Europe already has one foot in 'Japanese' deflation grave

(ヨーロッパは既に「日本式」デフレ棺桶に片足です)

By Ambrose Evans-Pritchard

Telegraph: 8:40PM BST 23 Oct 2013

(ヨーロッパは既に「日本式」デフレ棺桶に片足です)

By Ambrose Evans-Pritchard

Telegraph: 8:40PM BST 23 Oct 2013

Europe is sliding into a deflationary trap, displacing Japan as the world's epicentre of policy error. The effect is already causing debt ratios in half a dozen countries to ratchet upwards to the point of no return, making a mockery of the EMU debt crisis strategy.

ヨーロッパがデフレの罠にずるずるとはまりつつあり、日本に代わって世界の政策ミスの中核となりそうです。この影響は既に半ダースほどの国の債務比率を取り返しのつかない水準にまで急上昇させて、ユーロの債務危機戦略を嘲笑っています。

The EU authorities would do well to study Professor Irving Fisher's seminal paper from Econometrica in 1933, The Debt Deflation Theory of Great Depressions. The central argument should by now be self-evident, though a certain sort of mind had trouble grasping it then, just as it does today. If the price level is falling - the "swelling dollar" in Hoover's America - the real burden of the debt keeps rising.

EU当局は、アーヴィング・フィッシャーによる1933年のエコノメトリカの論文『The Debt Deflation Theory of Great Depression』を研究すると良いと思います。

主張の要点はこれまでに自明の理のはずです、が、今日も当時と同じように、一部の人は理解しずらいようです。

物価が下落すると(フーバー政権下の米国の「膨張するドル」)、債務負担は増大し続けるのです。

Deflation may seem relatively benign in "low-debt" countries at certain times, though less benign than claimed by a rentier class that lives off coupons. People forget that it was a major cause of the American Revolution, since British-imposed monetary contraction after the Seven Years War caused an economic depression, crippling Virginia planters like Thomas Jefferson. It was also the cause of the US agrarian revolt of the 1880s and 1890s, culminating in William Jennings Bryan's plaintive cry: "We shall not be crucified upon a cross of gold."

デフレは「低債務」国では比較的無害に見える時もありますが、不労所得で生活する人たちが言うほど無害ではありません。

皆、それが米国の独立戦争の主要因だということを忘れています。

七年戦争後の英国の通貨緊縮が要因で不況となり、トマス・ジェファーソンのようなバージニア州の大農園主は苦境に陥りました。

また、それは1880年代と1890年代の米国の農園主による反乱の原因でもありました。

これは「我々は金の十字架にかけられないぞ」という、ウィリアム・ジェニングス・ブライアンの物悲しい悲鳴に極まっています。

What is clear is that once total debt exceeds 300pc of GDP, deflation becomes lethal. That is now the case across most of western Europe.

明白なのは、債務が対GDP比300%を突破すれば、デフレが破滅的になることです。

それは今や西欧の殆どで同じです。

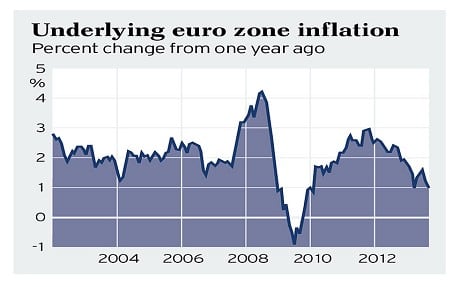

The headline inflation rate for EMU understates the risk, especially for countries in the eye of the storm. A Eurostat index called "HICP inflation at constant taxes" that strips out distortions created by austerity itself - chiefly VAT rises and other taxes - shows that inflation dropped to 0.9pc for the eurozone as a whole in September. This is the lowest since the Lehman crisis and far below the European Central Bank's target of 2pc.

ユーロ圏の消費者物価指数はこのリスクを控えめに表現しています。

嵐の真っ只中にある国々では特にそうです。

『HICP inflation at constant taxes』というEUROSTATの指数は、緊縮そのものによって生み出された歪み(主にVATなどの税率引き上げ)を取り除いたもので、ユーロ圏全体で9月は物価上昇率が0.9%に下落したと示しています。

これはリーマン危機以降最低の水準であり、ECBの目標値である2%を大きく下回っています。

Over the past three months the trend has intensified. France, Italy, Spain, Portugal, Greece, Cyprus, Ireland, Slovakia, Slovenia, Estonia and Latvia have all seen price falls, and already have one foot in deflation. Much the same is happening in the EMU sphere of Bulgaria, Romania, Hungary and the Czech Republic. Poland is at zero. Denmark is close, and so is Sweden, prompting the angry resignation of Riksbank deputy governor Lars Svennson, one of the world's great monetary economists. He too has been citing Irving Fisher's debt-deflation theories in disputes with colleagues.

