Is the whole theory of secular stagnation a hoax?

(長期停滞論は丸っと嘘っぱち?)

By Ambrose Evans-Pritchard

Telegraph: 8:55PM GMT 06 Jan 2016

(長期停滞論は丸っと嘘っぱち?)

By Ambrose Evans-Pritchard

Telegraph: 8:55PM GMT 06 Jan 2016

The Bank for International Settlements says the entire strategy of stimulus by global central banks is based on a false premise

BIS曰く、各国中銀による刺激戦略は全て間違った前提に基づいている、とのこと。

The world's monetary watchdog has thrown down the gauntlet. It has challenged the twin assumptions of secular stagnation and the global savings glut that have possessed - some would say corrupted - the Western economic elites.

世界の金融監視機関が挑戦に打って出ました。

西側の経済エリートを虜にしている(堕落させているという人もいます)長期停滞論と世界的な過剰貯蓄という二大前提に異議を唱えたのです。

It has implicity indicted the US Federal Reserve and fellow central banks for perverting the machinery of interest policy to conjure demand that may not, in fact, be needed, and ensnaring us in a self-perpetuating "debt-trap" with a diet of ever looser money.

FRBや各国中銀は実は必要ではないかもしれない需要を生み出すために金利政策の仕組みを悪用し、我々を恒常的な金融緩和によって自己永続的「債務トラップ」にはめているのだ!と暗に非難したわけです。

The Bank for International Settlements (BIS) - the temple of monetary orthodoxy in Switzerland - has been waiting for this moment, combing through the archives of economic history to mount an unanswerable assault.

BIS(スイスにあるオーソドックスな金融政策の聖堂)は決定的な一撃を加えるべく経済史を紐解きながら、この瞬間を待ち構えていました。

The BIS believes it has found the smoking gun in a study of recessions in 22 rich countries dating back to the late 1960s. The evidence suggests that the long malaise of the post-Lehman era - and the strange episode that preceded it - can be explained almost entirely by the destructive effects of boom and bust on productivity growth.

BISは先進22ヶ国の1960年代まで遡る不況に関する論文の中に決定的な証拠を発見したとしています。

この証拠によると、ポスト・リーマン危機時代に長引いている苦境(とそれに先立つ奇妙なエピソード)は、好不況の循環の生産性の伸びに対する破壊効果でほぼ全て説明出来るそうです。

Credit bubbles are corrosive. They gobble up resources on the upswing, diverting workers into low-productivity sectors and building booms. In Spain the construction share of GDP reached 16pc at the height of the "burbuja" in 2007, when teenagers abandoned school en masse to earn instant money erecting ghost towns.

信用バブルは腐食性です。

上昇期には資源を大量に飲み込み、労働者を低生産性のセクターや建設バブルに流入させます。

スペインでは建設のGDPに占める割合が2007年の「Burbuja(バブル)」のピークに16%に達しましたが、当時、ゴーストタウンを作って手っ取り早く稼ぐために、若者が大勢に学校を辞めました。

Parasitical wastage creeps in. "Financial institutions' high demand for skilled labour may crowd out more productive sectors," said the paper, acidly.

寄生的消耗が忍び寄ります。

「金融機関の高い高技能労働者需要が、より生産性の高いセクターを締め出す可能性がある」とBISのレポートは厳しく指摘しました。

The bubbles leave a long toxic legacy after the bust hits. This takes eight years or so to clear. "The occurrence of a crisis greatly amplifies the impact of previous misallocations," said the paper, racily titled "Labour reallocation and productivity dynamics: financial causes, real consequences".

このバブルが弾けた後に長期的に影響をもたらす悪い置き土産をしていきました。

これを解消するのに8年ほどかかります。

「危機の発生で過去の不適切な配分の影響が著しく増大した」と、『労働配分と生産性ダイナミクス: 金融的原因、実際の原因』などとわざとらしい題名が付けられたレポートには書かれています。

Crippled economies have to make the switch back to healthier sectors against the headwinds of a credit crunch and a broken financial system, and typically amid austerity cuts in public investment.

損傷した経済は、信用収縮と壊れた金融システムという向かい風に向かって、より健全なセクターに戻らなければなりません。

通常は緊縮政策による公共投資削減の真っ只中でもあります。

The BIS has long argued that a key reason why the US recovered more quickly than others is because it tackled the bad debts of the banking system early, forcing lenders to raise capital. This averted a long credit squeeze. It cleared the way for Schumpeterian creative destruction.

