A coming boom in the eurozone periphery? (technical)

(ユーロ圏周辺国にブーム到来?(テクニカル))

By Ambrose Evans-Pritchard Economics

Telegraph Blog: Last updated: June 3rd, 2013

(ユーロ圏周辺国にブーム到来?(テクニカル))

By Ambrose Evans-Pritchard Economics

Telegraph Blog: Last updated: June 3rd, 2013

Now here is something to ponder. Simon Ward from Henderson Global Investors – one of Britain's last surviving monetarists – predicts a Latin comeback later this year.

ネタが出てきました。

ヘンダーソン・グローバル・インベスターズのサイモン・ウォード氏(英国最後のマネタリストのお一人です)が、ラテン陣営は今年中に復活する、と予測しています。

As an anti-Keynesian, he thinks the great austerity debate is largely bogus. Europe tanked last year because monetary policy was too tight, and will now recover (in his view) for the opposite reason.

アンチ・ケインズ主義者として、彼は緊縮大議論はほぼ茶番だと考えているんですね。

ヨーロッパは昨年、金融政策がきつ過ぎてダメになりました。

で、今回、逆の理由により回復するのだそうです(彼の考えですが)。

"Eurozone monetary trends are signalling a return to growth over the remainder of 2013, with the periphery participating in the recovery during the second half – a development that would stun a bearish Keynesian consensus."

「ユーロ圏のマネタリー・トレンドは2013年中に成長が再開するというサインを出している。周辺国は下半期に回復に加わる。ベアなケインズ主義の考えを呆然とさせる展開だね」

And bang on cue, we had a jump in the eurozone manufacturing PMI to a 15-month high of 48.3 in May (though still below the contraction line).

そして見計らったように、ユーロ圏の製造業購買担当者景況指数は5月、15か月ぶり最高の48.3まで急上昇しました(まあ、それでも縮小ライン以下ですけども)。

Spain jumped 3.3 to 48.1, the best in two years. Italy jumped 1.8 to 47.3. New orders spiked in both countries. Glimmers of hope.

スペインは3.3跳ね上がって2年ぶり最高の48.1になりました。

イタリアも1.8跳ね上がって47.3になりました。

新規受注は両国で急増しました。

希望の光が見えますね。

Fellow monetarist Michael Darda from MKM partners has made a similar call:

同じくマネタリストの、MKMパートナーズのマイケル・ダーダ氏も、同様の発言をしています:

"Europe has been and continues to be in a deep slump, the result of serial monetary errors particularly in the summer of 2008 and then again in the spring and summer of 2011.

「ヨーロッパは相変わらずドツボだが、これは金融政策に連続して失敗した結果だ。特に2008年の夏、そして2011年の春、夏の失敗がイタイね」

"However, with key leading monetary and credit market indicators having made a decisive turn higher, we believe the consensus (which is calling for recession through 2013) is now too negative. We expect moderate growth in the euro-area during 2H and extending into 2014.

「でも、金融と信用の主要指標は決定的に上向きになったし。僕らは、(2013年一杯も不況だという)コンセンサスは今やネガティブ過ぎだと思ってるよ。今年の下半期から2014年にかけて、穏やかな成長になると予測している」

"Encouragingly, euro-area M1 growth continues to accelerate, up 8.5 per cent y/y in April, the fastest growth since 2010. Broad money growth has been slower, but it too accelerated in April with M2 up 4.8 per cent y/y, the fastest since 2009."

「励まされることに、ユーロ圏のM1の伸びは加速し続けてるしね。4月は前年比+8.5%で、2010年以来最速。ブロードマネーの伸び率はもっと遅いけど、それでも4月は加速して、M2は前年比+4.8%と2009年以来最速を記録したよ」

Michael Darda and Simon Ward are both excellent economists. I pass on their thoughts to readers, without endorsing them. I would quibble slightly with the figures, which are distorted by base effects and much else besides.

マイケル・ダーダ氏もサイモン・ウォード氏も、素晴らしいエコノミストです。

僕は彼らの考え皆さんにお伝えしますが、その通りとか言わないことにします。

このデータには若干ケチをつけたくなっちゃうんですよね…ベース効果だのなんだので歪んじゃってるので。

Broad M2 has been slowing again, growing at a 3pc rate over the last three months. Narrow M1 is tapering off on a month-to-month basis, and M3 has been almost flat for a while (despite the year-on-year rise).

M2はまた減速して、この3ヶ月の伸び率は3%です。

M1は前月比では減ってますし、M3はしばらくほぼ横ばい状態です(まあ、前年比だと伸びてますが)。

The Italian data can be wild, jerked up and down by a category known as "other financial intermediaries". This rocketed in March. Does that really imply that consumers and businesses are about to go out and spend?

イタリアのデータは、「その他の金融仲介機関」と呼ばれるカテゴリーでガタガタと動きが激しいこともありますしね。

3月は急上昇しました。

だからって、それが消費者と企業が金を使いまくろうとしているサインだってことってあるのかなと。

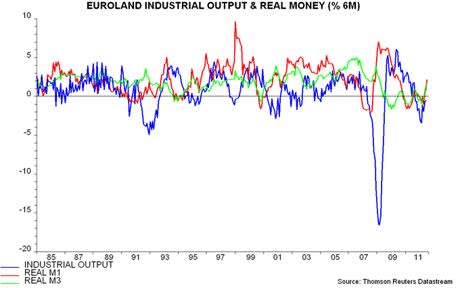

Simon Ward uses his own special gauge – 6-month real M1 money (not annualised) ― that has been a pretty good indicator over the last five years, though like all monetary signals it can give rogue readings.

サイモン・ウォード氏は独自の尺度、(年率に換算していない)6ヶ月実質M1マネーを使っています。

これはこの5年ほどは素晴らしい指標ですが、全てのマネタリー・シグナル同様、あてにならないこともあります。

Real M1 did jump the gun in the summer of 2012. The recession was in reality about to deepen (though stock markets loved it).

実質M1が2012年の夏にフライングしたのは本当ですよ。

不況は実際には悪化しようとしていました(市場は沸きましたけどね)。

My own view is that declining credit – and further "pro-cyclical" deleveraging by banks, as they are forced to meet the Basel III rules – ensure stagnation for a long time to come. That means falling nominal GDP in Spain and Italy, and therefore a surging debt ratio.

信用減少(と、バーゼルIIIへの対応を迫られる銀行の更なる『プロサイクリカルな』レバレッジ解消)で、まだまだしばらく低迷するのは確実になる、と僕は考えています。

それはつまり、スペインとイタリアで名目GDPが縮小して、それによって債務比率が急上昇するってことですね。

Rule of thumb: if the NGDP growth of Spain and Italy is well above zero for the next two years, they can perhaps make it in EMU. If it is below zero, they are doomed.

以下、確実。

スペインとイタリアの名目GDPの成長率が今後2年間しっかりプラスなら、ユーロ残留を果たせるかもしれません。

マイナスなら、一巻の終わりです。

Which of these outcomes lies in store is entirely dependent on the actions of the European Central Bank. The Jesuit-trained Mario Draghi understands this perfectly. Do the northern hawks?

どちらの結末が待ち受けるのかは、全くECB次第です。

イエズス会で訓練されたマリオ・ドラギ総裁は、これを完璧に理解しています。

北部欧州のタカ派は、理解してますかね?