この3ヶ月間、この傾向は強まりました。

フランス、イタリア、スペイン、ポルトガル、ギリシャ、キプロス、アイルランド、スロバキア、スロベニア、エストニア、ラトビアはいずれも物価が下落しており、片足を既にデフレに突っ込んでいます。

ユーロ圏周辺のブルガリア、ルーマニア、ハンガリー、チェコでもほぼ同じことが起こりつつあります。

ポーランドはゼロです。

デンマークもそれに近く、スウェーデンも同様であり、世界最高のマネタリー・エコノミストの一人であるスウェーデン中銀のラーシュ・スベンソン副総裁は怒って辞任してしまいました。

彼も同僚との論争の中で、アーヴィング・フィッシャーの債務デフレ論を採り上げていました。

The eurozone is one shock away from the Japan syndrome, and therefore the danger of exploding debt ratios. As Fed chair Ben Bernanke famously said in his 2002 speech, "Deflation: Making Sure 'It' Doesn't Happen Here", it is unforgivable for any central bank to let this happen. "Sustained deflation can be highly destructive to a modern economy and should be strongly resisted," he said.

ユーロ圏はあと一回ショックが起これば、日本シンドローム突入であり、従って、債務比率の急上昇の危険も目前です。

ベン・バーナンキFRB議長が2002年のスピーチ『デフレ:ここで「それ」が起こらないようにすること』の中で発言したのは有名ですが、デフレの発生を看過するのは中銀にとってもっての外なことなのです。

「長期的デフレは現代経済にとって極めて破壊的であり、積極的に闘わなければならない」と議長は述べました。

Zsolt Darvas from the Brussels think tank Bruegel argues in an excellent report, Euro Area's Tightrope Walk, that debt dynamics are acutely sensitive to the slightest changes in inflation. He warns that the current downward drift risks pushing Italy and Spain into a "runaway debt trajectory". The closer to deflation, the worse it gets.

ブリュッセルにあるシンクタンクのZsolt Darvas氏は、『ユーロ圏の綱渡り』という素晴らしいレポートの中で、債務ダイナミクスはインフレのささいな変化にも極めて敏感であると論じています。

同氏は、現在の物価下落はイタリアとスペインを「暴走債務軌道」に追い込む危険性があると警告しています。

デフレに迫れば迫るほど、事態は悪化するのです。

Mr Darvas says each one percentage point fall in inflation forces Italy to increase its primary budget surplus by an extra 1.3pc of GDP to stabilise debt. Since it is already targeting a surplus of 5pc, this would lift the bar to 6.3pc, a Sysyphean task. No country except Norway (with oil) has pulled this off over the past half century.

Darvas氏は、イタリアで物価が1%下落する毎に、債務を安定化させるために必要なプライマリーバランスの黒字を1.3%押し上げると言います。

既に黒字目標は5%なので、6.3%に上昇することとなり、無駄な苦労が果てしなく続くことになります。

(石油資源のある)ノルウェーを除き、これに成功した国は半世紀来、一つとしてありません。

Given what happened in February when Beppe Grillo's Five Star movement won the most votes in the Italian parliament's lower house with calls (albeit incoherent) for a return to the lira, and almost 60pc voted for anti-austerity parties, this looks like a tall order. Youth unemployment is already almost 40pc.

ベッペ・グリッロ氏の5つ星ムーブメントがイタリア・リラ復活を(支離滅裂とはいえ)掲げて下院選挙に勝利した2月以降の出来事、そして有権者の60%近くが反緊縮を掲げる政党に投票したことを考えれば、これは無理難題のようです。

若年失業率は既に40%目前です。

Mr Darvas puts his finger on the central contradiction of Europe's debt crisis strategy. The victim states are forced to cut real wages to claw back lost competitiveness against the German bloc through "internal devaluations", yet this frustrates the other objective of controlling the debt. They are damned if they do, and damned if they don't.