BISは前々から、米が他の国よりも迅速に回復した主要因は、銀行システムの不良債権に早期に取り組んで金融機関に資本増強を強いたからだと論じてきました。

これで長期的な信用不足が回避されました。

これでシュンペーターの創造的破壊が可能になりました。

The Europeans dallied, prisoners of their bank lobbies. They let lenders meet tougher rules by slashing credit rather than raising capital. Europe's unemployed have paid a high price for this policy failure.

ヨーロッパ勢は銀行のロビー活動の虜になって無為に過ごしました。

金融機関が資本を増強するよりも資本を減らすことでより厳しいルールを守らせました。

ヨーロッパの失業者はこの政策ミスのおかげで酷い代償を払わされました。

Claudio Borio, the paper's lead author and the BIS's chief economist, said the "hysteresis" effect of lost productivity is 0.7pc of GDP each year. The cumulative damage from the boom-bust saga over the past decade is 6pc.

同レポートの主筆者でBISのチーフ・エコノミスト、クローディオ・ボリオ氏は、生産性の損失の「ヒステリシス」効果は毎年、GDPの0.7%に相当すると言います。

過去10年間の景気循環物語による累積損傷は6%になります。

This more or less accounts for the phenomenon of "secular stagnation", the term invented by Alvin Hansen in 1938 and revived by former US Treasury Secretary Larry Summers. Loosely, it describes an inter-war Keynesian world of deficient investment and demand.

1938年にアルヴィン・ハンセンが作ってラリー・サマーズ元米財務長官が復活させた「長期停滞」という現象の説明は、これでほぼつきます。

この言葉は大まかに言うと、大戦時間の投資と需要が不足するケインズ的な世界を表しています。

The theory of the global savings glut propagated by former Fed chief Ben Bernanke falls away, and so does the Fed's central alibi. It can longer be cited as the canonical justification for negative real rates. The alleged surfeit of capital in the world proves a mirage. So does the output gap.

ベン・バーナンキ元FRB議長によって広められた世界的な過剰貯蓄論は剥がれ落ち、FRBの主なアリバイも剥がれ落ちています。

もはやネガティブ実質金利の正当な理由として取り上げることは不可能です。

世界における資本過多とやらは幻だと証明されました。

産出ギャップもご同様です。

If the BIS hypothesis is correct, there is no lack of global demand. The world faces a supply-side problem, impervious to monetary stimulus. The entire strategy of global central banks is based on a false premise.

BISの仮説が正しければ、世界的な需要不足なぞないのです。

世界は供給面の問題に直面しており、金融刺激などに影響されないのです。

各国の中銀の戦略は全て間違った前提に基づいていることになります。

There is little dispute that credit did run amok before the Lehman crisis. The Anglosphere was swept by infectious folly. Credit to households and firms in the US jumped from 157pc to 212pc of GDP over the decade leading up to 2008, and from 167pc to 248pc in the UK (OECD data).

信用がリーマン危機前に滅茶苦茶だったことに殆ど異論はありません。

アングロサクソン圏は感染性の愚行にやられていました。

2008年までの10年間に、家計と企業への信用は米国でGDPの157%から212%にまで跳ね上がり、英国では167%から248%に増えました(OECD調べ)。

The eurozone was just as bad, with parallel effects for countries that had to import the European Central Bank's loose money through currency pegs. Private debt in Denmark rose from 208pc to 275pc. Spain won the prize, rising from 137pc to 274pc. These were staggering jumps in such a short period, as some of us kept warning at the time, protesting vainly until we were blue in the face.

ユーロ圏も同様に酷い有様で、ペッグ制を通じてECBから低金利資金を輸入せざるを得なかった国への並列効果を伴いました。

デンマークの民間債務は208%から275%に増えました。

スペインは群を抜いていて、137%から274%まで増加しました。

この短期間においてこの増え方は驚くべきものであり、僕らの一部が当時ワーニングし続けた通りであり、顔が真っ青になるまで誰にも聞いてもらえない抗議を続けた通りです。

China has since replicated the Spanish property fiasco almost exactly, with the salient difference that the Communist Party's state-owned banking system will not allow a financial collapse. The trauma will manifest itself "a la japonnaise". It will be a slow loss of dynamism, a medscape of companies kept on life support, although interestingly the first state-owned shipbuilder - Wuzhou Ship - has just been allowed to go bankrupt.

