Global funds fear 'summer of shocks' despite boom in money growth

(国際FMがマネーサプライの伸び好調にも拘らず「ショックの夏」を危惧)

Ambrose Evans-Pritchard

Telegraph: 17 MAY 2016 ? 6:58PM

(国際FMがマネーサプライの伸び好調にも拘らず「ショックの夏」を危惧)

Ambrose Evans-Pritchard

Telegraph: 17 MAY 2016 ? 6:58PM

Global fund managers have almost no faith in the latest stock market rallies around the world and have begun to fear the worst from Brexit, putting aside near record sums of money in cash as they brace for a 'summer of shocks'

国際的なファンドマネジャーは世界中で起こっている最新の株高を殆ど信じておらず、ブレギジットの最悪のシナリオを心配し始めて、「ショックの夏」に備えて史上最高に近い額をキャッシュで積み上げています。

Investors have already lost confidence in China's economic rebound this year and are shunning British equities like the plague, fearing a financial crunch if Britain votes to leave the EU.

投資家は既に中国の今年の景気回復への信頼を失っている上に、ブレギジットで金融危機になることを恐れて、英国株を疫病の如く避けています。

What is puzzling is that this mood of deep alarm conflicts with clear evidence of accelerating monetary growth worldwide, usually a harbinger of better times ahead.

不思議なのは、この深刻な警戒ムードが世界中でのマネー・サプライの伸び率の加速(通常は今後の好況の前兆)と矛盾していることです。

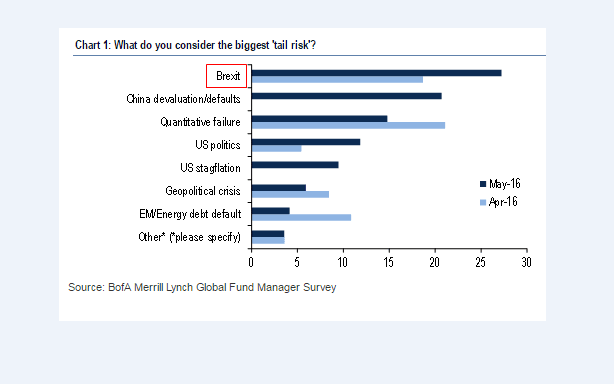

Bank of America's monthly survey of funds shows that 27pc now think Brexit is the biggest 'tail-risk' for the global economy, overtaking neuralgic concerns about a devaluation by China or a wave of defaults by Chinese companies.

バンク・オブ・アメリカの月次ファンド調査によれば、27%が今ではブレギジットは世界経済にとって最大の「テール・リスク」だと考えているとのことで、中国のデバリュエーションや中国企業の倒産多発への懸念を抜きました。

Longstanding fears that central banks are running out of policy ammunition or risk 'quantitative failure' have slipped to third place. The new worry is 'stagflation' in the US, a toxic mix of slowing growth and rising inflation at the same time.

中銀は政策を使い果たしたのではないか、または「QEを失敗」しそうになっているのではないか、という以前からあった不安は第3位にランキングを落としました。

新たな懸念は、米国における「スタグフレーション」、成長鈍化とインフレ上昇が同時に起こる凶悪な組み合わせです。

A net 36pc are underweight UK equities, a level of revulsion last seen in November 2008 and a sign that global fund managers have suddenly woken up to the serious risk that the British electorate may do the unthinkable ? in their eyes ? and walk away from the EU.

回答者の36%は英国株をアンダーウェイトとしていますが、ここまで引かれたのは2008年11月以来初めてです。

国際的なファンドマネジャーが、英国の有権者が(彼らの目には)思いも寄らないことをやってEUを離脱するかもしれないという深刻なリスクに突然目覚めたというサインです。

"While an overwhelming 71pc of investors think Brexit is either 'unlikely' or ' not likely at all', the big plunge in UK equity valuations this month suggests they've prepared for the worst," said the bank.

「71%もの投資家がブレギジットは『起こりそうもない』または『全く起こりそうもない』と考えている一方で、英国株の評価が大幅に落ち込んだことは彼らが最悪の事態に備えているということを示唆している」と同行。

The extent of bearish bets on the UK sets the stage for a powerful rally if the storm blows over, both for the London Stock Exchange and for sterling. A net 20pc think the pound is now undervalued, the most extreme reading since Bank of America started collecting the data.

このような英国株に対する弱気は、嵐が過ぎ去った時にロンドン市場と英ポンドの両方に強烈なラリーをもたらすお膳立てをしています。

回答者の20%が英ポンドは安過ぎると考えていますが、これはバンク・オブ・アメリカがこのデータを収集し始めて以来最も極端な数値です。

Michael Hartnett, the bank's chief investment strategist, says the spring rally on global markets is exhausted as the latest sugar-rush from central bank stimulus fades. The world is in a twilight phase of mounting risk as the post-Lehman business cycle reaches old age.