Darvas氏は、ヨーロッパの債務危機戦略の主な矛盾を指摘します。

被害国は「内的減価」によってドイツ陣営に対して失った競争力を取り戻すために実質賃金を削減せざるを得なくなっているが、これは債務を管理するという目標の足を引っ張っています。

やってもやらなくてもドツボということです。

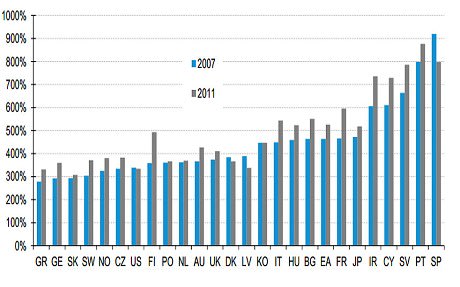

The verdict is already in. Italy's debt has jumped from 121pc to 132pc of GDP over the past two years (IMF data) despite a draconian fiscal squeeze and a primary surplus. Spain has jumped from 70pc to 94pc, Portugal from 108pc to 124pc and Ireland from 104pc to 123pc. Such is the curse of the "denominator effect". It is what happens when debt rises faster than nominal GDP. Europe's policy regime is inflicting ultra-austerity without offsetting monetary stimulus. You have to weep.

既に結論は出ています。

イタリアの債務はこの2年間に、苛烈な緊縮財政とプライマリーバランスの黒字にも拘わらず、121%から132%に急増しました(IMF調べ)。

スペインでは70%から94%に、ポルトガルでは108%から124%に、そしてアイルランドでは104%から123%に上昇しました。

これが「デノミ効果」の呪いなのです。

債務が名目GDPよりも速く増加すれば、こういうことになるのです。

ヨーロッパの政策は金融刺激による緩和を行わない超緊縮政策を押し付けています。

泣くしかありません。

The same vicious dynamic is at work with private debt, which matters just as much. Jamie Dannhauser at Lombard Street Research says the net debt ratio for big companies has risen by more than 100 percentage points in Italy, Spain, France and Portugal since the crisis began, and spiked even more sharply for small firms. "Distressed corporate sectors have not only added to their debt volumes, they have also run down their liquid assets to stay in business. This is where the rotten heart of Europe is to be found. Japanese-style deflation is a disaster for real assets," he says.

これと同じ悪いダイナミクスが、同じくらい重要な民間債務でも働いています。

ロンバード・ストリート・リサーチのジェイミー・ダンハウザー氏によれば、大企業の純債務比率はイタリア、スウェーデン、フランス、ポルトガルで危機勃発以降に100%以上増大しており、中小企業の場合はそれを上回って増大しているそうです。

「行き詰った企業部門は債務を増やしただけでなく、倒産しないために流動資産を減らした。ヨーロッパの問題の中心はここにある。日本式デフレは実物資産にとって大惨事だ」とのこと。

By mistakenly blaming the EMU crisis on profligate states - the morality tale scripted in Berlin, completely false except for Greece - and by imposing a crash diet of fiscal cuts on the wrong countries, they have made the greater problem of private debt even worse. Apart from being brutal, the policy is self-defeating in broader economic terms. While America is deleveraging very fast, private debt ratios have continued to rise in Europe.

ユーロ危機の責任は無頓着な国のせいだ(ベルリンで作られた、ギリシャのケースを除いて全く間違った道徳話)と勘違いな非難をすることで、また見当違いの国に苛烈な緊縮財政を押し付けることで、より大きな民間債務問題を一層悪化させました。

冷酷であるというだけでなく、この政策はより広い経済的な意味において自滅的なのです。

米国は急速にレバレッジ解消を進める中、ヨーロッパでは民間債務比率が上昇し続けています。

Mr Darvas says the only way to break out of the impasse is to let inflation drift up, with rising wages in Germany. The intra-EMU exchange rate gap - arguably still 20pc - could then be closed slowly without forcing the Club Med into a hopeless deflationary spiral. "The ECB should do whatever it takes, within its mandate, to ensure that inflation does not fall below 2pc," he said.

Darvas氏は、この膠着状態を打開する唯一の方法はインフレを許し、ドイツで賃金を上昇させることだと言います。

ユーロ圏内での為替レート格差(いまだに20%に上っています)も、そうすれば、地中海クラブを絶望的なデフレ・スパイラルに追い込むことなく、緩やかに縮まるでしょう。

「ECBはなりふりかまわず、独自に、物価上昇率が2%を下回らないようにしなきゃだめだよ」とのことです。

The ECB is instead sitting on its hands, even though the euro has risen 9pc in trade terms this year to $1.38 against the dollar, M3 "broad" money growth has sputtered out over the past four months, and private loans are shrinking at an accelerating rate of 2pc. The ECB is breaching its own M3 and inflation mandate, and its own published guidelines that inflation should be kept high enough to stave off the risk of deflation in any of the vulnerable countries.

