China shakes off deep slump as credit soars again

(中国:信用爆増再びで深刻な不況にサヨウナラ)

By Ambrose Evans-Pritchard

Telegraph: 6:16PM BST 18 Jun 2015

(中国:信用爆増再びで深刻な不況にサヨウナラ)

By Ambrose Evans-Pritchard

Telegraph: 6:16PM BST 18 Jun 2015

Forward-looking gauges of consumer confidence are rising at the fastest rate since 2007 in China as output picks up on almost every front

ほぼ全ての面で生産が回復する中、中国では先行指標の消費者景況感指数が2007年来最速で上昇中。

China's housing market is roaring back to life in the biggest cities while local governments are issuing bonds at a blistering pace, the latest signs that the world's second largest economy is finally pulling out of a deep downturn.

中国の大都市で住宅市場が猛烈な勢いで復活中のところ、地方自治体は強烈な勢いで債券発行中。

世界第2位の経済大国が遂に深刻な不況から抜け出しつつあるという直近のサインであります。

Output is picking up on almost every front as the effects of credit easing begin to feed through, with the 'expectations' component of consumer confidence soaring to the highest level since the glory days of 2007.

信用緩和の効果がじわじわくる中で、生産もほぼ全ての面で回復中。

消費者景況感の「期待」部分も2007年の栄光の日々以来という高水準へと上昇中。

Rail freight, electricity use, and even sales of diggers and earthmovers are all recovering at last from recessionary levels.

鉄道輸送、電力使用、ついでに掘削機やら土工機械の売上までもが遂に不況レベルから回復しつつあります。

The apparent inflexion point has major implications for the world's commodity markets and for struggling resource economies in Latin America and central Asia that depend on feeding the dragon.

この明らかな転換点は、ドラゴンの餌やりに依存する、世界の商品市場と南米だの中央アジアだのの悪戦苦闘中の資源国にとって、重大な意味合いを持っています。

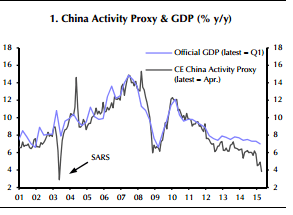

The China Activity Proxy published by Capital Economics – deemed more accurate than the official GDP data – suggests that the underlying growth rate slowed to 4pc in the first quarter. This was the slowest pace since the 1990s, excluding the brief episode of the SARS epidemic in 2003.

キャピタル・エコノミクスのChina Activity Proxy(中国政府の公式GDPデータより正確とされる)によれば、成長率は第1四半期に4%まで減速したみたいですね。

これって1990年代以来最低ペースです(2003年のSARS流行なんて短期的事件は除く)。

The economic cycle has now clearly turned as authorities step up stimulus, clearly worried that efforts to clamp down on the shadow banking system and rein in excess debt may have gone too far for comfort.

シャドーバンキング・システム取締と過剰債務抑制を居心地悪くなるくらいやり過ぎちゃったかも、と明らかに不安そうな当局が刺激策を強化した今や、経済サイクルはきっぱり変わりましたな。

The crucial shift is an expansion of the country's debt swap plan, intended to clean up the Augean Stables of China's local government finances. The regions have switched from bank lending to bonds, issuing $65bn in the first two weeks of June alone.

この重大なシフトとは、中国の地方自治体財政という肥溜を綺麗さっぱりお掃除を目指した、中国債務交換・プランの拡大であります。

同地域は銀行融資から債券にスイッチしまして、6月最初の2週間だけでも650億ドル相当を発行しました。

Mark Williams from Capital Economics said frees up borrowing for other purposes, even if the extra lending is disguised. "The value of these bonds is not included in the central bank's measure of total social financing," he said.

キャピタル・エコノミクスのマーク・ウィリアムズ氏曰く、追加融資が誤魔化されてるとしても、他の目的のために融資をフリーにしてるんだよ、とのこと。

「この手の債券の分は中銀の財源調達に含まれないから」

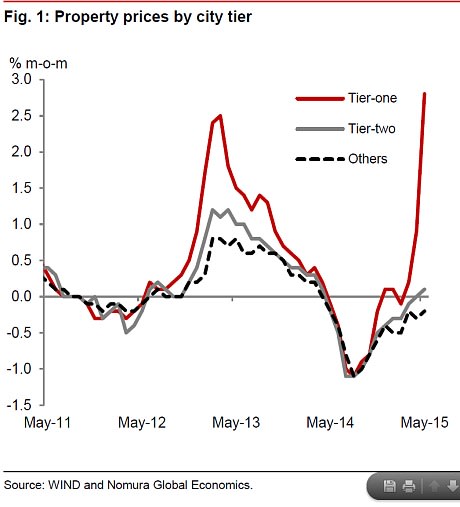

Fresh data from the National Bureau of Statistics showed that home prices in the "tier I" cities jumped 2.8pc in May, the largest one-month rise in over five years.