中国はその後、スペインの不動産バブルをほぼそのまま繰り返しました。

中国共産党の政府が仕切る銀行システムが金融崩壊をさせなかったのが目立った違いでした。

このトラウマは「日本式」に出現しました。

緩やかなダイナミズムの喪失が起こり、興味深いことに最初の政府系造船会社(Wuzhou Ship)が倒産を認められたばかりとはいえ、企業は生命維持装置につながれることになるでしょう。

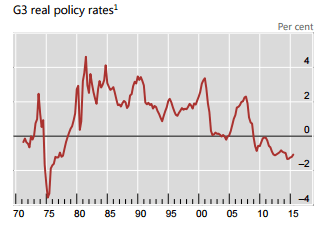

The BIS lodestar is the "natural" rate of interest, coined by the Swedish economist Knut Wicksell. If real rates are held too low, they throw the monetary system out of kilter and play havoc over time.

BISの指標は、スウェーデン人経済学者、クヌート・ウィックセルが作った新語、「自然」金利です。

実質金利は過剰に低く抑えられると、金融システムを揺るがして時と共に混乱を生じるというわけです。

Modern central banks think they have a warning gauge. When policy is loose, inflation picks up. This ignores irrefutable evidence that credit booms and asset prices can gather pace even if headline inflation is well-behaved, or even in deflation, and the consequences are dire.

現代の中銀は、自分達にはワーニング・ゲージがあると考えています。

政策が緩過ぎる時はインフレ率が上昇します。

これは

消費者物価指数が安定していても、もしくはデフレになっている時ですら、信用バブルと資産価格は加速し得るという反論しようのない証拠を無視しており、それは酷い結果になるでしょう。

Mr Borio swats aside the standard Fed objection that it is impossible to discern a bubble, asking whether it is really possible to discern the output gap or the "NAIRU" point of full employment, yet the Fed acts on these indicators.

ボリオ氏はバブルを無視することは出来ないとするFRBの標準的な反論を一蹴にして、FRBはこれらの指標に基づいて動いているのに、生産ギャップまたは完全雇用の「NAIRU」を本当に無視出来るのかと問いかけています。

He accused central banks of an "asymmetric" bias for the last quarter century. They let asset booms run their course, but throw the kitchen sink at each downturn. The result is ever-rising debt ratios, making it ever harder to right the ship again. "This can contribute to a kind of 'debt trap'. Over time, policy runs out of ammunition," he said.

また中銀の過去四半世紀の「非対称的」バイアスを非難しました。

中銀は資産バブルを放置したが、どの後退局面でも放棄しました。

その結果、債務比率は上昇し続けて、体勢を立て直すのをより一層困難にしました。

「これは或る種の『債務トラップ』を助長する可能性がある。時間と共に政策は弾切れになる」とのこと。

This is well understood. More contentious is the BIS claim that low rates themselves become "self-validating" and pull the monetary regime downwards over time - "easing begets easing".

これは良く理解されています。

低金利そのものが「正当性を証明する」ようになって、時間と共に金融政策を引き摺り下ろす、『緩和が緩和を呼ぶ』というBISの主張の方が異論は多いのです。

Personally, I struggle with these concepts. It could equally be said that the chief cause of surging debt ratios in Italy, Spain, France, Portugal, Finland and most of the eurozone from 2011 to 2014 was sheer policy error, the deflationary hammer blow of fiscal austerity and tight money at the same time. It led to a rising debt burden on a base of stagnant nominal GDP. The "denominator effect" automatically sent debt ratios spiralling upwards.

個人的にはこれらのコンセプトの理解に苦しみます。

と同様に、債務比率が2011-2014年にイタリア、スペイン、フランス、ポルトガル、フィンランド、そしてユーロ加盟国の大半で急上昇した主要因は、政策ミス、緊縮財政と金融引き締めの同時実施というデフレを招く打撃に他ならないとも言えるでしょう。

それが停滞する名目GDPの上で債務負担を膨れ上がらせました。

「デノミ効果」は自動的に債務比率を急上昇させるものです。

Nor is it clear exactly how, why or when the central banks first entered into their Faustian Pact. The implict BIS argument is that they should have let benign deflation run its course in the 1990s after the opening up of China and Eastern Europe doubled the global labour pool at a stroke, drastically containing wage pressure.