ECBはそうする代わりに手をこまねいています。

今年に入ってユーロが交易条件で1ユーロ1.38ドルまで9%も上昇し、M3マネーサプライの伸びが4ヶ月間低迷し、民間融資が2%という加速度的スピードで減少しているにも拘わらずです。

ECBは自らのM3とインフレに対する義務を放棄しています。

また、インフレは財政難の国のいずれにおいてもデフレを起こさない程度の水準に保たれなければならない、という自ら定めたガイドラインも破っているのです。

As ever, it is the ECB flouting the rulebook for political reasons. You could say it has a chronic German bias. It stoked double-digit money growth to nurse Germany through the slump in the early EMU years, accomodating a dovish Bundesbank, and dooming over-heated Club Med to its fate. This time the Bundesbank is in a hawkish mood, fretting that house prices in Berlin, Stuttgart and Munich are overvalued by as much as 20pc. Perhaps they are, but average rises across Germany have been 2.8pc annually over the past three years, with no signs of a blow-off. Even if there were, Germany could cap rises by clamping down on mortgages.

相も変わらず、政治的な理由のためにECBはルールを軽視しています。

慢性的ドイツ偏向症と言えるかもしれません。

ECBはユーロ発足当初、ドイツが不況から立ち直れるように二桁台でマネーを増やして、ハト派ドイツ中銀の世話をしながら、加熱する地中海クラブを放置しました。

今回、ドイツ中銀はタカ派で、ベルリン、シュトゥットガルト、ミュンヘンの住宅価格が20%も割高だとイラついています。

そうかもしれませんが、ドイツの過去3年間の平均上昇率は年率にして2.8%であり、暴発の兆しはありません。

暴発したとしても、ドイツは住宅ローンを締めて上昇を抑制することが出来ます。

In any case, Germany's own HICP inflation (at constant taxes) has been almost flat since March. The anti-inflation taskmaster may soon be on the cusp of deflation itself, the ultimate irony, but no less dangerous for that.

いずれにせよ、ドイツのHICPは3月以降ほぼ横ばいです。

インフレ反対派の親方は間もなく、全く皮肉にも、デフレに突き当たるかもしれませんが、その方が危険ではないというわけではありません。

As readers know, I have long argued that France, Italy, Spain and Club Med allies should gang up in the ECB's governing council and dictate terms, forcing through the reflation policy that the region so desperately needs. They have the votes. They have the legal and treaty authority to do so. Most monetary theorists around the world would egg them on. Yet they seem paralysed, terrified that Germany will storm off and revert to the D-Mark. They should screw their courage to the sticking plate and call Berin's bluff. Should Germany indeed walk out - and inflict crippling loses on its own banks and insurers in the process - this would at least be a solution of sorts. By lancing the boil, it would open the way for a return to growth.

読者諸氏は御存じの通り、僕は前々から、フランス、イタリア、スペイン、地中海クラブはECBの専務理事会で一致団結して、条件を決定して、この地域が酷く必要としているリフレ政策を推し進めるべきだと主張しています。

これらの国には投票権があるのです。

また、法的、条約的にそうする権限があるのです。

世界中の殆どのマネタリー論者は応援するでしょう。

それでも、ドイツが切れてドイツ・マルクを復活させるのではないかと恐れおののいて身動きが取れないようです。

これらの国は勇気を振り絞って、断固たる態度をとって、ドイツ政府のブラフに挑むべきなのです。

万が一、ドイツが本当に離脱したなら、そしてその中で自国の銀行と保険会社にとんでもない損害をもたらしたなら、これは少なくともなんらかの解決となるでしょう。

膿を出すことで成長に立ち戻る道が開けるのです。

Instead Europe seems to have abdicated leadership, praying for another decade of global growth to lift them off the reefs. This may happen but it is far from assured, and it is not a grown-up policy for the world's second biggest economy. The cycle committee of the Centre for Economic Policy Research still refuses to rule that Euroland is out of recession. Industrial output has been treading water through the summer.

奏する代わりに、ヨーロッパはリーダーシップを放棄して、次の世界成長の十年が助けてくれることを祈っています。

こういうことになるかもしれませんが、その保証はほとんどない上に、そんなやり方は世界第2位の経済がすることではありません。

CEPRの景気循環日付委員会は未だにユーロ圏の不況脱出を否定しています。

産業生産は夏の間も伸びませんでした。

All it needs is one nasty surprise - and there are many lurking, in China and the BRICS - and Europe will lose its monetary foothold. As the Japanese learned the hard way, once you let deflation lodge in the system, it takes heaven and earth to get out again.

一度とんでもないサプライズがあれば十分であり、中国やBRICSでは多くのとんでもないサプライズの影がちらほらしています。

ヨーロッパは足場を失うでしょう。

日本が苦労して学んだように、デフレの発生を許した最後、脱出には途方もない努力を要するのです。