はQEの扉を開きました(本当に極僅かですが、どうやら戦術的な理由によるもののようです)。

しかしそのような対策に対する政治的ハードルは、ドイツでは恐ろしく高いのです。

The Bundesbank was over-ruled on the ECB's bond-rescue plan in 2012 (OMT) but Germany as such was not over-ruled, a point that is often misunderstood by Anglo-Saxon analysts. The scheme was cooked up in concert with the German finance ministry and had the full support of Chancellor Angela Merkel. I heard a top German official say at a private dinner three weeks before the OMT that "nothing flies in the eurozone right now without Berlin's approval", and I have no doubt that he meant it. This is how EMU works. There is no sign yet that Mrs Merkel is ready for QE.

ドイツ中銀は2012年、ECBのOMT案を巡って負けましたが、ドイツは負けませんでした。

アングロ・サクソン系のアナリストがよく間違えるポイントです。

この策略はドイツ財務省と一緒に練られたのであって、アンゲラ・メルケル独首相の全面的な支援を得ていました。

僕はOMTの3週間前にプライベートなディナーの席で、ドイツ高官が「今、ユーロ圏でドイツの承認なしに進んでいることは何もない」と言うのを聞きましたが、彼は間違いなく大真面目にそう言ったのだと思います。

メルケル首相がQEを認める気配はまだありません。

The ECB insists that the latest dip in inflation is due to falling energy costs, and therefore transient. It is a suspicious alibi. The ECB made the opposite case in 2008, raising rates into an oil shock on the grounds that energy effects are not transient.

直近の物価上昇率下落はエネルギー価格下落によるものであって一時的なものだ、とECBは言い張っています。

怪しいアリバイですな。

ECBは2008年に逆の主張をして、エネルギー価格の影響は一時的なものではないという根拠でオイル・ショックへと利上げしたじゃありませんか。

In any case, some of the world's top energy analysts say oil has only just begun to fall as global crude production surges. Iraq's output has reached a 35-year high. Libya's exports are poised to soar as rebel militias end their blockade. The US may add 1m barrels a day this year, hitting 11m. A drop in oil prices to $80 would be a tonic for falling real incomes in half of Europe, but it would also unhinge "inflation expectations" altogether, the kind of rupture that hit Japan in the 1990s.

いずれにせよ、世界屈指のエネルギー・アナリストの一部は、石油価格は世界的な産油量の急増に伴って下落し始めたばかりだと言っていますね。

イラクの生産量は35年ぶり最高に達しました。

リビアの輸出量は反政府勢力が封鎖を終了して、今にも急増しようとしています。

米国も今年は100万バレル/日増産して1,100万バレルに達するかもしれません。

石油価格が80ドルまで下落したことは、実質所得が落ちているヨーロッパの半分にとって天の助けでしょうが、同時に1990年代に日本が経験したような「インフレ期待」崩壊に見舞われるでしょう。

Europe's deflation scare will blow over if we really are on the cusp of a fresh cycle of global growth. Whether that is the case as the US and China tighten together remains to be seen. "We could be facing years of slow and subpar growth," said the IMF's Christine Lagarde this week.

世界的な経済成長の新サイクルが本当に始まろうとしているなら、ヨーロッパのデフレ懸念は終わるでしょう。

米中同時引き締めが行われる時にそんなことになるかどうかは、未だわかりません。

「数年に亘って低成長、標準以下の成長が続く可能性がある」とIMFのクリスティーヌ・ラガルド専務理事は今週言いました。

"The risk is that without sufficient policy ambition, the world could fall into a medium-term low-growth trap. More monetary easing, including through unconventional measures, is needed in the euro area," she said.

「十分な政策的熱意がなければ、世界は中期的低成長トラップに陥る危険性がある。異例の対策を含む追加禁輸緩和がユーロ圏には必要だ」とのことです。

We may even be nearing the end of a five-year global cycle, one that Euroland largely missed due to its own unforced errors. If so, the region is just one upset away from a lurch into full-blown deflation that must mathematically drive Italy and others into insolvency, precipitating a sovereign debt crisis too big to be contained. It is a policy choice. Twenty-four men and women with a will of their own are letting it happen.

僕らは世界的な5年サイクルの終わりに近付きつつある可能性すらあります。

ユーロ圏が勝手に転んで殆ど恩恵に与れなかったサイクルです。

だとすれば、この地域はあと一歩で、数学的に考えてイタリアその他を否応なく破綻に追い込み、封じ込められない規模のソブリン債務危機を引き起こす、全面的なデフレに突入でしょう。

自分の意志を備えた24人の男女が成り行き任せにしているのです。