予想信用損失アプローチは信用損失の認識の適時性を改善する

国際会計基準審議会(IASB)が、3月7日に、金融商品の減損に関する提案の改訂版を公表しました。

世界的な金融危機を受けて、IASBとFASBが共同で開発してきたプロジェクトですが、完全には一致しないままとなっているようです。

「G20、金融危機諮問グループ1(FCAG)などからの要請に合わせて、IASBと米国財務会計基準審議会(FASB)は、予想信用損失を反映する、より将来予測的な減損モデルを開発するために共同で作業を行ってきた。本日公表した提案は、IASBとFASBとの間で以前に合意した予想信用損失モデルを基礎としたものであるが、利害関係者から受け取ったフィードバックを反映して簡素化されている。」

改訂案の内容については以下のとおり。

「IASBのモデルは、信用損失をより適時に認識するよう設計されている。予想信用損失は、本提案の範囲に含まれるすべての金融商品について、組成時又は購入時から認識される。

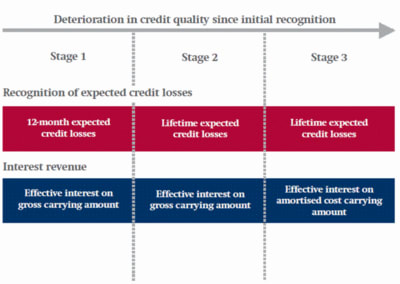

全期間の予想信用損失は、金融商品の信用度が著しく悪化した場合に認識される。これは現在の発生損失モデル(実務上、金融資産が債務不履行に近づいた場合にのみ引当金が計上される)の場合よりも著しく低い閾値である。」

プレスリリースの原文はこちら

↓

IASB publishes revised proposals for loan-loss provisioning(IASB)

The IASB model is designed to recognise credit losses on a more timely basis. Expected credit losses are recognised on all financial instruments within the scope of the proposals from when they are originated or purchased.

Full lifetime expected credit losses are recognised when a financial instrument deteriorates significantly in credit quality. This is a significantly lower threshold than under the incurred loss model today which in practice has resulted in provisioning only when financial assets are close to default.

IASBによる改訂案の概要

↓

Snapshot: Financial Instruments:Expected Credit Losses(PDFファイル)

3段階になっており、何もなければ、「12ヶ月期待損失(12-month expected credit losses)」の金額を引き当てます。「12ヶ月期待損失(12-month expected credit losses)」は、今後12ヶ月間にデフォルトが発生する確率に、そのようなデフォルトから生じるであろう(全期間にわたる)予想信用損失を乗じて算定されます。

An entity calculates ‘12-month expected credit losses’ by multiplying the probability of a default occurring in the next 12 months by the total (lifetime) expected credit losses that would result from that default.

まだ何にも利息収益が計上されていない貸付の最初から信用損失を計上するというのは、理屈に合っていないような気もしますが、期首に開始したと考えれば、信用度の低い(リスクの高い)貸付金の高い利息収益と「12ヶ月期待損失」が、だいたい見合っているはずだということでしょうか。

こちらのページに添付されているPDFファイルが少し詳しい説明になっているようです。

↓

IASBによる新たな期待信用損失モデルの提案(新日本監査法人)

IASB’s financial instruments impairment proposal differs from FASB’s(JofA)

FASB’s model, proposed in a December ED, would require an organization to consider all available information rather than limiting its estimate to losses that are expected during a particular period. FASB Chairman Leslie Seidman has said FASB will examine the comments received on its model as well as the IASB’s model in hopes that the boards can ultimately come to a converged approach.