World asleep as China tightens deflationary vice

(世界が居眠りする間も中国はデフレフォース強化中)

By Ambrose Evans-Pritchard

Telegraph: 8:00PM GMT 12 Feb 2014

(世界が居眠りする間も中国はデフレフォース強化中)

By Ambrose Evans-Pritchard

Telegraph: 8:00PM GMT 12 Feb 2014

We keep our fingers crossed as we glimpse the first foam of a deflationary Ch'ient'ang'kian coming our way from China. The world's central banks have no margin for error

中国からデフレ大潮のアワアワ第一陣が押し寄せて来るのを眺めつつ、天に祈りし続けるとしましょう。世界各国の中銀に失敗の余地はゼロです。

China's Xi Jinping has cast the die. After weighing up the unappetising choice before him for a year, he has picked the lesser of two poisons.

中国の習近平主席は賽を投げました。

一年間に亘ってありがたくない選択肢の数々を吟味した後、主席は最もマシと思われる毒を2つ選びました。

The balance of evidence is that most powerful Chinese leader since Mao Zedong aims to prick China's $24 trillion credit bubble early in his 10-year term, rather than putting off the day of reckoning for yet another cycle.

証拠を比較検討すると、毛沢東以来最強の主席は、次のサイクルまで審判の日を先送りするのではなく、10年間の任期の初期に、24兆ドルに上る信用バブルを弾こうとしているようであります。

This may be well-advised for China, but the rest of the world seems remarkably nonchalant over the implications. Brazil, Russia, South Africa, and the commodity bloc are already in the cross-hairs.

これは中国にとって賢明かもしれません。

が、中国以外の国々はその影響について驚くほど無頓着に見えます。

ブラジル、ロシア、南アフリカ、資源国陣営は既にロックオンされています。

"China is getting serious about deleveraging," says Patrick Legland and Wei Yao from Societe Generale. "It is difficult to gently deflate a bubble. There is a very real possibility that this slow deflation may get out of control and lead to a hard landing."

「中国はデレバレッジについて本気になりつつあるね」とソシエテ・ジェネラルのパトリック・レッグランド氏とWei Yao氏。

「やんわりバブルを弾けさせるのは難しいな。ゆっくりデフレが制御不能になってハードランディングになっちゃう可能性はかなり現実的」だそうです。

Zhang Yichen from CITIC Capital said the denouement will be a ratchet effect since China has capital controls and banks are an arm of the state, but that does not make it benign. "They are trying to deleverage without blowing the whole thing up. The US couldn't contain Lehman contagion, but in China all contracts can be renegotiated, so it is very hard to have a domino effect. We'll see a slow deflating of the bubble ," he said.

CITICキャピタルのZhang Yichen氏曰く、中国は資本規制をしているし銀行だって政府の手先なんだから、行きつく先もラチェット効果だろうけど、だからってそれが良いかって言うとそうでもないとのこと。

「連中は全部ぶっ壊さずにデレバレッジしようとしてるんだな。米国はリーマン危機を抑え込めなかったけど、中国では契約はぜーんぶ再交渉出来るんだから、ドミノ倒しにはならないだろうね。バブルはゆっくり萎むだろう」

What is clear is that we are dealing with a credit expansion of unprecedented scale, equal in size to the US and Japanese banking systems combined. The outcome may matter more for the world than anything that the US Federal Reserve does over coming months under Janet Yellen, well signalled in any case.

はっきりしているのは、僕らが目にしているのは、日米の銀行システムを足した規模に相当する、史上前例のない規模での信用拡大だってことです。

その結果は、イェレンFRBが今後数ヶ月間にやらかすことよりも(どうせ前触れ出してくれるし)、世界にとってもっと影響があるかもしれませんよ。

Societe Generale has defined its hard landing as a fall in Chinese growth to a trough of 2pc, with two quarters of contraction. This would cause a 30pc slide in Chinese equities, a 50pc crash in copper prices, and a drop in Brent crude to $75. "Investors are still underestimating the risk. Chinese credit and, to a lesser extent, equity markets would be very vulnerable," said the bank.