また、そもそも、正確にはいつ、どのように、なぜ中銀が悪魔との契約を結んでしまったのかもはっきりしていません。

BISの暗黙に、1990年代、中国と東欧の開放で世界の労働者プールを一気呵成に倍増させて、賃金圧力を劇的に抑え込んだ後、中銀は良性のデフレを放置すべきだったと論じています。

Yet it can hardly be disputed that Alan Greenspan, Ben Bernanke and their peers did in fact face a capital glut. The global savings rate rose relentlessly for two decades, reaching a peak of 25pc of GDP only last year.

しかし、アラン・グリーンスパン氏や他国の中銀総裁が実は資本過多に直面していたことは殆ど反論しようがありません。

世界の貯蓄率は20年間に亘って上昇し続け、つい昨年はGDPの25%のピークに達しました。

China, the emerging states of Asia, the petropowers and sovereign wealth funds did push foreign reserves to $18 trillion, pulling the money out of the global reservoir of consumption and hoarding it as capital instead.

中国、アジアの新興国、産油国、そしてSWFは確かに外貨準備を18兆ドルまで積み上げて、世界中の消費向け資金を吸い上げて代わりに資本として蓄積しました。

Be that as it may, the BIS is clearly right that zero rates and QE set off a tidal wave of stimulus through Asia, Latin America and emerging markets from 2009 onwards. It overwhelmed financial defences, pushed offshore dollar debt to $9.8 trillion, and drew the world's last holdouts into the Ponzi scheme. Only Cuba and North Korea seemed to escape the curse.

さはさりながら、BISの、ゼロ金利とQEが2009年以降にアジア、南米、新興市場を刺激でジャブジャブにした、というのは明らかに正解なのです。

それは金融的な防衛を圧倒して、オフショアの米ドル建て債務を9.8兆ドルまで膨張させ、世界最後の抵抗をねずみ講に引きずり込みました。

この呪いを免れたのはキューバと北朝鮮だけのようです。

Radical stimulus may have worked for the US and the UK in one sense, but it was a "Pareto suboptimal" for the world as a whole.

異次元的な刺激策は或る意味、米国と英国には効いたかもしれませんが、世界全体にとっては「パレート準最適」だったのです。

The result is before our eyes. Total debt has risen to an all-time high of 265pc of GDP in the OECD club and 185pc in emerging markets, 35 percentage points higher than it was at the top of the last credit cycle eight years ago.

その結果が、今僕らの前に在ります。

債務残高は史上最高のOECDでGDPの265%、新興市場で185%に達しました。

これは8年前の前回の景気サイクルのピークを35%も上回っています。

Mr Borio would like us to pluck up our courage and restore rates to their Wicksellian equilibrium, come what may. My fear is that it is already too late. The social and political consequences of a liquidation purge are too terrible. We are trapped in this insidious circle, and we will have to live with it.

ボリオ氏は僕らに勇気を出して、何が何でも、金利をBISのウィックセル均衡まで戻してほしいのです。

僕が心配なのは、もう手遅れだということです。

流動性パージの社会的、政治的な結末は兎にも角にも酷過ぎます。

僕らはこの狡猾なサイクルに囚われていて、それと共生するしかないでしょう。

Money and debt contracts are social conventions. They can be torn up, or reinvented. When we go into the next global downturn - perhaps in 2017 - we may have to resort to an entirely different form of QE. The next step is to print money to fund state spending directly, and probably behind capital constraints in a less "globalized" world.

マネーと債務の契約は社会的な規則です。

破り捨てることも出来れば、作り直すことも出来ます。

次の世界的な景気後退局面に入る時(多分2017年)、僕らは全く違った形のQEをしなければいけなくなるかもしれません。

次のステップは公共支出に資金を直接、もしかすると、より「グローバライゼーションが退化した」世界の資本規制の背後で供与するために紙幣を増刷することです。

Economic life will go on. As the Habsburgs used to say, the situation is desperate but not serious.

経済生活は続きます。

ハプスブルク家の言葉通り、状況は切実だが深刻ではないのです。