バンク・オブ・アメリカのチーフ・インベストメント・ストラテジスト、マイケル・ハートネット氏は、中銀の最新の刺激策の興奮が収まって春の国際市場ラリーは終わってしまったと言います。

世界はポスト・リーマン危機のサイクルが終盤に至る中でリスクが増大する黄昏のフェーズにあります。

"Cyclical leading indicators are rolling over, and the decline in US corporate profits has extremely ominous implications for US payroll numbers (jobs) in coming months. We believe a counter-trend rally in the dollar would reignite the downward spiral in emerging markets and commodities, and end the rally in risk assets," he said.

「景気循環の先行指標がロールオーバーしているし、米国の企業利益の減少は今後数ヶ月間の同国の雇用に極めて不吉な意味合いを持っている。米ドルのトレンドに反したラリーは新興市場とコモディティで下方スパイラルを再燃させて、リスク資産のラリーを終わらせると考えている」

Mr Hartnett warned of a choppy market over coming months, advising investors to stay clear of Wall Street until the S&P 500 index of equities has dropped back to a range of 1950-2000.

また同氏は、今後数ヶ月間は不安定な市場が続くだろうとワーニングして、投資家にはS&P500が1950-2000のレンジに戻るまで株には手を出さないようアドバイスしました。

Torsten Slok from Deutsche Bank said markets may have underestimated the inflationary forces building up in the US and are not listening to clear warnings from the Federal Reserve that rate rises are coming. "This is setting up for a battle later this year. I think we could get more January-February style sell-offs," he said.

ドイチェ・バンクのTorsten Slok氏は、市場は米国で高まっているインフレ圧力を過少評価したかもしれない、利上げをするぞというFRBからの明確なワーニングに耳を貸していないと言いました。

「これは今年中にバトルが起こるお膳立てをしている。1-2月のようなセルオフがあるかもしれない」とのこと。

Albert Edwards from Societe General said the red warning sign is a surge in the ratio of US business inventories to sales, now at levels that usually forces firms to slam on the brakes.

ソシエテ・ジェネラルのアルバート・エドワーズ氏は、今や通常は企業に急ブレーキを踏ませる水準になっている、米企業の在庫・売上高比率の急上昇は赤信号だと言いました。

"Recessions are caused by the business investment cycle. The continuing inventory overhang is an increasingly precarious sword of Damocles hanging over investors' heads as profits swoon and liquidation beckons," he said.

「企業の投資サイクルによって不況は発生する。利益が減って清算を招きよせるのだから、過剰在庫が続くことは投資家の頭上にぶら下がる益々危険度の増すダモクレスの剣だ」

These warnings are hitting home. The cash holdings of global fund managers have risen to 5.5pc, higher than the peak during the eurozone debt crisis and comparable to the most extreme levels seen during the Lehman panic in 2008.

このようなワーニングは急所を突いています。

国際的なファンドマネジャーの現金保有高は5.5%まで上昇しましたが、これはユーロ債務危機のピークを上回り、2008年のリーマン・パニックの最中に見られて以来の極めて極端な水準です。

Monetarists are more sanguine about the world. Growth of the M1 money supply in the US has accelerated to 7.8pc, in stark contrast to the monetary contraction in the months leading up to the global financial crisis in 2007-2008.

マネタリストは世界についてもっと楽天的です。

2007-2008年の世界的金融危機までの数ヶ月間に起こったマネーの収縮とは真逆に、米国のM1マネーサプライの伸び率は7.8%まで加速しています。

Simon Ward from Henderson Global Investors says his adjusted gauge - six-month real M1 - has picked up briskly in the US after a soggy patch. Moreover, it is surging at the highest rate since 2009 for the world as a whole, reaching 10pc on an annualized basis.

ヘンダーソン・グローバル・インベスターズのサイモン・ウォード氏は、米国の調整尺度(6ヶ月実質M1)は不調の後で順調に回復していると言います。

更に、世界全体としては2009年来最も早いスピードで急増しており、年率にして10%に達しました。

"The numbers are looking strong everywhere. It may be that the world economy could finally be firing on all cylinders later this year," he said. The M1 data usually leads the actual economy by around six to twelve months.

「どこもかしこも数字は堅調らしい。世界経済は今年末までに、遂に全力で行くことになるかもしれない」

M1データは通常、実体経済の6-12ヶ月先行指標です。

"The one caveat is that we are in uncharted territory with negative interest rates in Japan and Europe, so the historical relationship between money and growth may have been disrupted," he said.

「日本とヨーロッパでマイナス金利という未知の領域に在るから、マネーと成長の歴史的関係は疎外されたかもしれない、と警告するよ」

Bank of America's fund survey is often used a contrary indicator, a sign that investors are clustering in over-crowded positions. They are not always right. Indeed, they are often wrong.

バンク・オブ・アメリカのファンド調査は逆指標として使われることがよくあります(投資家が混雑したポジションに集合しているというサイン)。

いつも正しいわけではありません。

間違うことも本当によくあります。

On that interpretation we may be on the cusp of a powerful global rally.

その解釈に基づくと、僕らは強烈な世界的ラリーの最前線に在るのかもしれません。