ソシエテ・ジェネラルの中国ハードランディング定義は、2期連続縮小で成長率2%まで激落だそうです。

中国の株価30%暴落、銅価格50%暴落、ブレント原油価格75ドルまで暴落なんてことになるかもしれません。

「投資家は相変わらずこのリスクをなめてるね。中国の信用と、信用ほどじゃないけど株は相当ヤバい」とか。

Such an outcome -- not their base case -- would send a deflationary impulse through the global system. This would come on top of the delayed fall-out from China's $5 trillion investment in plant and fixed capital last year, matching the US and Europe together, and far too much for the world economy to absorb.

そんなこと(規範事例じゃなくて)になれば、世界中に向けてデフレ電波が放たれるでしょう。

しかもこのデフレ電波の前に、去年は5兆ドルもやらかした設備投資の遅行効果があるわけで、その規模たるや米欧を合わせたものに匹敵する上に、世界経済が到底吸収出来ない規模というわけです。

The effects of this on large parts of Latin America, Africa, the Middle East, and core Eurasia would hit before offsetting benefits accrued to consumers in the West. Such commodity shocks are "asymmetric" at first. Southern Europe would fall over the edge into deflation, pushing Italy, Portugal, and Spain deeper into a debt compound trap.

西側の消費者が得する前に、これは南米、アフリカ、中東、ユーラシアのコア国の大半を襲うでしょう。

この手の商品ショックは最初は「非対称的」なものです。

南部欧州はデフレの底に真っ逆さま。

イタリア、ポルトガル、スペインは債務増大トラップの奥深くへと沈められるでしょう。

China did of course blink in January when the authorities stepped in to cover the $500m liabilities of the trust fund, "Credit Equals Gold No. 1". It is the fifth trust rescue in opaque circumstances in recent weeks. Yet it would be hasty to conclude that President Xi is backing away from his Third Plenum vows to end to the bad old ways.

中国は1月、例のトラストファンド『Credit Equals Gold No. 1』の5億ドルの債務をカバーする為に当局が介入した時、確かに一瞬目を瞑りましたよ。

数週間で5度目の怪しげな状況でのトラストファンド救済でした。

でも、習主席は第3回会議の悪慣習終了の誓いを破っている、と結論付けるのはちょっとお待ちを。

The central bank (PBOC) is tightening methodically, allowing the benchmark 7-day repo rate to ratchet up by 200 basis points to 5.21pc over the last year. It drained a further $50bn from the system this week.

中国人民銀行は整然と引き締めを進めていて、ベンチマークである7日ものレポレートが去年一年間で200BPも上がって5.21%になるのを放置しました。

それに今週はシステムから更に500億ドルを減らしました。

Its latest quarterly report has turned hawkish, even though producer prices are in steep deflation, and the M2 money supply is slowing. It complains that "reliance on debt is still rising" and that "hidden risks in the financial sphere require attention".

直近の四半期レポートはタカ派に方向転換しています。

確かに生産者価格は急激に下落していますし、M2マネーサプライの伸びだって減速してますけど。

「借金依存は相変わらず強まっている」、「金融の隠れリスクに注意しなきゃいかん」とご立腹です。

Zhiwei Zhang from Nomura says China has entered a "prolonged period of policy tightening" that will push up bank lending rates by as much as 90bp this quarter, leading to a chain of defaults.

野村證券のZhiwei Zhang氏は、中国は銀行の貸出金利を今期最大90BPも押し上げて倒産を連発させることになる「長期金融引き締め期間」に突入したと言います。

The tell-tale signs are obvious in the central bank's handling of reverse repos and maturing bills. The yield on corporate AA 1-year bonds has jumped 272 basis points to 7.15pc since June. "We think the PBOC intends to raise the whole spectrum of interest rates to push deleveraging," he said.

そのサインは中銀のリバース・レポや償還期限を迎える債券の扱いにおいて明白です。

AA格付け社債1年物の金利は6月以降に272BPも跳ね上がって7.15%になりました。

「中国人民銀行はデレバレッジを進めるためにあらゆる金利を引き上げるつもりだな」とのこと。

This will be a rough ride. JP Morgan's Haibin Zhu says the shadow banking system alone has jumped from $2.4 to $7.7 trillion since 2010, and is now 84pc of GDP. To put this in perspective, the total US subprime debacle was $1.2 trillion.