国家統計局の最新データからは、「ティア1」住宅価格が5月は、1か月間の伸びとしては5年ぶり最大の2.8%も跳ね上がったことがわかります。

Property continued to lag in the rest of the country – with a glut of 4.3m unsold units still hanging over the market - but prices have at least stabilized after sixteen months of declines. The sharp contraction in sales earlier this year has given way to a new burst of optimism, with transactions up 15pc in May.

他の地域では相変わらず不動産は低迷中(売れ残り430万戸)ですが、価格は下落の一途を辿った16ヶ月間の末、少なくとも落ち着きました。

今年先の売上激減も新たな楽観気分に圧倒されて、5月の取引は15%アップしました。

Bo Zhuang from Trusted Sources said the government's attempt to navigate a "controlled slowdown" nearly went awry earlier this year as curbs on local government spending led automatically to fiscal tightening – what some called a "fiscal cliff".

トラステッド・ソーシズのBo Zhuang氏曰く、政府の「管理減速」チャレンジは今年先に地方自治体の支出が自動的に財政引き締めを生じてオジャンになりかけたそうです。

「財政の崖」と呼ぶ人もおりました。

Cuts in the reserve requirement ratio – the central bank's pain policy tool – merely offset the contractionary effects of record capital outflows. They did not add extra stimulus.

RRRの引き下げ(中銀の政策ツール)は記録的な資本流出の引き締め効果をオフセットしただけで、刺激を追加することにはならなかったんですね。

The result was an ugly squall, with a crash in fixed investment and several months of outright contraction in industrial output. It amounted to a minor shock that sent ripples the world. Lombard Street Research estimates that China's real domestic demand plunged by 2.1pc in the first quarter.

で、その結果が大嵐。

固定投資は激減するわ、工業生産は何か月も連続で減少するわ…。

世界中に影響するようなミニ・ショックになりましたとさ。

ロンバード・ストリート・リサーチの試算だと、中国の実質内需は第1四半期に2.1%も激減したみたいですね。

Bo Zhuang said Beijing has now pulled a set of stimulus levers, reverting to the same 'stop-go' pattern of past years. The benchmark market lending rate (7-day repo) has dropped abruptly from 5pc to 2pc, flushing the market with liquidity.

Bo Zhuang氏は、中国政府は遂に刺激策のレバーを引いて、過去数年間の「ストップ&ゴー」様式に立ち戻ったと言います。

ベンチマークの市場貸出金利(7日物レポ)はいきなり5%から2%までガクッと下がって、市場に流動性をジャブジャブさせました。

The country is still in the grip of powerful deflationary forces, with excess capacity in steel, cement, chemicals, and swathes of manufacturing. Factory gate inflation remains stuck at minus 4.6pc and has been negative for 37 months.

中国は相変わらず強力なデフレ・フォースに捕まっています。

過剰生産性は鉄鋼、セメント、化学、あれこれの製造業にはびこってます。

工場出荷価格の上昇率も-4.6%のまんまで、37か月連続でマイナスです。

Yet there is little doubt that the Communist Party has blinked once again, putting off the day of reckoning. "They want a correction without actually having to go through one," said Patrick Chovanec, a China veteran at Silvercrest Asset Management.

でも中国共産党がまたまたありゃりゃと思って、また審判の日を先延ばししたのはほぼ間違いないですね。

「連中は調整を実体験しなくても良い調整がやりたいんだよ」とシルヴァークレスト・アセット・マネジメントの中国ベテラン、Patrick Chovanec氏は言います。

Beijing is winking at a vertiginous stock market boom that has lifted the Shanghai composite index by 150pc over the last year, fuelled by margin debt that eclipses even the final blow-off phase of the Wall Street bubble in 1929.

1929年のウォール街バブル崩壊を彷彿とさせる証拠金負債を燃料に、上海総合指数を1年間で150%も押し上げた眩暈しそうな株高ですが、中国政府はスルー中ですね。

Mr Chovanec said China's leaders are now in much the same position as Japanese officials in the early 1990s when they discovered that it was already too late to escape the consequences of a credit bubble and systemic over-capacity.

Chovanec氏は、中国の指導者達はもう1990年代初頭の日本当局者とほぼ同じ立ち位置だ、と言います。

そう、信用バブルと組織的な過剰生産性が招く結末から逃げるには手遅れだね、とわかったあの時です。

"In the end, they will have to turn on the fiscal taps to prevent a collapse of GDP, just like Japan," he said.

「いずれGDPの崩壊を防ぐために財政を〆なきゃならなくなるんだよ。日本みたいにさ」とのこと。