これは厳しいことになるでしょうね。

JPモルガンのHaibin Zhu氏は、シャドーバンキング・システムだけでも2010年の2.4兆ドルから7.7兆ドルに規模が膨張しまくって今やGDPの84%を占めていると言います。

こうやって考えれば、米国サブプライム危機なんてたかが1.2兆ドルだったんですね。

Haibin Zhu says there is mounting risk of "systemic spillover". Two thirds of the $2 trillion of wealth products must be rolled over every three months. A third of trust funds mature this year. "The liquidity stress could evolve into a full-blown credit crisis," he said.

Haibin Zhu氏曰く、「システミック・スピルオーバー」のリスクは高まりまくりだそうです。

金融商品2兆ドルのうちの3分の2を3ヶ月毎にロールオーバーしなけりゃいけないのであります。

トラスト・ファンドの3分の1が今年中に償還期限を迎えます。

「流動性ストレスは本格的な信用危機に進化しそうだね」とのこと。

Officials from the International Monetary Fund say privately that total credit in China has grown by almost 100pc of GDP to 230pc, once you include exotic instruments and off-shore dollar lending. The comparable jump in Japan over the five years before the Nikkei bubble burst was less than 50pc of GDP.

IMFの当局者が非公式に言うところによれば、中国の信用残高は、特殊商品やらオフショア・ドル建て融資を含めると、GDPの100%近く膨れ上がって230%に達しているそうで。

日経バブルが弾けるまでの5年間に日本でも似たような急増はありましたが、GDPの50%もありませんでしたからね。

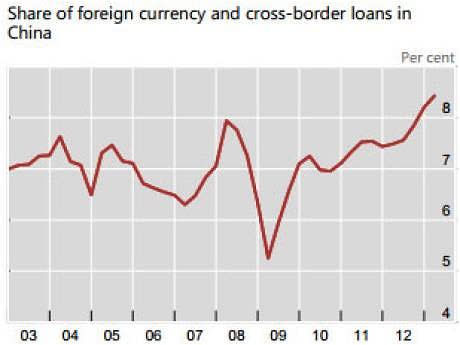

The transmission channel to the global banking system is through Hong Kong and Macao. Bejing's credit squeeze is causing a scramble for off-shore dollar credit to plug the gap. It is this that keeps global regulators awake at night, for foreign currency loans to Chinese companies have jumped from $270bn to an estimated $1.1 trillion since 2009.

国際的な銀行システムへの窓口は香港とマカオです。

中国政府の信用引き締めで、穴埋めのためのオフショア・ドル建て融資への殺到が起こっています。

これで各国の規制当局の中の人は夜も眠れないというわけです…中国企業への外貨建て融資は2009年以降、2,700億ドルからおよそ1.1兆ドルへと爆増してるんですから…。

The Bank for International Settlements says dollar loans have been growing "very rapidly and may give rise to substantial financial stability risks", enough to send tremors across the world.

BISによれば、ドル建て融資は「極めて急速」増加しており、世界の隅々まで激震させられるほど「著しい金融安定リスクをもたらす可能性がある」だそうで。

The BIS data shows that British-based banks -- a broad-term, including branches of US and Mid-East outfits -- are up to their necks in this. They hold a quarter of all cross-border bank exposure to China. By contrast, German, Dutch, French and other European banks have cut their share from 32pc to 14pc as they retrench to shore up capital ratios at home.

BISのデータから、英国に拠点を置く銀行(ざっくり言って、米国や中東の銀行の支店も含みます)はもうこれにどっぷり浸かっていることがわかります。

ここだけで対中融資の4分の1に相当します。

対照的に、ドイツ、オランダ、フランスなど欧州系の銀行は資本引き上げを進める中で、32%から14%に削減しています。

CH: Switzerland, DE: Germany, FR: France, GB: Great Britain, JP: Japan, NL: Netherlands, oEU: Other Europe, RoW: rest of world, US: United States. Source: BIS

This may be why the Bank of England's Mark Carney warned before Christmas that the "parallel banking sector in the big developing countries" now poses the greatest risk to global finance. Officials at the Bank recently showed him an unsettling report by the Hong Kong Monetary Authority on China's off-shore loan risks.

だからなんですね、イングランド銀行のマーク・カーニー総裁がクリスマス前に、「大手開発途上国のパラレル銀行セクター」は今や世界の金融にとって最大のリスクになっている、と警告したのは。

イングランド銀行の中の人は先日、香港金融当局がまとめた中国のオフショア・ローン・リスクに関するとんでもないレポートを総裁に見せました。

Charlene Chu, Fitch's China veteran and now at Autonomous in Beijing, told The Telegraph last week that these dollar debts were large enough to set off a fresh global crisis if mishandled.

フィッチの中国専門家で今や北京のAutonomousに務めるCharlene Chu氏は小紙に先週、このドル建て債務の規模は、その扱いを一歩間違えば新たな世界的危機が起こるほどだと言いました。

Whether this unfolds depends entirely on how the world responds. One can hardly be sanguine. Raghuram Rajan, India's rock star central bank chief, says global co-ordination has "broken down". Turkey, Brazil, and South Africa, among others, are tightening into economic downturns to defend their currencies. Others are distracted by their own political struggles at home.

これが現実になるかどうかは、全く世界の対応にかかっています。

とても楽観的にはなれませんよ。

インドのカリスマ中銀総裁、ラグラム・ラジャン総裁曰く、世界的協調は「ぶっ壊れた」とか。

トルコ、ブラジル、南アフリカその他諸々は通貨防衛のために不況に向けて引き締め推進中です。

他の国は国内の政治闘争に明け暮れています。

The Fed's Janet Yellen can hardly back away from bond tapering as her first order of business, even though US data has turned soggy. She has to shake off her (unmerited) reputation as a dove. Besides, most Fed governors are on the warpath against asset bubbles.

FRBのジャネット・イェレン氏は議長就任初の命令として、米国のデータが嫌な感じになっているにも拘わらず、QE縮小を出さないわけにはいきませんし。

彼女は、イェレンはハト派という(勘違い)評判をなくさなければならないのです。

それにFRBの議長というのは大体において資産バブル嫌いですし。

They may be right, but bear in mind that the growth rate of America's M2 money supply has halved over the last year. It might have contracted since April without $85bn of bond purchases by the Fed each month.

FRB議長連中は正しいのかもしれませんが、でも、米国のM2マネーサプライの伸び率が一年間で半分になっちゃったってことは覚えておかなくちゃ。

FRBが毎月850億ドルの債券を購入していなかったら、4月からだって減ってたかもしれませんよ。

The European Central Bank is paralysed after the German constitutional court read the riot act last Friday, strongly suggesting that its bond rescue plan (OMT) is Ultra Vires and a violation of "monetary financing".

ドイツ憲法裁判所が先週金曜日に停止命令を発して、OMTは越権行為であり「マネタリー・ファイナンス」禁止違反だと断言してから、ECBは麻痺状態です。

The ECB cannot easily carry out quantitative easing to cushion a deflationary shock in the teeth of such a judgment, even if QE is a different tool. In German politics they are the same.

そんな判決を下されて、ECBがデフレ・ショック緩和のための量的緩和をやるのは、QEが違うツールだとしたって、簡単じゃありませんよ。

ドイツ政界じゃ一緒くたなんですから。

The decision came disguised as a referral to the European Court, but was in reality a warning shot, as former judge Udo di Fabio has more or less said. The German court cannot stop the ECB buying bonds but it can stop the Bundesbank from taking part, and must do so if actions are Ultra Vires. That is enough.

この判断は、欧州司法裁判所への付託なんて隠れ蓑を着せて下されましたが、ウド・ディ・ファビオ元裁判官がほぼ言っちゃったように、現実には威嚇射撃です。

ドイツ憲法裁判所はECBの債券購入を停められませんが、ドイツ中銀が参加するのを止めることは出来ますし、これが越権行為なら止めねばならんのです。

以上終了。

So we keep our fingers crossed as we glimpse the first foam of a deflationary Ch'ient'ang'kian coming our way from China. The world's central banks have no margin for error.

というわけで、中国からデフレ大潮の最初のアワアワが押し寄せて来るのを眺めつつ、僕らは天に祈るとしましょう。

世界各国の中銀に失敗の余地はゼロなのであります。